We have a big economic calendar and potential Fed news. Those stories will take a back burner this week. My safest prediction is that we are about to see a new rash of China experts both in print media and on CNBC! These freshly-minted pundits will be asking:

What will the Trump-Xi meeting mean for the economy, and for stocks?

Last Week

Last week the news was mostly positive, but light. Markets continued the attention to the Trump Administration’s next policy steps – especially the chances for tax reform.

Theme Recap

In my last WTWA I predicted a discussion about the aftermath of the ACA repeal decision. That was a good call, as assorted pundits explained what the next policy moves might be. The more adventurous speculated about whether the Freedom caucus would block changes in the debt ceiling or tax reform. Some of that discussion will continue in the early part of next week.

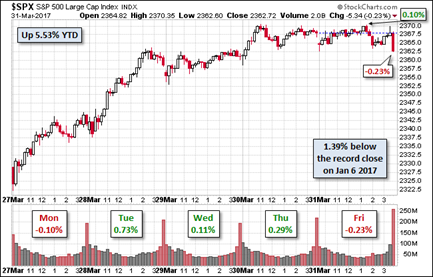

The Story in One Chart

I always start my personal review of the week by looking at this great chart from Doug Short via Jill Mislinski. She notes the overall weekly gain of 0.80% and the quarter one increase of 5.5%. The biggest takeaway might be the general rebound from last week’s market reaction to the failure of the ACA repeal.

Doug has a special knack for pulling together all the relevant information. His charts save more than a thousand words! Read his entire post for several more charts providing long-term perspective, including the size and frequency of drawdowns.

The News

Each week I break down events into good and bad. Often there is an “ugly” and on rare occasion something very positive. My working definition of “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

This week’s news was slightly positive.

The Good

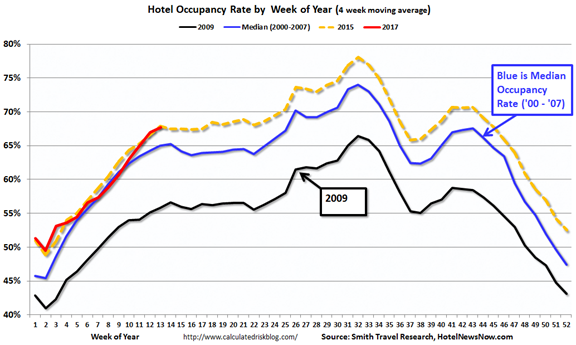

- Hotel occupancy is strong. Calculated Risk reports interesting hard data from private sources. These are items you might not see elsewhere.

-

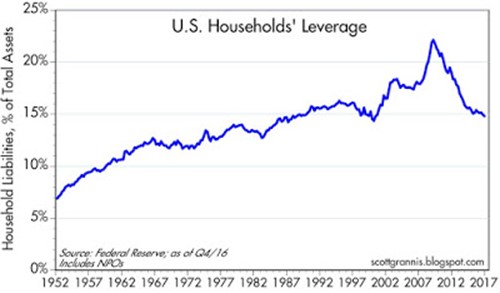

Household finances are on “solid ground” as explained by Scott Grannis. Debt levels as a percentage of disposable income are at 30-year lows. He provides an interesting chart of household leverage.

-

Serious delinquencies have declined to 1.19% (Fannie Mae via Calculated Risk). This is the lowest level in nine years.

-

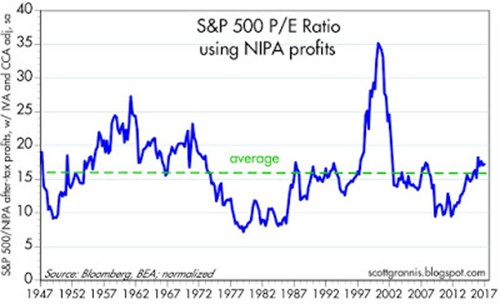

Corporate profits remain strong, increasing 9.3% year-over-year in Q416. New Deal Democrat has a good account of the trends, why National Income and Profit Accounts (NIPA) come so late, and how he estimates this series in advance. Scott Grannis has a similar report which also shows the relationship between NIPA profits and stocks. It is dramatically different from the popular valuation charts.

-

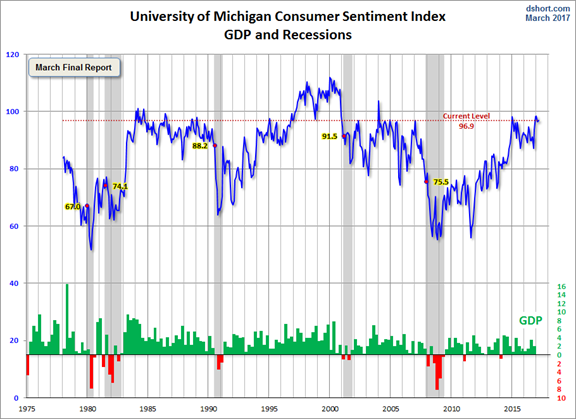

Michigan consumer sentiment remained strong, increasing to 96.9. Jill Mislinski has the update. It includes an interesting excerpt from the Survey of Consumers chief economist, Richard Curtin. He notes that expectations and partisanship are influencing the outlook. This bears watching. Jill also has this fine chart.

-

Q4 GDP revisions edged a little higher than expected to 2.1%

-

Pending home sales increased 5.5%. CNBC’s Diana Olick has an interesting report, noting that sales would be much higher if there were more inventory. She has an interesting interview from Denver, where construction is 50% behind the pace needed. Builders blame the lack of labor, especially illegal immigrants frightened by recent policy changes. The builder interviewed stated that the jobs were not desirable for most U.S. workers.

This report, if accurate and typical, has implications for homebuilders, Fed policy (labor market tightness), and immigration policy. You need to watch the video to see the key points.

The Bad

-

Personal consumption spending missed expectations. The increase was only 0.1% despite an income increase meeting expectations of 0.4% growth. Steven Hansen (GEI) has a thorough analysis with excellent tables and charts.

-

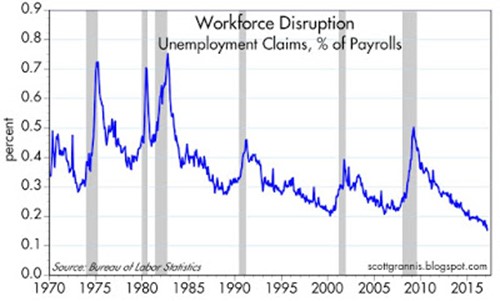

Jobless claims moved slightly lower, to 258K, but the four-week moving average moved higher. I am scoring this as “bad” because the series has moved a bit higher from the best levels. Scott Grannis helps us to keep this in perspective with this interesting chart of claims compared to the labor force.

The Ugly

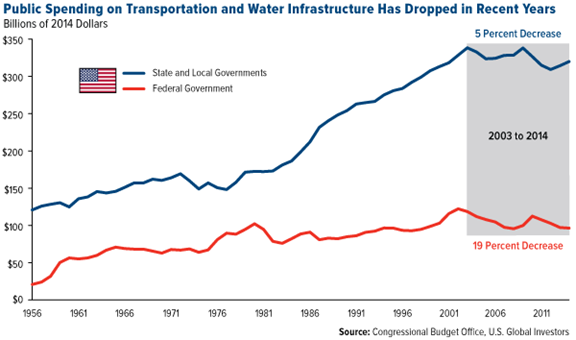

U.S. Bridges. (No, not the recent North American Bridge Championship, where Bill Gates had a nice win. While that particular event was limited to players with fewer than 10,000 masterpoints, it still included many experts. It was a nice victory, and his best career result). Turning back to actual structures, the American Society of Civil Engineers (ASCE) notes that 40% of bridges are more than fifty years old. Over the next twenty-five years the U.S. is short of needed spending by about $3 trillion.

The Silver Bullet

I occasionally give the Silver Bullet award to someone who takes up an unpopular or thankless cause, doing the real work to demonstrate the facts. No award this week, but nominations are always welcome. There are many bogus claims and charts out there! I wrote about headline spinning last week, and the misleading recession forecasts that resulted. We should all encourage astute analysts to help on this front!

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react. That is the purpose of considering possible themes for the week ahead. You can make your own predictions in the comments.

The Calendar

We have a very big week for economic data, featuring the most important reports.

The “A” List

- Employment report (F). Expectations are in the 180K range, down from last month’s 235K

- ISM index (M). Continuing strength expected.

- Auto sales (M). The concept of “peak auto” has some recent buzz, drawing attention to this private data.

- ISM services (W). Wider scope than manufacturing, but a shorter history. Strength expected.

- FOMC minutes (W). Will be scrutinized for hints about the pace of future rate hikes.

- Initial jobless claims (Th). Is the series edging up from record low levels?

The “B” List

While the schedule is not as heavy as last week, FedSpeak will be featured on several days.

The Thursday meeting between President Trump and China’s President Xi Jinping could be extremely important for economic policy and the markets.

Next Week’s Theme

This is a big week for economic data. We could usually expect daily analysis of the news, focusing on the Friday employment data. A secondary theme might be the emerging change in Fed policy, with speakers and the release of minutes on Wednesday.

Not this week! The visit of Xi Jinping and the meetings at Mar-a-Lago have significance extending beyond recent economic news. The commentary next week will raise the question:

What will the Trump-Xi meeting mean for the economy and stocks?

No one knows what will happen. The best we can do is collect relevant facts and decide what to watch for. Here is some key background.

-

Trump is advertising a “tough” meeting. Quartz suggests the reasons and key issues:

He is sure to be coached by hardline China advisor Peter Navarro, who believes China is full of cheating thieves, intent on global domination. After Trump’s allegations that China had stolen jobs and a way of life from America’s middle class on the campaign trail, the stage seems set for a clash. Sensitive topics could include the trade imbalance, China’s over-production of steel, North Korea’s increasing militarization, and Beijing’s insistence that it control the South China Sea, in defiance of international law. American CEOs are worried that the wrong move could destabilize the relationship and harm the US economy.

-

Xi is the most powerful and popular Chinese leader in decades. He is dismantling the “collective leadership” approach. The Economist explains and questions whether this will lead to needed reforms. After describing his takeover of key committees and battle against corruption, the article focuses on his mission:

All of this helps Mr Xi in his twofold mission. His first aim is to keep the economy growing fast enough to stave off unrest, while weaning it off an over-dependence on investment in property and infrastructure that threatens to mire it in debt. Mr Xi made a promising start last November, when he declared that market forces would play a decisive role (not even Deng had the courage to say that). There have since been encouraging moves, such as giving private companies bigger stakes in sectors that were once the exclusive preserve of state-owned enterprises, and selling shares in firms owned by local governments to private investors. Mr Xi has also started to overhaul the household-registration system, a legacy of the Mao era that makes it difficult for migrants from the countryside to settle permanently in cities. He has relaxed the one-child-per-couple policy, a Deng-era legacy that has led to widespread abuses.

-

Chinese strategy is to reach Trump through his family. The FT describes the background.

China seems to have grasped that the best way to influence Mr Trump is via his family. Chinese diplomats have gone out of their way to court Mr Kushner and Ivanka Trump, who were their guests of honour at the Chinese new year celebration in February. China has also looked favourably on Mr Trump’s business. Since his inauguration it has approved dozens of pending trademark applications by The Trump Organization. The volume of applications to market Ivanka Trump’s brand in China has also soared. This week, Kushner Companies — the family property group from which Jared has stepped back — ended talks to sell a prime piece of Manhattan real estate on very favourable terms to Anbang, a Chinese company, after members of Congress alleged a conflict of interest.

-

Possible outcomes. The FT continues with the range of what we might expect.

At one extreme, Mr Trump could threaten to carry out his campaign vow to impose a 45 per cent tariff on Chinese imports — a step that would provoke a global trade war and fall foul of the World Trade Organisation. That would produce a similar outcome to Mr Trump’s rancorous meeting with Angela Merkel last month, in which he presented her with a massive invoice for Germany’s defence costs. At the other extreme, Mr Xi could package a few Chinese investments into easily tweetable jobs announcements. Last year China invested a record $45bn in the US — mostly in real estate, finance and entertainment.

What does this all mean for investors? As usual, I’ll have a few ideas of my own in today’s “Final Thought”.

Quant Corner

We follow some regular featured sources and the best other quant news from the week.

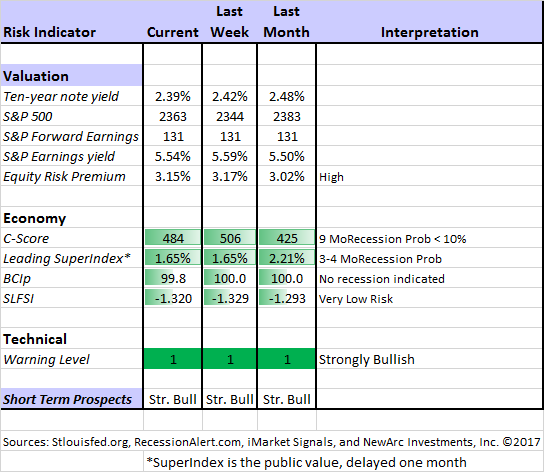

Risk Analysis

Whether you are a trader or an investor, you need to understand risk. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update.

The Indicator Snapshot

The Featured Sources:

Bob Dieli: The “C Score” which is a weekly estimate of his Enhanced Aggregate Spread (the most accurate real-time recession forecasting method over the last few decades). His subscribers get Monthly reports including both an economic overview of the economy and employment. (see below).

Holmes: Our cautious and clever watchdog, who sniffs out opportunity like a great detective, but emphasizes guarding assets.

RecessionAlert: Many strong quantitative indicators for both economic and market analysis. While we feature his recession analysis, Dwaine also has several interesting approaches to asset allocation. Try out his new public Twitter Feed.

Georg Vrba: The Business Cycle Indicator and much more.Check out his site for an array of interesting methods. Georg regularly analyzes Bob Dieli’s enhanced aggregate spread, considering when it might first give a recession signal. His interpretation suggests the probability creeping higher, but still after nine months.

Brian Gilmartin: Analysis of expected earnings for the overall market as well as coverage of many individual companies. His most recent post notes that the expected growth rate in S&P earnings is now 8.41% — the highest level since October, 2014.

Doug Short: The World Markets Weekend Update (and much more). His Big Four chart is the single best method to monitor the key indicators used by the National Bureau of Economic Research in recession dating. The latest update now includes the real income data.

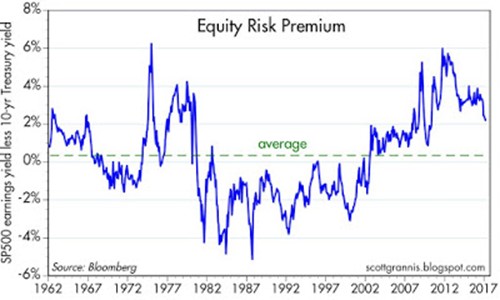

Scott Grannis writes this week about the equity risk premium, which I currently score as “high.” This means that I find stocks to be much more attractive the bonds. Here is Scott’s chart of this relationship. The above-average value is IMHO the best gauge of market sentiment – still negative on stocks versus bonds.

How to Use WTWA (especially important for new readers)

In this series, I share my preparation for the coming week. I write each post as if I were speaking directly to one of my clients. Most readers can just “listen in.” If you are unhappy with your current investment approach, we will be happy to talk with you. I start with a specific assessment of your personal situation. There is no rush. Each client is different, so I have eight different programs ranging from very conservative bond ladders to very aggressive trading programs. A key question:

Are you preserving wealth, or like most of us, do you need to create more wealth?

Most of my readers are not clients. While I write as if I were speaking personally to one of them, my objective is to help everyone. I provide several free resources. Just write to info at newarc dot com for our current report package. We never share your email address with others, and send only what you seek. (Like you, we hate spam!)

Best Advice for the Week Ahead

The right move often depends on your time horizon. Are you a trader or an investor?

Insight for Traders

We consider both our models and the top sources we follow.

Felix, Holmes, and Friends

We continue with a strongly bullish market forecast. All our models are now fully invested. The group meets weekly for a discussion they call the “Stock Exchange.” In each post I include a trading theme, ideas from each of our five technical experts, and some rebuttal from a fundamental analyst (usually me, but sometimes a guest expert). We try to have fun, but there are always fresh ideas. Last week the focus was on “Voodoo Chart Reading” inspired by Michael Kahn (see below).

Top Trading Advice

Like everyone else, I like reading about Jesse Livermore. He enjoys a reputation as a great trader despite multiple bankruptcies and a life ending in suicide. That certainly is one measure of success!

Joe Fahmy has a nice post highlighting Livermore trading rules from almost 80 years ago. Most still make plenty of sense. It would be a nice project for someone to analyze how these might be different under modern conditions. Out of the many rules I endorse, I especially like this one:

21. Few people ever make money on tips. Beware of inside information. If there was easy money lying around, no one would be forcing it into your pocket.

Brett Steenbarger remains at the top of trader “must-reads.” My favorite post this week is about trading resilience. Many traders do not recognize how negative factors can affect their work. You need the ability to bounce back.

Chartered Market Technician Michael Kahn uses the “Voodoo” word in discussing charts. He has a great post on what you can and cannot expect to learn from your chart study. I especially like his dismissal of the “death cross.”

First of all, the death cross occurs when the trend has already changed. That is the only way the math works, by the way, because the pattern is defined as the 50-day moving average crossing below the 200-day moving average. That cannot happen when prices are rising.

Anyway, in practice we often see the market bounce right as the cross happens. Why? Because typically it has been falling for a while already. Again, is has to be falling otherwise the short-term average cannot drop under the long-term average.

OK, Einsteins, I know we can make the math work with price spikes and outliers but roll with me here.

So, the market may be a bit oversold and it bounces. But overall the cross appeared because most likely something is wrong. Short of real voodoo telling us what’s what that is all we can hope from charts. They do not tell us what will happen. They are meant to give us clues as to what to do.

Insight for Investors

Investors have a longer time horizon. The best moves frequently involve taking advantage of trading volatility!

Best of the Week

If I had to pick a single most important source for investors to read this week it would be Michael Kitces great article, The Evolution Of The Four Pillars For Retirement Income Portfolios.He presents an excellent history of retirement needs and alternatives. He also analyzes the consequences of each of the current choices. I especially like this element of the conclusion, an issue that we frequently discuss with clients:

In fact, arguably when thinking about a retirement portfolio, it’s better to think in terms of “retirement cash flows” than retirement income, as what constitutes “income” for investment purposes (interest and dividends, but not principal) is different than what constitutes “income” for tax purposes (as interest and dividends might be tax-free coming from a Roth, while principal may be fully taxable if withdrawn from a pre-tax retirement account).

Nice work, with many great points. Please read the entire post.

Stock Ideas

David Fish has updated the list of dividend champions, challengers, and contenders. This is always a good source of ideas. This week he features McGrath RentCorp (MGRC) and includes some analysis from Chuck Carnevale.

Chuck is back with a deep dive on United Parcel Service (UPS). The quantitative metrics are solid, so he takes on the key concern – the challenges in business to consumer deliveries. This is a typically first-rate analysis.

Brian Gilmartin’s earnings-driven analysis still favors energy stocks. Like everyone else, we will be paying even more attention to Brian next week as earnings season begins.

Barron’s agrees with the energy theme, and also features Under Armour (UA) and Lowes (LOW).

Our Stock Exchange always has some fresh ideas. There are ideas from five different approaches. Felix, who is most aligned with long-term traders, likes Wynn Resorts (WYNN). The most recent post provides descriptions of each model. You will probably identify with one of the characters, and your questions are welcomed.

Lee Jackson has five “safe stocks” if you think the “Trump magic” has worn off.

Yield Plays

Blue Harbinger has some dividend ideas in health care.

Wade D. Pfau does a nice job in describing bond ladders. I especially like the rolling ladder, which we offer as a complement to higher-yielding programs. Anyone interested in safe yield, with the potential to grow with the market, should read this post.

Emerging Europe?

Frank Holmes opines that the time has come.

Personal Finance

Professional investors and traders have been making Abnormal Returns a daily stop for over ten years. If you are a serious investor managing your own account, this is a must-read. Even the more casual long-term investor should make time for a weekly trip on Wednesday. Tadas always has first-rate links for investors in his weekly special edition. As usual, investors will find value in several of them, but my favorite is this week’s best investment advice (see above). Other great posts included the question of whether you would prefer $1 million or $5000 per month for your retirement, and the pragmatic warning about making financial decisions on your smartphone.

In his regular column, Seeking Alpha Editor Gil Weinreich takes up yet another important topic – diversification and what is added by ETFs. He cites contributor Roger Nussbaum, who provides a balanced discussion of diversification, stock picking, concentrated portfolios, and recent strong opinions. A timely point for discussion.

Watch out for…

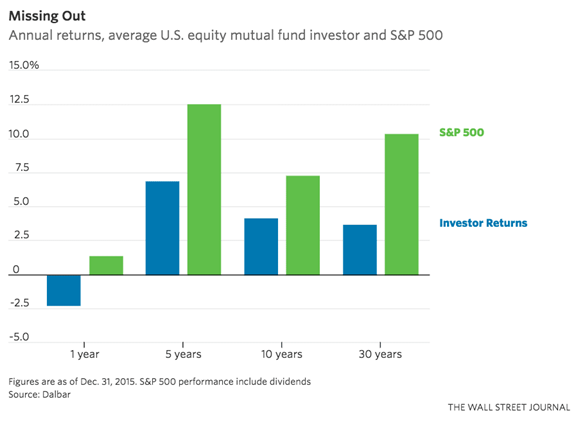

Costly but natural mistakes. Josh Brown cites data showing that investors significantly underperform market averages. Mostly this comes from psychological reactions, but some is also stock selection. The key chart is below. If you are lagging on your investment performance, please request (main at newarc dot com) my free report on the 12 Pitfalls for Individual Investors. It is a quick and easy test to see if you can profitably “fly solo.” Here is Josh’s chart:

Subprime auto. Steve Eisman warns. Barron’s also features a negative take on CarMax (KMX) for the same reason.

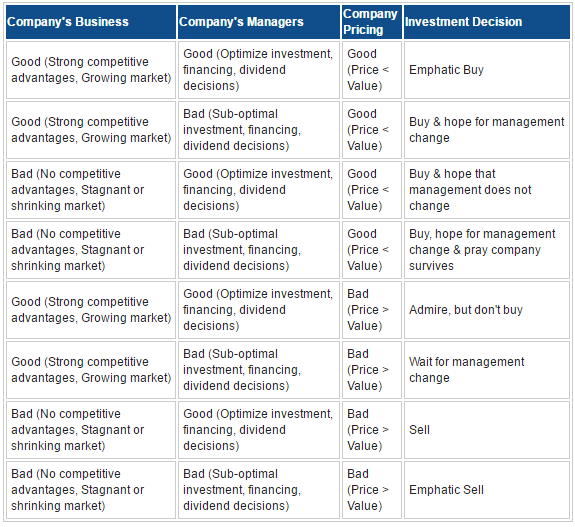

Good companies that are bad investments. Aswath Damodaran explains how to tell this difference. Here is the summary, which I strongly endorse!

Final Thoughts

A major change in leadership has everyone thirsting for information about possible policy changes. Stated positions from a candidate are not dependable. Those ideas might change once in office, or might prove infeasible. In the case of foreign policy, the range of possible results is especially wide. The President has a lot of flexibility, and many of the relationships have a personal quality.

This highlights the importance of this week’s Trump-Xi meeting. Like a top poker player, you should be looking for “tells” about true intentions, future policies, and the economic implications.

As is often the case, it is foolish to predict the specific outcome of these meetings. Readers sometimes expect a definitive answer to the week’s question in my “final thought.” That is not the mission of WTWA. I try to do two things:

- Explain what will be the focus in the coming week;

- Provide help with interpreting events.

It is important to recognize what you do not know, what is unknowable, and what is pure speculation. Pretending that you know a specific answer can be costly.

Given that setting, how can we prepare for this event? Most observers will be focused on specific policy implications. That is a mistake. I am interested in the following:

- Overall tone and friendliness. I do not expect any golf! This will be an early test of how foreign leaders, aggressively criticized by Trump during the election campaign, respond to him as President.

- Symbolic quality of the announced results. A tough line by the President? Some clear concessions by Xi?

- Common ground. Will there be an emphasis on issues like North Korea?

- Technical missteps. The China team consists of specialist on the specific issues – those who work only on these matters and have done so for years. The US team has dismissed the experts for a more general approach. Will this matter? Will it lead to blunders?

The most important consequence will be the implications for trade policy. One major viewpoint is that President Trump has engaged in tough talk to facilitate bargaining. The other is that he will instigate a trade war. Which is closer to the truth?

This week will provide the first hints. Stay tuned!

© NewArc Investments, Inc.

Read more commentaries by NewArc Investments, Inc.