It was always the ubiquitous THEY, those indefinable conspirators who would inevitably force the market to go the opposite way you were playing it. THEY were the rumormongers who forced stock and commodity prices to fluctuate wildly regardless of the economic climate. THEY were the ones who toyed with the military-industrial complex of the fifties and sixties and then with the oil powers of the seventies. THEY profited from those long lines of gas-hungry cars and the shortages of everything from aluminum to wheat. THEY were the brains, the real insiders with all the money to manipulate the markets to make more. THEY were the immovable forces that gave you that lonely feeling that you were up against it, the ones that always profited by your mistakes. THEY were the ones who used pit gossip to create doubts about your stature as a shrewd trader. THEY were the enemy; heartless, calculating, always on the offensive, forever elusive. THEY were everything you weren’t.

Paul had become obsessed with the “they factor” to the point where he would rationalize away his own trading blunders. THEY, of course, were always around to take the blame for his poor judgment. Damn, were THEY cunning. Sometimes THEY would suck you into the market by letting you win first; then, like a shifty hustler, THEY would wipe you out. THEY would always see you as just a small-time Charlie Potatoes, a Fast Eddie Felson squeezed between Minnesota Fats and Willie Mosconi in a game of cutthroat nine ball. It always worked. You could never learn your lesson. THEY knew just how greedy you were and that small profits would never satisfy you. And just when you were raking it in, inevitably THEY would lower the boom.

. . . The New Gatsbys, by Bob Tamarkin

Recently the word “they” has surfaced with the media; THEY are influencing elections, THEY colluded with the Russians, THEY are selling U.S. dollars, THEY are manipulating markets, THEY are buying bonds, and a week and a half ago THEY sold the tech stocks causing sort of a minicrash as whispers of a “bubble” careened down the canyons of Wall Street. Yet CNBC’s sagacious Bob Pisani cited a survey by Bank of America asking, “Are the internet stocks in a bubble?" To wit:

Some light on how Wall Street views this came today from Bank of America, which published its Global Fund Manager Survey this morning. The 210 fund managers weighed in on the key question - are (the) internet stocks in a bubble? The conclusion: the majority believes they are expensive, but not in a bubble, a subtle but important distinction. Here are the results. Fund managers on internet stocks: Expensive 57%, in a bubble 18%, fairly priced 25%. On the broader question - are equities overvalued? Forty-four percent said yes, which is the highest ever, and a jump from 37% in May. However, roughly 50% believe that global profits will continue to improve.

Shortly after I read Bob’s blog I received this from a particularly bright portfolio manager in Canada. He writes:

I think many people assume the FANGs are in a bubble because of price action alone and totally disregard the sales and earnings growth that’s accompanied it. I also think most people don’t really know what kind of multiples a lot of these companies even trade at. For example, Facebook is trading @ 25x P/E (NTM) and a PEG (price to estimated growth) below 1. Google is @ 22x P/E (NTM) and a PEG of 1.4. Apple (not a FANG) trades under 15x (Bloomberg data). And all are even lower if you want to back out share-based compensation (SBC) and cash in the case of Apple.

It doesn’t seem like a bubble to me given the tremendous growth potential, market dominance (Google has over 80% of the search market globally) and high profitability. [These points are] especially relative to the market, which should have a higher multiple for the reasons you have often mentioned. We’re taught in business school that a trailing P/E above ~20 is expensive and one below ~13 is cheap, so many will just assume Netflix and Amazon are outrageously priced without further investigation. They start with the conclusion and work backwards. Also, the tech wreck may not be fresh in everyone’s mind, but it’s probably not forgotten either – and generals are always fighting the last war!

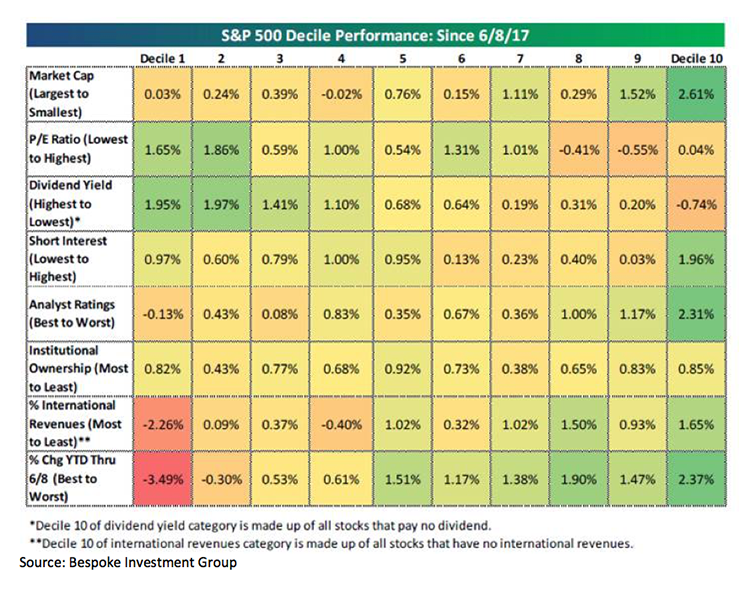

Last week, however, the tech trashing continued, leaving one of the technology indices we follow off almost 5% from its June 9, 2017 intraday peak. Despite that, the rest of the stock market seemed to go back into flat lining mode with the S&P 500 (SPX/2433.15) gaining a mere 0.06% for the week. Flat lining, indeed, because at its May 25 intraday high the SPX traded at ~2419 and at last Friday’s intraday low it changed hands around 2422. Beneath the surface, however, there was a pretty big rotation. As Bespoke Investment Group writes:

We take a closer look at each category [in its report], but the matrix below [see chart on page 3] lets you see that the smaller stocks in the S&P have been outperforming the largest stocks, the stocks with the highest dividend yields have outperformed stocks with low or no dividends, the stocks most unloved by analysts have been outperforming, and stocks with heavy international revenue exposure have gotten hit. This is a complete reversal of what was working in 2017 prior to last Friday.

So, even with the tech trauma, the D.C. debacle, more terrorist tactics, a rate ratchet, the flattening yield curve, North Korea, soft economic statistics, etc., there has been virtually no damage to the SPX’s chart pattern. Moreover, the flat lining since late-May has actually allowed the stock market’s internal energy to be rebuilt to levels that will support a decent move, which Andrew and I think will come on the upside. What has been interesting is the rotation by investors into the financial, industrial, and energy sectors, a rotation we like. To us that rotation shows there is still a healthy amount of cash out there that needs to be put to work. According to Nuveen’s Bob Doll there is roughly seven trillion dollars on the sidelines.

The call for this week: We have just come off of the strongest earnings season we have seen in years, with the S&P 500 earnings improving nearly 14%. More importantly, the “bears” that have been telling us earnings may be okay, but revenue growth is nonexistent, just got proven wrong with revenue up almost 8%. This is the kind of action you typically see as the equity markets transition from an interest rate to an earnings driven secular bull market. Obviously, there will be a time when our indicators, models, and the stock market’s own price action start to suggest more caution, but now is not that time. This morning the SPX is ignoring the Syrian escalation where a U.S. Navy F/A-18 shot down a Syrian Su-22 fighter jet, and a new terrorist truck-pedestrian attack in London, leaving the preopening S&P 500 futures better by some 6 points at 5:33 a.m. Like we have said, “In bull markets most of the surprises come on the upside!”