In certain cases, leverage doesn’t need to be applied to meet enhanced return targets. Distressed assets, restructurings, or assets in the development phase, can in some cases offer unlevered returns comparable to the levered assets described above. The return differential often stems from investing in an asset offering an income stream, and one with no income and significant operational complexity. Hence although these assets are unlevered, investing in them isn’t necessarily less risky, as they may still have very volatile return profiles.

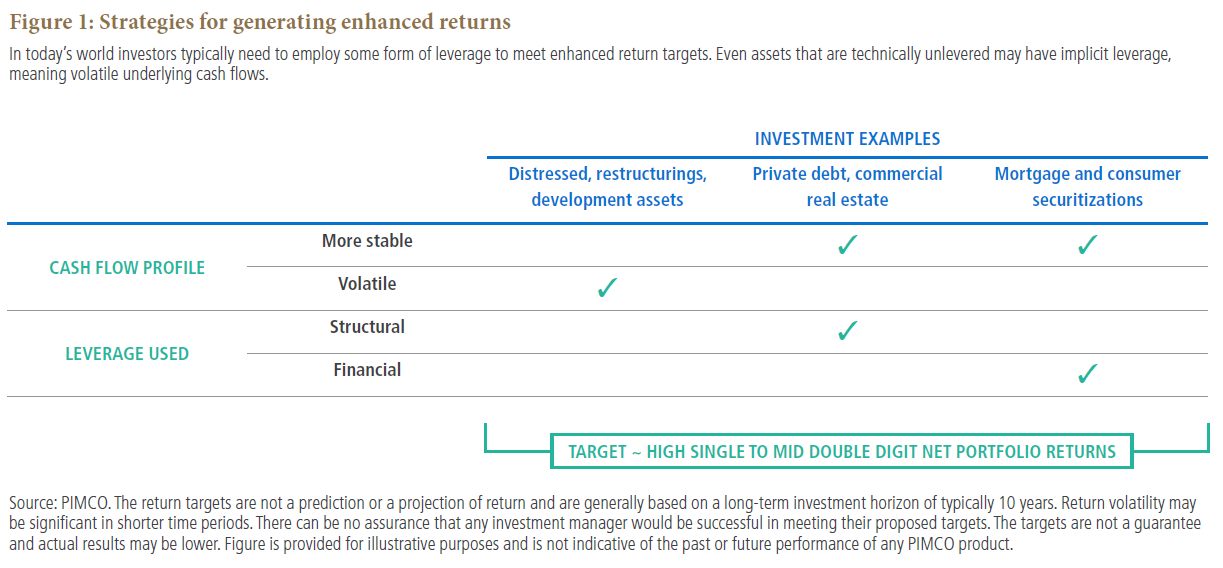

In short, investors seeking enhanced returns likely either need to employ some form of explicit or direct leverage, or take on more risk via implicit leverage, by investing in assets with more volatile cash flows. These options are summarized in Figure 1.

Types of leverage

If a strategy employs direct leverage, then it will typically be broken out between structural leverage – resulting from an asset’s position in the capital structure – and financial leverage, which is associated with the use of derivatives, synthetics and repurchase (repo) agreements.

STRUCTURAL LEVERAGE

By definition, we view an investment as structurally levered if one percent of collateral loss can create more than one percent of loss to the investment. Examples include the first loss or mezzanine tranche on a mortgage pool, or the equity and subordinated debt in a company, assuming both have senior debt outstanding. When analyzing a structurally levered investment, it’s important to analyze loss distribution (cash flow variability), debt mechanics and asset volatility, among other factors, to understand the investment’s risk profile.

Generally speaking, structural leverage works well when longer term debt is applied to assets with stable cash flows, such as private debt or core commercial real estate. In these situations, the levered income component can potentially stabilize the return profile. For example, consider a commercial real estate building with a 6.5% capitalization rate (the return from income), funded with a 3.5% loan at a 75% percent advance rate (the loan-to-value percentage). This profile offers a low double digit return for the sponsor or equity holder, based off the income alone. If this is earned for several years, the sponsor can sell the underlying building at a steep discount to price originally paid and still have a positive total return – referred to as “burning the basis down.” Selling the building above the original price can lead to substantial return potential (subject to risks, which are discussed below).

Structural leverage offers the key benefit of being non-recourse, meaning that the loan is secured by collateral only (a lender has no claim on any other assets of the borrower), and also non-mark-to-market. This can allow asset values to recover from temporary losses if the underlying collateral recovers, as was the case with many investments that experienced recovery post the financial crisis, despite substantial cash flow disruption during the event. Essentially, their liability structure enabled them to withstand the cash flow uncertainty. CLO equity’s resilience during the financial crisis is one such example.

A key downside, however, is that many structurally levered investments are arguably negatively convex, meaning they have limited upside with large downside risks. This is particularly true of many mezzanine assets that lack upside potential as they can materially underperform during periods of economic stress. Often this is due to embedded “triggers” within the debt instruments; for example, a company losing its biggest client, a commercial building having its largest tenant file for bankruptcy, or the need to roll over the debt at the maturity date, all of which could each lead to very significant losses.

Accurately assessing the cash flow uncertainty of the asset is critical to evaluating the risk of structural leverage. Often, we use asset volatility as a proxy or metric to evaluate an investment’s inherent risk. For example, consider a lending company which has a loan book of $100, funded by $10 of equity, $20 of mezzanine debt and $70 of senior debt. If the value of the loan book declines by 31%, then the value of the mezzanine and equity tranches is wiped out, as the underlying asset value is now $69. If a liquidation trigger is breached, these tranches’ recovery value could be 0%. Put another way, if the value of the loan book declines by 10% to $90, each percentage of additional decline wipes 5% off the value of the mezzanine tranche – hence its inherent risk.

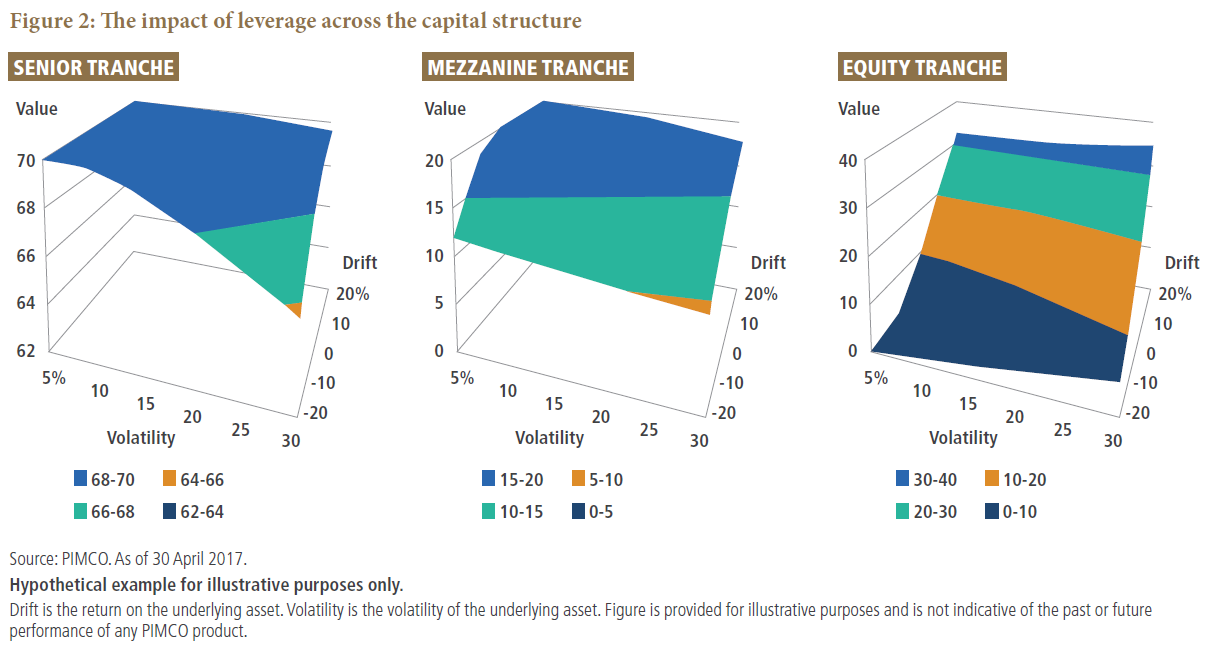

By applying an option valuation framework, we can see how structural leverage plays out across the capital structure. Figure 2 shows a simple capital structure where underlying asset value ($100) is distributed to the senior ($70), mezzanine ($20) and equity ($10) tranches sequentially, and demonstrates how the value of the tranche changes as a function of the underlying asset return (drift) and volatility (vol). The charts show that an increase in asset return (drift) increases the return across all tranches, while an increase in asset volatility increases the return on the equity tranche, but lowers the return on the senior tranche. It also shows how the equity tranches are most sensitive to the underlying asset return distribution.

FINANCIAL LEVERAGE

Financial leverage is the ability to use mark-to-market/recourse borrowing to finance the purchase of an asset or portfolio. Examples include derivatives, synthetics and mark-to-market repos on cash investments. This is recourse leverage and in the context of a portfolio, there can be a direct claim on all the assets, not just the one being funded. Funding a senior asset with financial leverage essentially creates a “mezzanine” profile, creating the basis for investors to compare relative value versus structural leverage. Often, however, this entails making subjective assumptions.

Financial leverage is often considered risky given its recourse nature and inherent asset-liability mismatch, which can materialize if a portfolio is forced to sell assets during periods of market dislocations due to a lack of available funding. However, this risk is often quantifiable, and if used prudently, financial leverage can arguably reduce the overall risk of the portfolio.

All else equal, the lower cost of financial leverage may allow for a portfolio to run less notional leverage and/or allow an investor to lever assets with more certain cash flows, such as mortgages or consumer-related assets that amortize over time. The difference in funding cost between non-recourse and recourse leverage can, at times, be several hundred basis points. Recourse leverage will also typically involve higher advance rates versus non-recourse options, with a borrower often able to secure an additional 10% to 25% of asset value. If the additional borrowing is simply retained as cash in the portfolio, the lower funding cost alone can improve levered return potential by hundreds of basis points. This may enable investors seeking enhanced returns to hold assets with more certain cash flows and potentially a less risky portfolio.

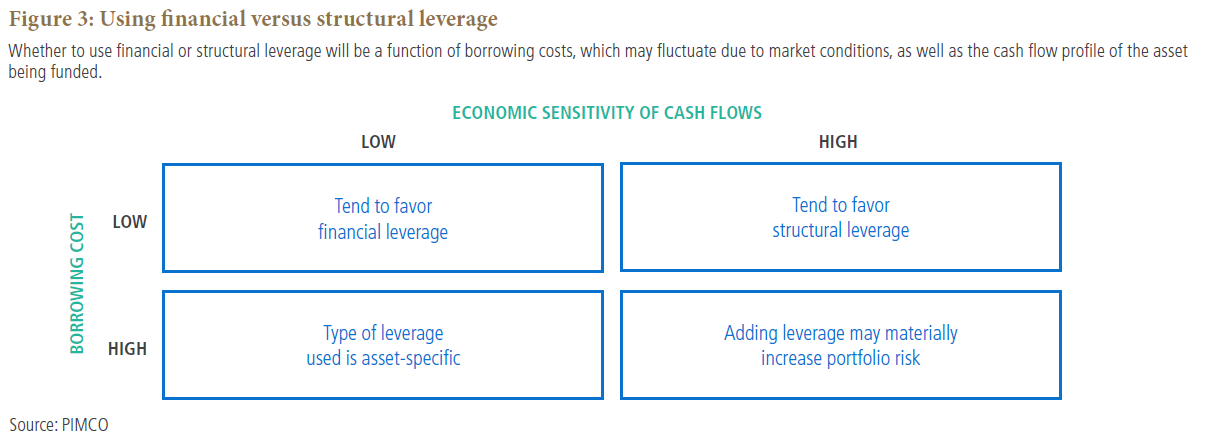

FINANCIAL VERSUS STRUCTURAL LEVERAGE

Changes in the market environment will shift the relative merits of using structural or financial leverage, whether at the asset or portfolio level, particularly as there are numerous inefficiencies in the funding market. This is something we believe can be prudently exploited by knowledgeable investors, based on underlying vehicle structure and liquidity provisions.

Interestingly, we often hear of strategies claiming they don’t employ financial leverage, almost as a “badge of honor.” Realistically, these strategies likely employ structural leverage in the form of equity investments and/or outsized directional economic bets. Yet as we described, if you are wrong on the overall economic direction, then the second and third order effects of leverage, could have a significant impact on a portfolio. Said another way, there is the potential for very high loss in structurally levered positions. For financial leverage there is the opportunity cost of having to sell a non-structurally levered position to meet a margin call. Of course, it should be noted that in volatile markets this could also result in portfolio losses.

KEY TAKEAWAYS ON THE SOURCES, RISKS AND BENEFITS OF LEVERAGE

When looking at any investment strategy and particularly alternatives strategies seeking enhanced returns, it’s imperative to understand the form of leverage being used, for in most instances, leverage will be there. When used prudently it is a way to deliver enhanced return potential in a world of low interest rates, but it also entails risks - which in some cases may be significant. Ultimately, and most importantly, an investor needs to understand the cash flow profile and return volatility of the investment being levered, as the impact of leverage is simply a derivative of this distribution.

This article contains hypothetical scenarios. Hypothetical and simulated examples have many inherent limitations and are generally prepared with the benefit of hindsight. There are frequently sharp differences between simulated results and the actual results. There are numerous factors related to the markets in general or the implementation of any specific investment strategy, which cannot be fully accounted for in the preparation of simulated results and all of which can adversely affect actual results. No guarantee is being made that the stated results will be achieved.

All investments contain risk and may lose value. The use of leverage may cause a portfolio to liquidate positions when it may not be advantageous to do so to satisfy its obligations or to meet segregation requirements. Leverage, including borrowing, may cause a portfolio to be more volatile than if the portfolio had not been leveraged. Derivatives may involve certain costs and risks, such as liquidity, interest rate, market, credit, management and the risk that a position could not be closed when most advantageous. Investing in derivatives could lose more than the amount invested. Prospective investors in alternative products are advised that investment in these products are suitable only for persons of adequate financial means who have no need for liquidity with respect to their investment and who can bear the economic risk, including the possible complete loss, of their investment.

There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market. Investors should consult their investment professional prior to making an investment decision.

This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed.

© PIMCO

© PIMCO

Read more commentaries by PIMCO