“The Climb”

“There's always gonna be another mountain

I'm always gonna wanna make it move

Always gonna be an uphill battle

Sometimes I'm gonna have to lose” (Climb). . . Miley Cyrus

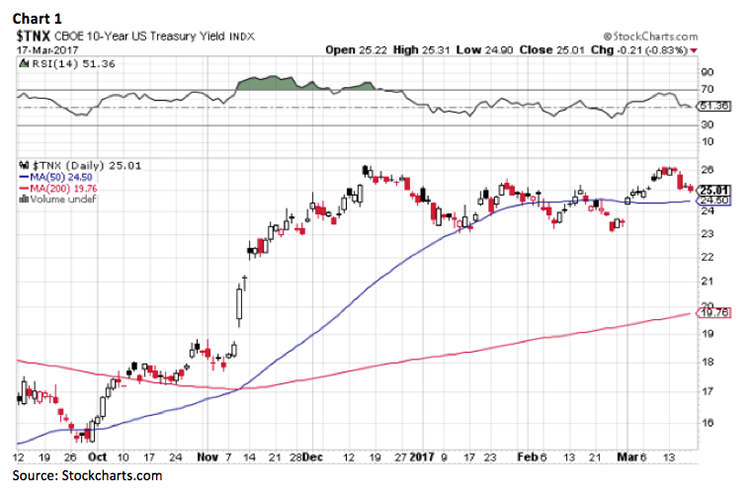

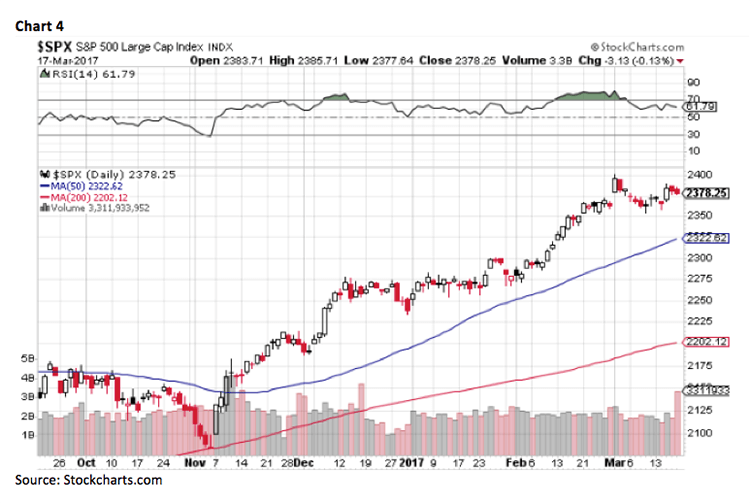

I spent last week climbing the mountains of Idaho and Utah, seeing accounts and doing presentations for our financial advisors and their clients. In my absence, the stock market did some climbing of its own as the S&P 500 (SPX/2378.25) came within five points of its all-time closing high (on an intraday basis), causing one old Wall Street wag to comment, “Can you spell double top?!” The challenge of the all-time highs came on last Wednesday’s “celebratory climb” following Ms. Yellen’s rate ratchet of 25 basis points, which occurred amid a string of softening economic statistics (sidebar: The Taylor Rule suggests the Fed is behind the curve by over 260 basis points). Despite last “Wednesday’s Win”, the SPX had no upside follow-through on Thursday, or even in Friday’s “quadruple witch twitch,” leaving it trapped in its 2350-2400 trading range that has existed since mid-February. Interestingly, given said rate rise, the 10-year T’note’s yield actually fell from Wednesday’s pre-FOMC announcement of over 2.6% into Friday’s close of ~2.5%. Almost on cue, the U.S. Dollar Index (DXY) declined from Tuesday’s intraday high of 101.79 to close the week at 100.31. Over that same timeframe, crude oil prices rose from $47.09 to $48.78, and gold rallied from $1196.80/ounce to $1229.80. On a very short-term basis, using NO fundamental analysis and just looking at the price charts, the 10-year T’note’s yield appears to have peaked (Chart 1 on page 3), crude oil looks to have bottomed (Chart 2 on page 3), gold has the appearance of a bottom (Chart 3 on page 4), and the S&P 500 looks toppy (Chart 4 on page 4).

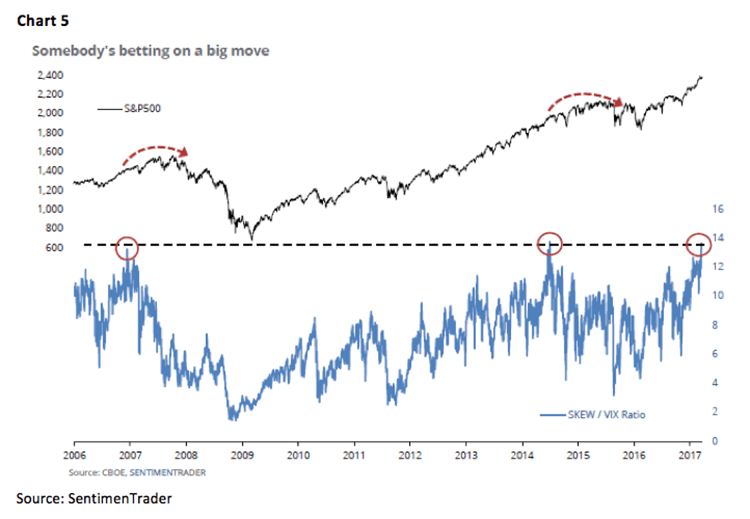

Speaking to our models, and the stock market’s “internal energy,” our long-term proprietary model flipped positive in October 2008 and has NEVER turned negative since then. In recent history, our intermediate model turned positive the week before the presidential election but flipped negative at the end of January and remains in cautionary mode. Likewise, the short-term model turned positive the week prior to the election and turned negative the last week of January; however, it flipped positive around the beginning of March. Obviously, our short and intermediate models are in conflict, which is why Andrew and I have often said that this is a confusing time in the equity markets. In the past, when our models have been conflicted, we have exercised patience, a strategy we are currently embracing. Certainly the large commercial hedgers are somewhat confused, because, with the stock market trading towards new all-time highs, they are “short” (betting on the downside) holding the second largest short position in the equity index futures in history. Meanwhile, there are some pretty weird breadth readings. According to the sagacious Jason Goepfert (SentimenTrader), “Advancing securities on the NYSE accounted for only 43% of all volume, while more than 60% of the issues actually rose. Since 1965, there was only one other day with a divergence like this. With lesser divergences (less than 45% Up Volume but more than 55% Up Issues), stocks struggled over the shorter term, with the S&P rising over the next seven days nine out of 24 times, averaging -0.7%.” The eagle-eyed Jason goes on to note, “One of the major reasons we were expecting volatility to rise in January (which likely meant stocks would also fall) was the fact that options traders were betting on an outsize moved, but it was being masked by what everyone was seeing in the VIX. We've looked at the ratio of the SKEW to VIX indexes for years as a way to get a little more information as to how traders are pricing in volatility expectations. In January, traders were pricing in a relatively high probability of a "black swan", or large, sudden move, in the next 30 days. That was a complete failure. Now it's even more extreme.” (Chart 5 on page 5)

Of course, this concurs with our “internal energy” model, which while not having a full charge of energy, has almost a full charge. This, too, implies a big move is capable of happening in the short run. If that energy is released on the downside, it is a long way down to even a shallow 0.382 retracement of the rally off of the pre-election lows with a target downside target of 2278 for the SPX. The ideal set-up for a pullback would be an early week rally attempt that either fails to exceed 2400 or marginally exceeds 2400, followed by steady stock market price erosion. Plainly, it is not required for the equity market to pull back, but our models suggest it should be difficult for the SPX to make meaningful upside progress from its current position. We guess it could grind away in a churning fashion, allowing the SPX to re-energize, but in our view, that is a low probability “bet.”

As for the sectors, excluding Real Estate, because it was not a sector back in 1990, weightings have changed dramatically since 1990, and even since 1999, as can be seen in Chart 6 on page 5. Of note is that four cyclical sectors currently have weaker breadth readings than the broad S&P 500: Energy, Materials, Industrials, and Consumer Discretionary (a tip of the hat to Bespoke Investment Group). That mix is likely due to the softening economic statistics and has caused some pundits to cry “a recession is coming.” We, however, believe the underlying economy is much stronger than the government’s figures suggest. To examine that “stronger economy” viewpoint, we are having a conference call with our pal Joe Brusuelas, who is the Chief Economist at RSM US LLP (formerly McGladrey LLP).

Sticking with the economy, and parsing President Trump’s proposed budget, shows the winners and losers. The winners: Defense with an increase of $52.3 billion (+10%), Veterans Affairs an increase of $4.4 billion (+5.9%), and Homeland Security with an increase of $2.8 billion (+6.8%). The losers: Health and Human Services (-17.8%), State (-28.7%); Education (-13.5%), Housing and Urban Development (-13.2%), Agriculture (-20.7%); Labor (-20.7%), Transportation (-12.7%), Energy (-5.6%), Commerce (-15.7%), Interior (-11.7%), Justice (-3.8%), Treasury (-4.1%), and the EPA (-31%). Moreover, President Trump’s proposed budget would eliminate: Community Development Block Grants, the Weatherization Assistance Program, the Low Income Home Energy Assistance Program, the National Endowment for the Arts, and the Corporation for Public Broadcasting. And don’t look now, but the House Budget Committee voted 19 to 17 to advance the Republican healthcare bill. Amid the cacophony of last week’s “political noise”, almost unnoticed was this Department of Commerce request: The Department of Commerce is seeking information on the impact of federal permitting requirements on the construction and expansion of domestic manufacturing facilities and on regulations that adversely impact domestic manufacturers.

Ladies and gents, this is HUGE, because fewer regulations will unleash the entrepreneurial spirts of America’s free enterprise system.

The call for this week: The SPX has experienced two “inside days”, meaning Thursday’s intraday high/low was “inside” Wednesday’s intraday high/low, and Friday’s action was “inside” Thursday’s range. According to Investopedia, “An ‘Inside Day’ is a candlestick formation [in the charts] that occurs when the entire daily price range for a given security falls within the price range of the previous day. Inside day often refers to all versions of the harami [chart] pattern and can be very useful for spotting changes in the direction of a trend.” We would also note there is a small upside gap in the SPX chart that occurred in last “Wednesday’s Win” between 2368.55 and 2368.94. Recall that gaps tend to get filled. Interestingly, the SPX’s 20-day moving average has proved to offer buying opportunities and it is now at 2371.64, so watch those two levels. This week’s trading action is key . . .