“Washington – A gauge of U.S. business prices rose to the highest level in five years, another sign inflation pressure is picking up across industries.”

. . . The Wall Street Journal (5/12/17)

Some inflation numbers were reported last week. They read: April PPI jumped 0.5% month/month, +2.5% year/year; +2.2% year/year was expected. Meanwhile, core PPI increased by 0.4% month/month, +1.9% year/year; +0.2% month/month and +1.6% year/year were expected. The inflation report reminded us of something Pippa Malmgren (a policy consultant to numerous presidents) said to us at a recent national conference. She opined that when inflation goes from 1% to 2.5%, or maybe even 3.0%, it’s a really big deal; and we agree. Shortly after parsing those inflation figures I read something about the El Niño that is expected to “hit” in the back half of 2017. As paraphrased from the eagle-eyed David Lutz’s blog “What Traders Are Watching,” (Jones Trading):

The headline read, “Full-Fledged El Niño Increasingly Likely in Second Half 2017.” The U.S. government’s Climate Prediction Center (CPC) last month forecast El Niño conditions would prevail by the end of the northern hemisphere summer, but put the probability at only 50 percent. Most El Niño indicators have strengthened since then so the probability is likely to be revised higher when the CPC issues its next forecast later in May. Aussie’s wheat crop could see further drought damage. Sugar cane will also be impacted. Dryness in Southeast Asia could depress harvest levels of crops including rice and sugar in Thailand, Robusta coffee in Vietnam, and will add stress to rubber and palm oil trees in Indonesia and Malaysia. El Niño has also been linked to a weaker Indian monsoon and lower than average rainfall could affect crops including rice, wheat, cotton, and sugar. Indian farmers are large buyers of gold, and analysts at UBS last year raised concerns that a potential weak monsoon could hit purchases of the precious metal. El Niño has tended to impact cocoa production in West Africa. Meanwhile, Peru’s anchovy catch is almost always affected by the weather event, and is the main ingredient for fishmeal.

Interestingly, this “fishmeal” inference made me recall that a severe El Niño was responsible for the term "core inflation," which excludes food and energy prices in its inflation figures for those of you who don't eat or drive. We like this story:

It was in the early 1970s when an El Niño weather pattern caused torrential rains in Chile. Those rains caused Chile's Atacama Desert, the driest non-polar region in the world, to turn to mud. Since said desert lies between the Andes Mountains where copper is mined, and the Pacific coast, the copper could not be transported to Chile's ports, causing copper prices to surge. Further exacerbating the inflationary bias, the rain runoff spilled into the Humboldt Current. The Humboldt Current flows from the southern tip of Chile to northern Peru and extends about 1000 klicks off the coast into the Pacific Ocean. It is also responsible for about 25% of the world's "fish catch," mainly consisting of sardines and anchovies. For the uninitiated, those fish have many uses, like being dried and then crushed to be used in animal feed. The heavy rain runoff changed the saline content in the Humboldt Current causing the "fish catch" to collapse, which sent the price of feed stock for animals soaring with a concurrent rise in the price of beef, hogs, etc. At the same time OPEC was jamming “up” the price of crude oil with the OPEC oil embargo. A stumped Arthur Burns, then chief of the Federal Reserve, consequently asked his minions how to remove the price of food and energy from the inflation figures. P-r-e-s-t-o, "core inflation" was born, which excludes the costs of food and energy.

The impact of these La Niña/El Niño weather effects are not an unimportant point, for as Tony Heller notes:

“There are ominous signs that the earth’s weather patterns have begun to change dramatically and that these changes may portend a drastic decline in food production with serious political implication for just about every nation on earth. The [subsequent] drop in food output could begin quite soon, perhaps only ten years from now.”

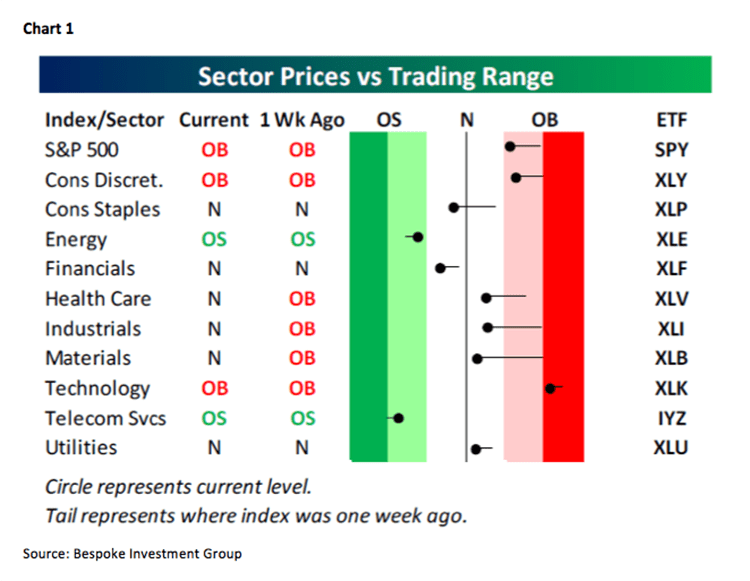

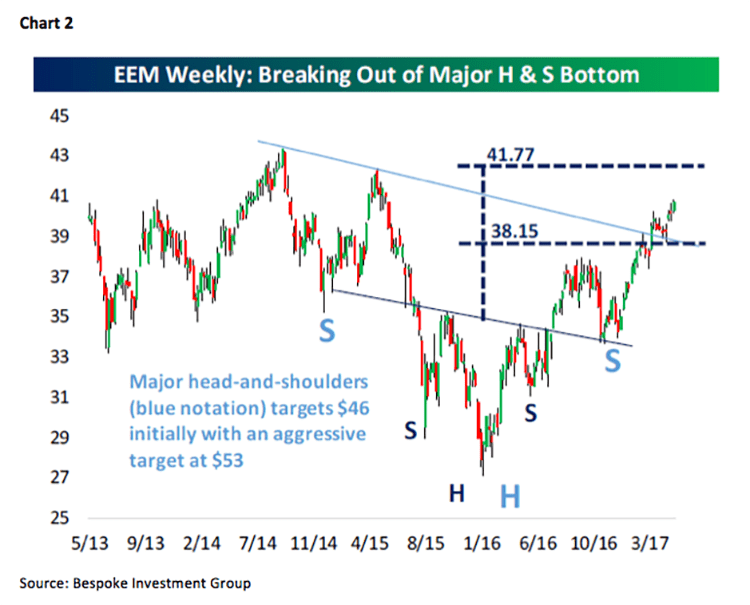

Speaking of “drops,” the “drop” in the price of crude oil looks to be over to us and we are tilting portfolios appropriately. The individual stock of choice our models like, and our fundamental analysts have a positive rating on for this energy theme, is Genesis (GEL/$31.43/Outperform). In fact, looking at the sectors, the only two that are oversold are the Energy and Telecom sectors (see chart 1, below). Also of interest is that the emerging markets appear to have bottomed and in the process have formed a reverse head-and-shoulders bullish chart formation (see chart 2 on page 3).

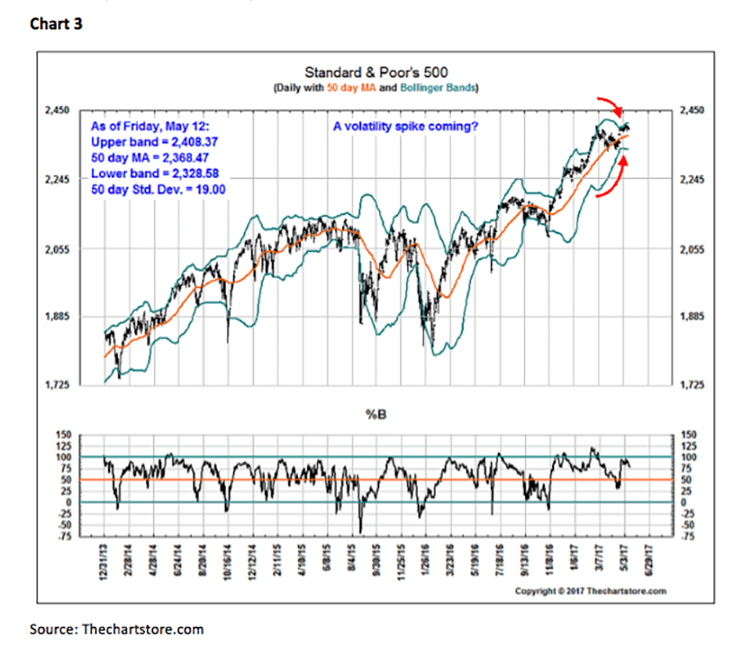

The call for this week: I am in Nevada and California speaking at events for our financial advisors and their clients this week, so this is being written on Sunday night without the benefit of the preopening futures. Our models suggest the drop in equity prices ended on April 19th with another breakout to new all-time highs slated to begin late this week. Early this week has the potential for some further stock price weakness, but by late week that potential weakness should abate. The compression of the Bollinger Bands, like our models, are telegraphing the potential for a pickup in volatility (chart 3 on page 3), which we think will come on the upside beginning late this week or early the following week. While our models are not always right, they are right more times than they are wrong and hereto we are tilting portfolios accordingly. Meanwhile, the transition to an earnings-driven secular bull market is in full swing with 61.6% of companies reporting earnings beating the consensus estimates and 63.1% bettering revenue estimates.