On a craps table, if a 7 or 11 rolls on the first throw of the dice, you are an automatic winner if you are betting the “pass line.” But, if you roll a 2, 3, or 12 on the first roll, you lose. So “7 come 11” means that any time after the first roll, when a shooter has a point to make, you win with a bet on the “come line” with a roll of a natural 7 or 11 and lose on craps (2, 3, or 12).

So, last week I found myself in Reno Nevada, and then Las Vegas, speaking at events for our financial advisors and a couple of conferences. Now, anytime I am near a craps table, I like to throw dice. Unfortunately, my first attempt to do so saw me, as well as everyone else at the table, unable to make three passes in a row. The experience was costly, as the “pass line” bets were all losing bets. The second night, I decided to bet on the “don’t pass” line, meaning you are betting against the players trying to make the designated point. It is not much fun playing the “don’t pass” line, and the other players do not like people betting the “don’t,” but that night it proved to be the winning strategy. Having won back my previous losses, I decided to play the “pass line” the next night only to lose all the money I had won the previous night.

Similarly, participants should have bet the “don’t pass” line last Wednesday when the D-J Industrial Average (INDU/20804.84) lost an eye-popping 373 points for the biggest one-day loss of the year. Yet, this should have come as no surprise, because as Andrew and I wrote last Monday:

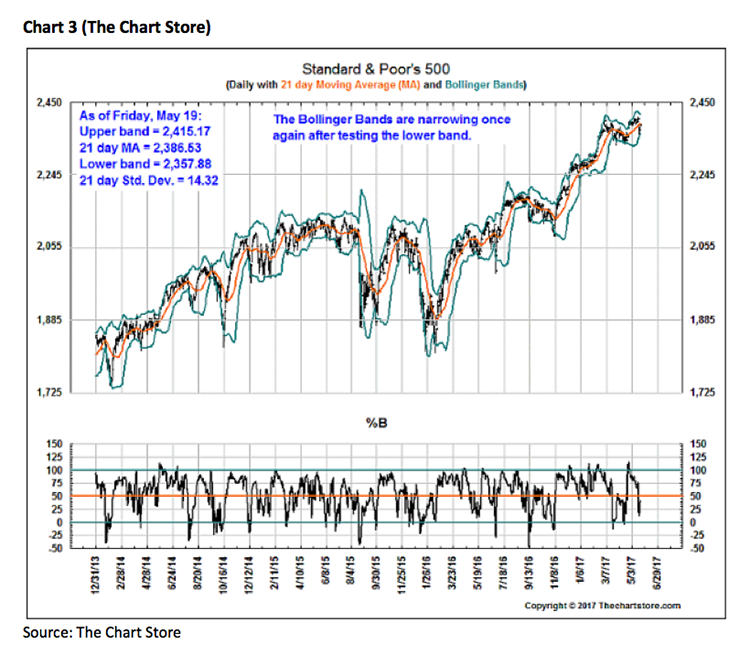

Our models suggest the “drop” in equity prices ended on April 19th with another breakout to new all-time highs slated to begin late this week. Early this week [however] has the potential for some further stock price weakness, but by late week that potential weakness should abate. The compression of the Bollinger Bands, like our models, are telegraphing the potential for a pickup in volatility, which we think will come on the upside beginning late this week or early the following week.

Last Monday, that strategy looked flawed when the senior index tacked on roughly 85 points. Tuesday, it looked a little better as the Industrials hugged the “flat line.” Comes Wednesday, and well, you all know how Wednesday turned out. To be sure, Wednesday’s Wilt caused the S&P 500 (SPX/2381.73) to close below its 50-day moving average (DMA) at 2369.53. As our friend Craig White wrote Wednesday afternoon:

To summarize Wednesday’s action, I sent a more balanced note to some contacts stating the following; “Art Cashin said it best this afternoon ‘a lot of damage done today on the charts, but not irreparable’. Indeed, a lot of uncertainty with respect to obstruction of justice etc. and those cracks/doubts finally emerged today. Far too early to determine if this is the start of a more serious decline, but I agree, I don’t like to see the banks lead on the downside. That said, yields gapped lower today so I’m not surprised to see this, which was also reflected in the insurers. Technology was off 2.8% today, with the mega caps contributing to a good percentage of the points lost. When the financial and tech sectors, which account for ~40 % of the index, lead on the downside, it’s bound to produce a more meaningful decline such as the 1.8% seen today. The divergence in transports is also concerning as it was broad based across the 20 constituents, but this trend has been in place since March. That said, the spread between the industrials and transports is widening which certainly needs to be respected. So where do we go from here? Well, the next few sessions should provide some guidance as to the seriousness of the recent Washington machinations with the market ultimately deciding on its relevance. It’s best to sit back and observe the ensuing trading action with patience and diligence. In the meantime, sharpen the pencils in anticipation of putting money to work if this blows over and another buying opportunity presents itself, which unless significantly violated on the downside, I believe will be the outcome. Stay tuned.”