South Korea’s Too Big to Fail

On March 10, Park Geun-hye was removed from her position as president of South Korea. Her ouster came on the heels of a scandal involving her close confidant who is accused of seeking bribes from chaebols, a group of family-owned multinational conglomerates that dominate the South Korean economy, to curry favor with the Park administration. Prior to the scandal, Park’s political party, Liberty Korea, had been accused of prioritizing the interests of the chaebols over the interests of the Korean people.

This controversy has paved the way for populist candidate Moon Jae-in, from the Democratic Party of Korea, to rise to the presidency. It is assumed that he will look to loosen government ties with chaebols. Recently, chaebols have come under scrutiny as many people feel that their overall size and dominance have constrained the economy. Currently, South Korea suffers from high youth unemployment, rising household debt and rising income inequality. Moon Jae-in has vowed to tackle each of these problems in addition to chaebol reform. This task may prove to be difficult as the chaebols have accumulated a lot of political clout over the years, thus he may find it difficult to pass serious reforms through parliament.

In this report, we offer a brief history on the origins of chaebols and their influence in lifting the country out of poverty. From there, we will focus on the role the Asian Financial Crisis played in changing public attitude toward chaebols and examine possible chaebol reforms. Finally, we will conclude with market ramifications.

Chaebol Origin

The term chaebol means “wealth clan” in Korean. Chaebols were originally started by the Japanese during their occupation of the peninsula.1 As is typical with colonialism, Japan modernized Korea’s infrastructure to make it more suitable for industrialization. In addition to the infrastructure changes, the Japanese began financing chaebols to develop strategic sectors of the Korean economy. Most of the chaebols at the time were Japanese, but there were a few Korean-run chaebols. The most prominent Korean chaebol was Samsung (005930.KS, ₩2,297,000.00), which at the time was a trade company that shipped food from South Korea to Manchuria.2 Although the chaebols were profitable, much of the wealth generated was repatriated to the Japanese empire as a form of tribute, while most Koreans remained impoverished.

After the Japanese were defeated in WWII, they and the Japanese-owned chaebols were forced to leave the Korean peninsula. Following Japan’s departure, the Korean War ensued between regions north and south of the 38th parallel of the Korean peninsula. The war led to the destruction of much of the infrastructure built by the Japanese. In order to foster recovery, South Korean leaders emulated Japan’s economic development model and established chaebols. They established their role in the economy in 1961 when a coup overthrew President Yun Bo-seon and placed Park Chung-hee in power.

Rags to Riches

Following the conclusion of the Korean War, South Korea used U.S. foreign aid to rebuild its infrastructure. This aid was used to invest in schools, roads and modern communication networks. In addition, South Korea encouraged household saving by implementing import substitution. This involved placing restrictions on imports through tariffs and quotas to give domestic firms a competitive advantage over foreign firms. Consequently, domestic firms charged high prices for their goods, which led to suppressed consumption. The accumulated savings that resulted allowed firms to obtain inexpensive loans, which made it easier for them to expand their capacity. It is worth noting that although import substitution helped firms grow, it did little to improve the living standards of Koreans.

After rising to power through military coup, Park Chung-hee moved South Korea away from import substitution and toward export promotion. His first order was to nationalize all of the banks and then proceeded to allocate credit to chaebols through cheap loans and export subsidies. Instead of providing the loans to a broad group of firms, he targeted firms that specialized in steel, textiles and petrochemicals and later expanded to other sectors such as semiconductors and cars. Essentially, the chaebols became “national champions” that would work to dominate sectors of the export market. The idea was to use all of the country’s resources to exploit areas in which Korea had a competitive advantage. As the chaebols began to specialize and gather market share, Park allowed them to venture into higher valued goods.

Increased bargaining power and production led to suppressed input prices and wages per good. This allowed the chaebols to quickly expand their capacity and achieve economies of scale. As chaebols dominated sectors, they began venturing into unrelated industries. Samsung (005930.KS, ₩2,297,000.00), for example, began making semiconductors.3 The chaebols’ increased profitability eventually led to higher wages for laborers and urbanization. In order to take advantage of the job opportunities offered by the chaebols, South Koreans migrated from rural areas to urban areas.

From 1965 to 1979, South Korea’s real GDP growth averaged 9% per year. As chaebols became more successful, they began to build even closer ties with the government. Politicians relied on chaebols to create jobs in their regions and the chaebols relied on politicians for favorable treatment. The public revered the chaebols, crediting them with pulling the country out of poverty; chaebol executives were essentially treated as rock stars.

Asian Financial Crisis

After Park Chung-hee’s assassination in 1979, the government gradually became more decentralized. In 1992, the South Korean government liberalized the banking system and granted foreigners access to the Korea Stock Exchange. While chaebols were allowed to own shares in banks, regulations prevented them from owning controlling stakes. Chaebols were able to work around this restriction by buying controlling shares in offshore non-banking financial institutions (NBFIs). Owning shares in the NFBIs provided the chaebols with access to U.S. dollar credit from international lenders. Chaebols were attracted to credit abroad because they offered lower rates than domestic banks. Furthermore, the chaebols believed that currency risk was eliminated since the South Korean won was pegged to the dollar. International lenders agreed to provide credit because chaebols were profitable and relied on the assumption that the South Korean government would not allow them to fail.

Access to credit from abroad encouraged the chaebols to become more heavily leveraged. As these firms added on more debt, they became vulnerable to external shocks due to changes in U.S. monetary policy. The increased indebtedness of these firms became a growing concern as firms began investing in riskier business ventures in hopes of boosting profits. Mid-sized firms were especially aggressive as they were desperate to take market share away from the larger chaebols.

In 1994, the Federal Reserve started to raise rates in order to prevent the U.S. economy from overheating. As a result, the dollar began to appreciate relative to other world currencies. Because most Southeast Asian economies, including South Korea, pegged their currencies to the dollar, their currencies also appreciated. Accordingly, exported goods from this region became less competitive and businesses became less profitable. A key element of export promotion is a weak currency, so appreciation undermines the economy. These countries also fell victim to speculative attacks as hedge funds believed that currencies within the region were overvalued. Although South Korea was not immediately brought down by the crisis, its economy began to show signs of stress as inventories rose and profit margins narrowed. Increased pessimism in the region led to a credit crunch that made it harder for chaebols to refinance their loans. As a result, 16 out of the top 30 chaebols would eventually file for bankruptcy.

In 1997, the South Korean government was forced to accept a bailout from the IMF and other developed nations. The terms of the agreement included austerity and chaebol restructuring. In order to comply with the bailout, chaebols laid off workers and cut salaries, while the government had to roll back entitlements. The chaebols facing bankruptcy had to sell some of their non-core businesses to other chaebols at a discount. In addition, chaebols had to adhere to international accounting standards and corporate governance practices. Even though the people of South Korea complied, with many selling personal belongings to help the government repay the loans, the chaebol reputation was stained. The Asian Financial Crisis turned the perception of chaebols from revered symbols of Korean exceptionalism to symbols of excess and corruption.

Generational Gap

Since the Asian Financial Crisis, chaebol reform has been a topic of debate. This issue has led to a generational divide between those who grew up before and after Park Chung-hee's reign. The Park generation, those living during Park's reign, has a more favorable view of the chaebols, while the younger, post-Park generation views the chaebols with skepticism. The Park generation remembers the chaebols lifting them out of poverty, whereas the post-Park generation remembers the IMF bailout.

The Park generation is less critical of the chaebols, having witnessed them transform South Korea from a struggling agrarian economy to the world’s 11th largest economy. As a result, this generation, especially those who are employed by chaebols, believes that chaebols are a national treasure that the government should protect rather than penalize. The older generation enjoys the corporate tradition established by the chaebols that stresses loyalty and commitment to its more tenured workers. Consequently, many of the chaebols have adopted a last-in/first-out system of hiring and firing, in which younger workers are viewed as relatively expendable. Chaebols, in a sense, reinforce the tradition of honoring the elders in society. There is fear among the Park generation that reforms could lead to forced retirements in favor of younger workers.

The post-Park generation is suspicious of government ties with the chaebols and believes that the government should focus on helping people. The lack of prospects after graduating college has been their biggest source of contention. About 69% of workers between the ages of 25-34 have college degrees, which is the highest among OECD countries. Due to increasing demand and limited job postings, young adults are forced to take entrance exams in order to secure employment in the chaebols. Those who fail are forced to accept temporary jobs at smaller firms for longer hours and less pay. According to McKinsey& Co., a management consulting firm, wages at smaller firms are 38% lower than the chaebols.4 Essentially there is a two-tier labor market in which the highly skilled and well-connected are able to land high-paying and steady jobs, while the others are forced to work temporary jobs.

Relatively high prices for goods and rising household debts have increased the burdens on struggling groups in both generations. The government has tried to rectify the problem by offering cheap loans to the elderly and those with low credit ratings. Attempts to reform labor laws to make it easier for chaebols to lay off older workers have been met with staunch resistance from labor unions. As a result, the prior administration has struggled to meet the growing demand for relief for those struggling at the lower end of the income scale.

The Chaebol Curse of Bigness

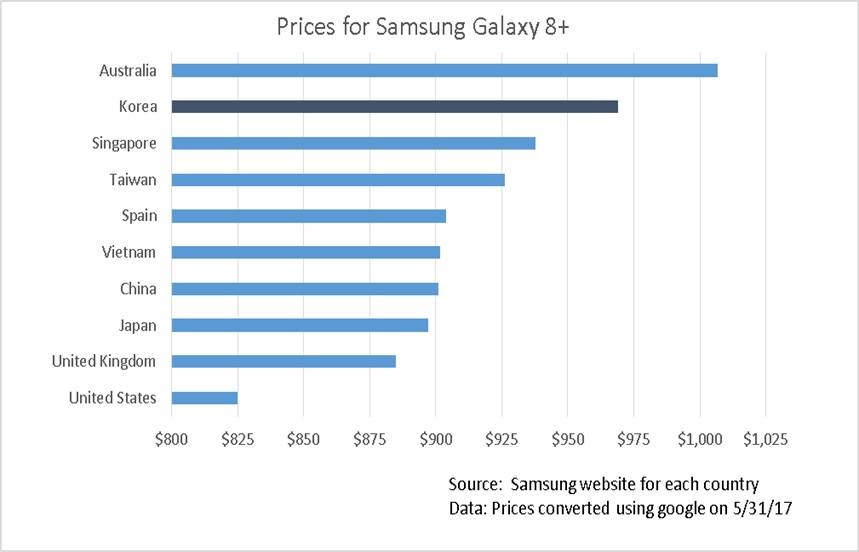

Chaebols have generated healthy profits for their owners and expanded their operations globally, even as the South Korean economy has slowed. Their successes are due to state-sponsored monopoly power. Being state-sponsored monopolies, chaebols are able to charge higher prices for goods domestically than they do internationally (see chart below). This price discrimination allows them to offset losses from selling goods abroad. In addition, trade restrictions on international goods allow domestic prices to stay relatively high. The additional revenue generated domestically allows the chaebols to subsidize their exports.

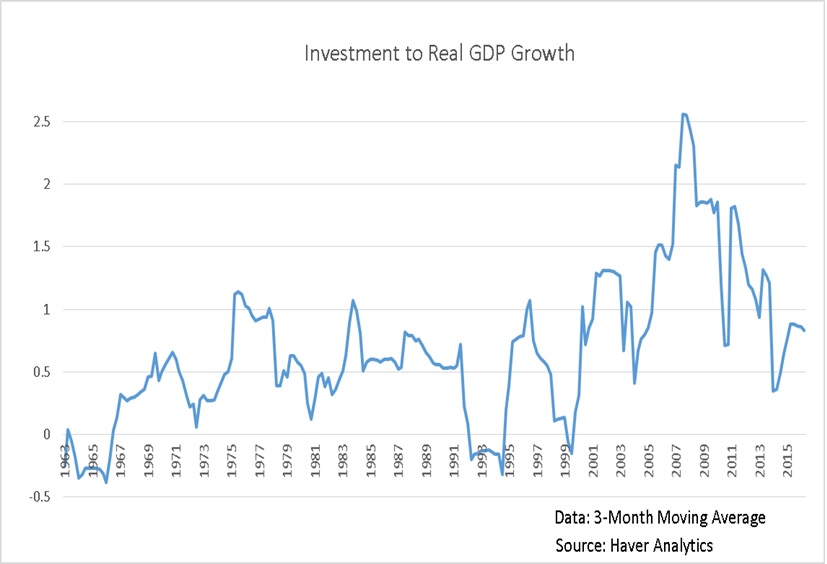

The chaebols’ almost monolithic control over the South Korean economy allow them to squeeze out smaller companies by crowding out capital and labor. The chaebols’ excessive funds allow them to buy up most of the country’s resources and bid up the cost for highly skilled workers, thus making it harder for startup companies to offer competing products. In the past, allowing state-sponsored chaebols made sense because the chaebols could efficiently direct the investment as they expanded their capacity. Recently, though, the effect of investment on real GDP growth has waned. In other words, South Korea is no longer getting the same return on chaebol investment.

While chaebols were instrumental in pulling South Korea out of its poverty-stricken state after the Korean War, they are currently putting the country in economic paralysis. As chaebols have increased their market share in various industries around the world, much of the country's wealth has been concentrated in the hands of the chaebols, even as economic growth has slowed. Furthermore, critics claim that the chaebols have been using their excessive funds to prop up failing business ventures as opposed to paying out dividends to their shareholders. This has a negative impact on the economy as it limits investors’ abilities to efficiently reallocate funds to other sectors of the economy. The practice has led the chaebols to be undervalued relative to their peers in what investors have nicknamed the “Korea Discount.”

Prior administrations have been cautious to rein in the chaebols due to their effect on the economy and their political influence. The five biggest chaebols account for about half of the value of the Korea Stock Exchange and their total revenue constituted about 58% of South Korea’s GDP in 2015. The ouster of Park Guen-hye represented growing public support for less government involvement with the chaebols. The South Korean government now has the political capital needed to institute new reforms. On the campaign trail, Moon had vowed to take on the chaebols by ending government pardoning of the chief executives, increasing their transparency and limiting the board members’ abilities to pass down ownership to their children.

Ramifications

Despite the tough talk, Moon has yet to introduce any anti-trust legislation. Breaking up the chaebols could lead to large layoffs and could anger the labor unions, who have been known to be militant in the past. In order to avoid possible political instability, we believe that Moon will attempt to pass modest reforms, such as giving shareholders the right to vote for board members, corporate transparency and more conservative accounting standards.

In summary, we believe that chaebol reform could improve the economic outlook for South Korea. Although Moon is unlikely to break up the chaebols, improving chaebol transparency as well as shareholder participation could lead to more shareholder value. As a result, if reforms are significant, it is likely that Korean equities will appreciate; this would be especially true for smaller South Korean firms.

Thomas K. Wash

June 12, 2017

This report was prepared by Thomas Wash of Confluence Investment Management LLC and reflects the current opinion of the author. It is based upon sources and data believed to be accurate and reliable. Opinions and forward looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

© Confluence Investment Management LLC

Confluence Investment Management LLC is an independent, SEC Registered Investment Advisor located in St. Louis, Missouri. The firm provides professional portfolio management and advisory services to institutional and individual clients. Confluence’s investment philosophy is based upon independent, fundamental research that integrates the firm’s evaluation of market cycles, macroeconomics and geopolitical analysis with a value-driven, fundamental company-specific approach. The firm’s portfolio management philosophy begins by assessing risk, and follows through by positioning client portfolios to achieve stated income and growth objectives. The Confluence team is comprised of experienced investment professionals who are dedicated to an exceptional level of client service and communication.

|

|

1 The Japanese word for chaebol is “kaibutsu.”

2 Kim, C. (2016). Samsung, Media Empire and Family: A Power Web. New York, NY: Routledge (p. 31).

3 We mentioned previously that it was a trade company.

© Confluence Investment Management

Read more commentaries by Confluence Investment Management