SUMMARY

- Delivering sustainable investment returns includes evaluating whether business models that are competitive today will be competitive in the future.

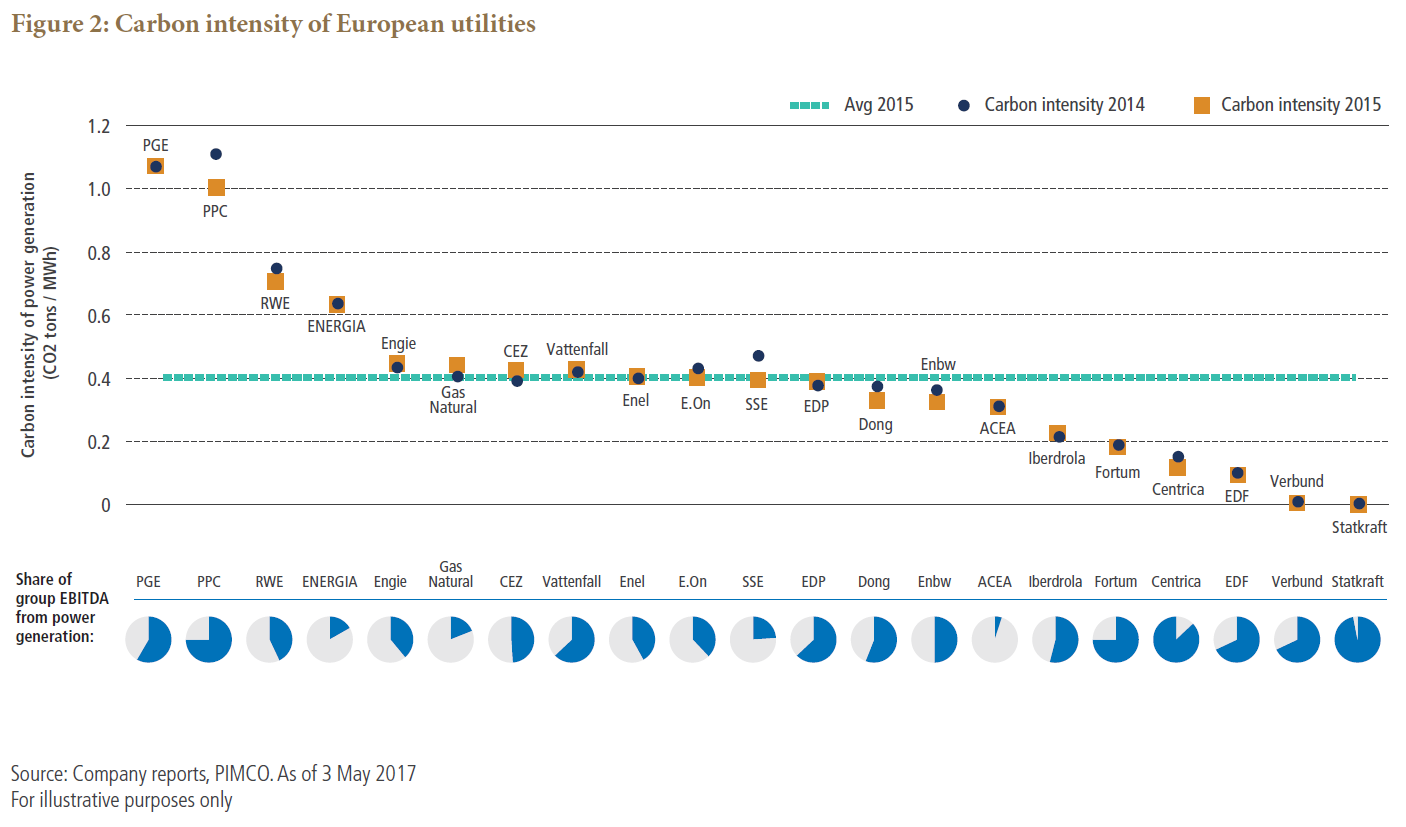

- In the European utilities sector, many of the challenges companies face are directly connected to ESG-driven changes in the market.

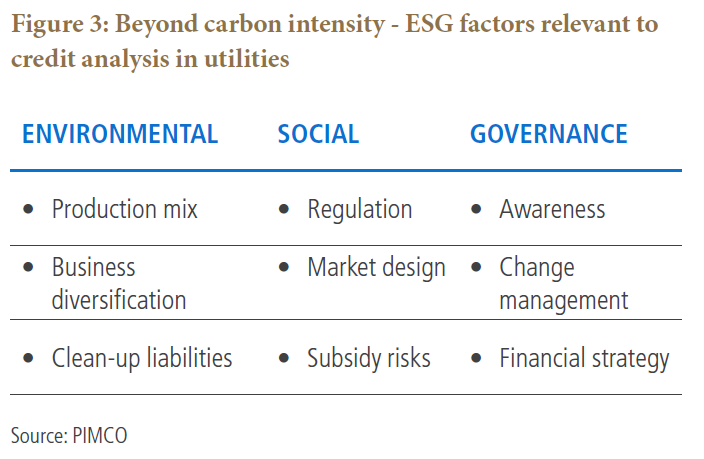

- Credit research in this sector requires looking beyond carbon intensity to understand the full spectrum of ESG issues facing firms.

PIMCO credit analyst Christian Schuetz discusses the Environmental Social and Governance (ESG) factors he looks at when evaluating the European utilities sector, and why understanding these is critical for thorough credit analysis.

Q: Why is it important to integrate ESG factors in credit analysis?

A: The idea of incorporating ESG factors in an investment process has been growing in importance and is a trend that looks set to stay. In part this reflects increased demand from investors who seek more than just financial return, and wish to align themselves with processes that reflect this. But it also makes good investment sense.

At PIMCO, we seek to deliver risk-adjusted returns for our clients in a manner that is sustainable over the long term. That means making sure that the investments we make on their behalf represent business models that are competitive not only today but well into the future, and this requires looking at ESG. In European utilities for example, which is the area I focus on, many large vertically integrated companies are facing big challenges as a result of structural changes in the market. Most of these changes are directly connected to "E", "S" or "G".

Q: Can you provide an example of how ESG factors have influenced an issuer's credit quality?

A: A good example of this is RWE, a German-based vertically integrated utility, which has seen its credit rating fall from BBB+ in 2014 to BBB- today. A combination of falling power prices, dependence on conventional power, and policy and regulatory headwinds, led to asset write-downs at the firm. A shift in strategy and a split of the company into two separate entities followed (see Figure 1).

All of this had important implications for bondholders. Not only did credit quality deteriorate over the period, but the split of the company ushered in a divergence in rating between RWE (the group containing the old thermal power assets) and Innogy (the new company containing grid, retail and renewables businesses). Senior unsecured bonds transferred to Innogy, but subordinated hybrid bonds remained at RWE.

This meant that investors in the senior unsecured bonds were able to benefit from the lower carbon intensity of the new company and from the improvement in the environmental risk profile of the credit.