All Asset All Access, May 2017

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsRob Arnott, founding chairman and head of Research Affiliates, discusses why the PIMCO All Asset and All Asset All Authority funds’ ambitious, inflation-based secondary return benchmarks still make sense; Omid Shakernia, senior vice president of asset allocation, provides insight into how Research Affiliates’ proprietary business cycle modeling is informing asset allocation decisions; and Chris Brightman, chief investment officer, discusses why emerging market valuations still look favorable despite the recent strong rally in EM stocks. As always, their insights are in the context of the PIMCO All Asset and All Asset All Authority funds.

Q: The PIMCO All Asset and All Asset All Authority funds have secondary benchmarks of Consumer Price Index (CPI) +5% and CPI +6.5%, respectively. Are these return aspirations still realistic?

Arnott: Before delving into our return outlook, let’s discuss how we view our CPI benchmarks. Admittedly, these secondary benchmarks are unusual and differ from more traditional index-based benchmarks. From a market peak, they are stretch goals, and tough to achieve; from a market trough, they should be far easier to achieve. Importantly, I’m referring to a peak or trough for Third Pillar assets (diversifying markets – real assets, emerging markets and high yield bonds), which are at the heart of the All Asset strategies, not for more conventional stocks! We’ve just finished the first year of a bull market in Third Pillar assets after a challenging three-year bear market. So, we’re closer to a trough than a peak. In short, I do not think these CPI-based benchmarks should be difficult to reach from current Third Pillar market valuation levels.

The same cannot be said for conventional U.S. stocks and bonds. U.S. stocks are entering the ninth year of a bull market and recently reached a Shiller P/E ratio of 29, a valuation level seen in only two other periods over the past 140 years: just before the stock market crash in 1929, and during the tech bubble from 1998–2001. That’s it.

Sadly, many U.S. pension funds – and investors’ IRA and 401(k) portfolios – are counting on earning about a 5% real return, over and above inflation, to meet their financial needs in retirement.1 In a world of meager bond and stock market yields, most mainstream programs will likely fall far short of this goal. We estimate that a 60/40 U.S. stock/bond portfolio (i.e., 60% S&P 500 Index and 40% Bloomberg Barclays U.S. Aggregate Bond Index) is currently priced to deliver CPI +0.9% (about 3% including inflation) and has less than a 1% chance of delivering CPI +5% in the coming decade.

Last fall, we ran a “5% Challenge”1 that invited people to try to create a hypothetical portfolio that could give them a decent likelihood of CPI +5% over the coming decade. More than 60,000 people have explored it, but surprisingly few (just over a thousand as of 1 May) have met the challenge. It’s actually not hard to design a portfolio with the potential to deliver CPI +5%, at least not for those willing to think way outside of the mainstream. Suppose we start with a 60/40 portfolio allocation but abandon the expensive U.S. markets. Let’s split the 60% stock portion into half Europe, Australasia and the Far East (EAFE) and half emerging markets (EM) and split the 40% bond portion into half EM local currency bonds and half U.S. high yield. Based on current valuations and our forward-looking asset class return assumptions, we’d estimate this portfolio to earn CPI+5.1% over the long term.

And that’s without any additional alpha potential. For example, within the context of the All Asset suite, sources of alpha include PIMCO’s active management of the underlying funds (including alternative approaches to generating alpha, such as the portable alpha strategies employed in PIMCO’s StocksPLUS suite) and the systematic active approach employed by the RAE equity strategies, as well as our active asset allocation decisions. The hypothetical return also doesn’t take into account the return potential available from employing leverage, a tool available to the All Asset All Authority Fund, at a modest cost of roughly Libor +1%. (Please note this is a hypothetical portfolio utilizing return forecasts; it may or may not reflect actual future results, and estimated volatility would exceed that of a mainstream 60/40 portfolio.)

Despite this astonishing gap – by our estimates, less than a 1% real return for the U.S. 60/40 investor and over 5% real return for the unconventional non-U.S. 60/40 investor – most people are loath to pry their money away from these so-called safe haven markets, let alone to deploy more money into Third Pillar markets (especially after the daunting bear market of 2013–2015!). It bears mentioning that anything newly expensive will probably have wonderful past returns, and anything newly cheap will have been recently disappointing. This is why buying low and selling high is difficult.

Let’s turn to how our strategies have performed. Since its launch, the All Asset Fund has achieved marginally below its 5% real return target, within the rounding error. The All Asset All Authority Fund has fallen short of its 6.5% real return target, but we remain confident in its future prospects. All Authority was designed to shine in weak and turbulent equity markets; it’s a diversifier for when investors desperately need diversification. During its 13-plus-year history, we’ve seen 12 steady bull market years and only about 18 months of weak and turbulent markets (in 2008–2009 and briefly in 2011). Importantly, the All Asset suite delivered real returns while diversifying away from mainstream stocks and bonds, in line with our mission to be a true diversifier.

Interestingly, a lot of investors asked the same question about our CPI-based benchmarks about four years ago. Back then, most asset classes were fully priced and expensive. In that environment, we acknowledged that our CPI+ benchmarks were stretch goals. But after a grueling three-year Third Pillar bear market (and five years for EM stocks and currencies!), the tide seems to have turned. Even after a 25% rebound from the January 2016 lows, we believe our core Third Pillar investments are still cheap relative to First and Second Pillar assets. From this starting point, our outlook for achieving these return targets has considerably improved.

Looking forward, what gives us confidence in our potential to achieve our secondary return targets over the coming decade? Consider a few time-tested sources of added value. First, we seek to counter headwinds in the form of low yields and forward-looking returns by using a deep toolkit of liquid asset classes. Second, our strategies rely on excess returns arising from manager skill and from structural alpha. And finally, we seek incremental return by tactically shifting assets into recently out-of-favor markets offering premium yields, trading against the market’s most extreme bets.

Thinking of our CPI benchmarks from a long-run, outcome-oriented perspective (rather than through a benchmark-constrained lens) is more in keeping with the mission and design of our portfolios. In line with our dynamic, contrarian strategy, we flexibly shift the portfolio’s prospective mix and risk posture based on market conditions to reflect our view of the best long-term risk-to-reward opportunities across a global set of asset classes.

It’s comfortable to be an index-hugger and a crowd-follower. But we deliberately accept the short-term pain and discomfort that accompany maverick risk, knowing that markets tend to reward neither comfort nor performance-chasers in the long run. By design, benchmarks do not dictate our decisions.

Q: A distinguishing element of Research Affiliates’ allocation models is your proprietary business cycle modeling. How does that inform asset allocation decisions, and what is it saying today?

Shakernia: We’ve discussed at length the well-documented empirical evidence across capital markets linking asset class valuations to long-term returns. Within the All Asset suite, starting yields and long-horizon mean reversion form the basis of our strategic allocations, informing our decisions on what to own. The purpose of our business cycle model is to calibrate the asset class yields and valuations with the state of the macro economy to help shape our short-term (one-year) expected returns. This calibration of yields and valuations via the business cycle model forms the basis of our tactical allocations, informing our decisions on when to trade.

Contrarian, value-oriented investment strategies have a well-known tendency to be early – both in buying when asset prices fall (prices may continue to fall if economic conditions are deteriorating) and in selling when prices rise (prices may continue to rise when macroeconomic conditions are improving). A key benefit of the business cycle model is that it allows us to counterbalance this tendency to be early – and potentially harvest additional returns – by identifying the macroeconomic conditions that justify lower valuations in bad times and higher valuations in good times.

For example, when valuations fall and the economy is deteriorating, the business cycle model might indicate higher-than-average investor risk aversion, which justifies the falling valuations over the short run and tempers our enthusiasm for cheap valuations. Similarly, if an asset class has experienced strong returns, but the economy is continuing to improve, our business cycle model highlights the rising risk tolerance of the marginal investor and will encourage us to wait before taking profits. In many ways, the effect is similar to incorporating a momentum overlay on a contrarian strategy.

In a 2002 paper,2 Tarun Chordia and Lakshmanan Shivakumar showed that momentum strategy returns can be explained by the business cycle, and that payoffs to momentum strategies disappear once returns are adjusted for their predictability based on the macroeconomic variables. By incorporating the business cycle directly, rather than using a simple momentum overlay, we get the benefit of tempering our contrarian strategy’s tendency to be early while at the same time basing our views on the fundamental macroeconomic drivers of shorter-term market returns.

The theoretical foundation of our business cycle model is the consumption habit model developed by John Campbell and John Cochrane (as laid out in their 1999 paper3), which relates investors’ desire and capacity to accept more or less risk to the difference in consumption growth (or decline) and recent trend growth (or decline). In the Campbell/Cochrane model, the consumption habit is “slower-moving” and may fluctuate less than consumption itself, which can vary more widely with the growth cycle. When consumption declines, risk aversion tends to rise – people in general don’t want to drop below a certain baseline level of “habitual” consumption they’ve grown used to. As a proxy for aggregate consumption growth and habits, we measure deviations of economic growth from the recent GDP trend.

The turning points of these cyclical deviations determine growth periods (when growth is accelerating relative to trend) and slowdown periods (when growth is decelerating relative to trend). Consistent with the theory, the growth cycles capture a wide array of empirical relationships across capital markets, including the pro-cyclical variation of valuations (Shiller P/E ratios tend to be lower and credit spreads wider in slowdown periods) and the counter-cyclical variation of risk (volatilities and correlations tend to be higher in slowdown periods).

Since the turning points in the business cycle can only be determined several months after they have occurred, our model includes a forecasting component to gauge the probability of a transition to a slowdown period in the next quarter. This forecast is based on proprietary leading indexes consisting of both economic activity and monetary policy indicators.

To capture the dispersion in macroeconomic conditions across the globe, our business cycle model consists of slowdown probability forecasts for 10 developed market and 10 emerging market countries. Finally, we measure the sensitivity of asset class valuations to changes in our forecasts, allowing us to calibrate our tactical allocations. These tactical views are based on adjustments to both expected return (through adjustments to asset class fair valuations) and to risk (through adjustments to volatilities and correlations) across the business cycle.

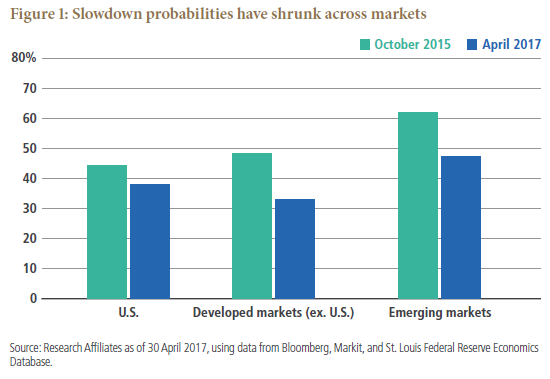

Looking at business cycle conditions across the globe today, we see that the U.S. and the average of developed market economies currently have slowdown probabilities of about 38% and 33%, respectively, drops of 5% and 15%, respectively, over the prior 18 months (see Figure 1). These levels are consistent with the improving economic conditions we’ve experienced recently, with leading indicators pointing to more of the same for the next quarter. The story in emerging markets is even better, and is not widely recognized. The average of EM slowdown probabilities is at a neutral reading of just under 50%, but the slowdown probability has dropped by roughly 15% over the past 18 months.

These materially improving economic conditions support the rising valuations we’ve seen recently. Even with the strong one-year returns in EM equities, our business cycle model is countering the contrarian tendency to take profits too early. Given these attractive valuation levels, if economic conditions in EM countries continue to improve, the case for diversifying away from mainstream assets would become even more compelling.

Q: Has the rationale behind your emerging markets positioning changed, given the strong rally in EM stocks?

Brightman: In February 2016, we suggested that EM equities might represent “the trade of a decade.” Since then, their strong rebound4 has prompted many to ask us whether this rally has run its course.

Not even close. While recent positive price momentum has put a small dent in our forward-looking return estimates, EM stocks remain an enormous bargain, in our view. EM stocks trade at attractive discounts, both relative to the global equity opportunity set and relative to their own historical levels. Further, the market environment has now turned more supportive.

When we scan global capital markets, we find that the securities with the highest prospective real returns are located in countries afflicted by fear and uncertainty. Consider today’s cheapest market: Russia. Exhibiting a cyclically adjusted price-to-earnings (CAPE) ratio of only 5x, the Russian market would likely produce a real return approaching 12% per year over the coming decade, according to our forecast – albeit with very high risk around that point estimate. For Turkish stocks, priced at a CAPE of 10x, we estimate an 8% annualized long-term real return. In stark contrast (and as Rob mentioned above), U.S. stocks priced at a CAPE of 29x – the highest since the U.S. tech bubble – offer an annualized long-term real return of less than 1%.

We’ve regularly mentioned the strong relationship between starting yield and long-term, prospective return.5 Let’s define starting equity market yield as the ratio of 10-year trailing real earnings per share divided by current price. Since 1990, the correlation between this yield premium or discount of EM stocks to U.S. stocks and their subsequent 10-year excess return has been a remarkable 96%. The yield premium of EM stocks over U.S. stocks reached 151% in January 2016 and was still huge, at 134%, at the end of March 2017. Using history as a guide – and noting, of course, that past performance is not a guarantee or reliable indicator of future results – the current premium would imply a 10-year annualized excess return for EM equities relative to U.S. equities of 8.2%.

Not only are EM stocks still trading at cheap levels relative to U.S. stocks, they are also trading cheap relative to their own history. As of 31 March 2017, the starting yield for EM stocks stood at 8.1%, near the cheapest 15th percentile of the historical range and far above its historical average yield of 5.6% over the past 25 years. In a world starved for yield, EM equities remain compelling.

Finally, the market environment has turned more supportive for EM. Factors beyond valuation supporting EM assets include depressed currencies, strong price and economic momentum, and improving fundamentals. (My colleagues have discussed this subject in more detail in a previous paper6).

Today’s historically attractive valuations, coupled with favorable market conditions, give us increased confidence in our positioning. We think now is an unusually compelling time to diversify investments away from mainstream assets to exploit attractive relative valuations and thereby position for much higher potential long-term real returns.

The All Asset strategies represent a joint effort between PIMCO and Research Affiliates. PIMCO provides the broad range of underlying strategies – spanning global stocks, global bonds, commodities, real estate and liquid alternative strategies – each actively managed to maximize potential alpha. Research Affiliates, an investment advisory firm founded in 2002 by Rob Arnott and a global leader in asset allocation, serves as the sub-advisor responsible for the asset allocation decisions. Research Affiliates uses their deep research focus to develop a series of value-oriented, contrarian models that determine the appropriate mix of underlying PIMCO strategies in seeking All Asset’s return and risk goals.

Further reading

Recent editions of All Asset All Access offer in-depth insights from Research Affiliates on these key topics:

- Active investment management (April 2017)

- Where conventional wisdom may be making mistakes in today’s market (March 2017)

- Contrarian strategies to enhance real return (February 2017)

- Long-term asset class forecasts (January 2017)

- Potential investment implications of Trump presidency (December 2016)

- Introducing Chris Brightman as co-PM on All Asset funds (November 2016)

© PIMCO

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All