Third, and partly related to the previous item, we are scaling down the risk of a major China “accident” this year. Both our internal and external experts at the forum emphasized the will and the wherewithal of the Chinese leadership and central bank to maintain financial and (relative) exchange rate stability ahead of the 19th National Party Congress in the fourth quarter of this year. While capital outflow pressure and rising debt pose serious risks over the secular horizon, the cyclical outlook for China appears to be for relative stability. Note, however, that the lowered official growth target of around 6.5% for 2017 and the heightened focus of the authorities on financial stability imply a waning of the Chinese credit impulse for the global economy in the course of this year.

Fourth, recent polls as well as the outcome of the Dutch election last week suggest somewhat lower odds of success for nationalist, anti-European candidates and parties in the upcoming elections in France and Germany. In fact, as we discussed at the Forum, the momentum for Emmanuel Macron in France and Martin Schulz in Germany increases the probability of a “more rather than less Europe” outcome, which could benefit assets in the peripheral countries. Overall, however, we remain cautious on Europe given the near-term political event risk and also our secular concerns about the viability of the euro in its present form, as redenomination risk – albeit very remote – has resurfaced in the eurozone.

Fifth, we are scaling back our assessment of near-term inflationary pressures in the U.S. following the recent run-up in headline inflation (which we had anticipated). One reason is that labor force participation has increased in recent months, which is likely to damp wage inflation for now. Another reason is that oil prices have recently declined in response to fears of an expiration of last year’s OPEC deal on supply constraint just at a time when more U.S. shale supply is coming to the market. To be sure, we think longer-term risks to inflation are skewed to the upside, but at the same time the momentum behind the recent reflation trade is likely to ebb temporarily in the near term.

A strengthening and broadening global expansion

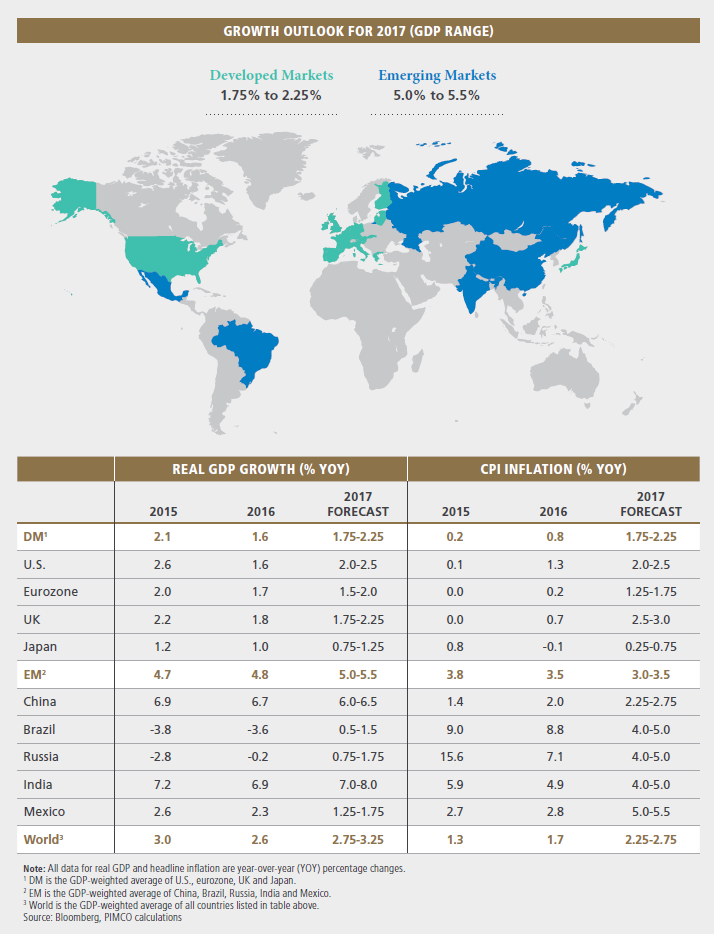

Putting it all together, we are now more confident in our baseline view that the nearly eight-year-old global economic expansion will be strengthening and broadening over our cyclical horizon. In fact, both world GDP growth and consumer price inflation for 2017 are now likely to come in a quarter percentage point higher than previously expected, reflecting: 1) generally supportive fiscal policies (or expectations thereof) in most developed market economies, 2) easier financial conditions since the start of the year, 3) more positive animal spirits as evidenced by consumer and business confidence data and 4) a rebound in global trade in recent months. While back in December we forecast 2017 world GDP growth averaging 2.5%–3.0%, we now expect growth to be in a 2.75%– 3.25% range this year, up from 2.6% in 2016. More specifically (and also see the forecast table), here are our baseline scenario estimates for growth and inflation in major economies around the world in 2017:

- We expect U.S. GDP to grow in an above-trend 2%–2.5% channel through 2017 as business investment recovers, particularly in the energy sector, and consumer spending is supported by a further decline in unemployment, higher consumer confidence and expectations of personal income tax cuts in 2018. Meanwhile, we forecast core inflation to hover sideways this year, but that the Fed will feel encouraged by above-trend growth to raise interest rates two more times during 2017 on top of the March rate hike. Also, we expect the Federal Open Market Committee to discuss and eventually agree on a plan to taper reinvestment of maturing bonds starting in 2018 and thus organically shrink the Fed’s balance sheet.

-

We now expect the eurozone economy to grow in a 1.5%–2% range in 2017, revised higher from our December forecast to reflect the stronger momentum into the year. While political uncertainty remains elevated ahead of crucial elections in France, Germany and potentially Italy, both fiscal policy and monetary policy are expansionary and the recovery in global trade growth supports exports and investment. We anticipate core inflation at just below 1%, making little headway toward the European Central Bank’s (ECB) “below but close to 2%” objective and that the ECB will keep buying bonds at the recently announced reduced pace of €60 billion per month through December 2017, before tapering and eventually ending its purchases from early next year.

-

In the UK, we forecast growth to stay in a 1.75%–2.25% range in 2017 (above market consensus) despite Brexit, reflecting robust momentum so far and supported by higher government spending and a positive contribution of net trade on the back of the 15% fall in the pound in 2016. We forecast CPI inflation to exceed the Bank of England’s 2% target, but that the Bank will keep policy rates unchanged throughout 2017.

-

Japan’s fiscal stimulus and a weaker yen will likely propel 2017 GDP growth into a 0.75%–1.25% zone while inflation remains subdued significantly below the 2% target. We expect the Bank of Japan to keep targeting the overnight rate at −0.1% and the 10-year bond yield at 0% and thus continue its standing invitation to the government to engage in additional fiscal expansion, which we expect to happen later this year.

-

China’s public sector credit bubble and its private sector capital outflows will likely remain under control this year,and we anticipate growth will slow into a 6%–6.5% band in 2017 as policymakers prioritize financial stability over economic stimulus ahead of the 19th National Party Congress in the fourth quarter of 2017. Any trade war with the U.S. will likely be engaged via words (and tweets) rather than action, and we expect the yuan to depreciate gradually by some 4%–5% against the U.S. dollar.

- In emerging markets, we expect Brazil and Russia will see moderate growth returning as their deep recessions end. With inflation dropping from elevated levels, both countries’ central banks can cut rates multiple times. Meanwhile, Mexico’s Banxico will likely tighten policy further (following the Fed’s lead) to support the peso and quell inflation. As a consequence, growth in Mexico will likely slow into a 1.25%–1.75% band in 2017.

Scaling back accommodation

But here is the catch, and it’s a big one: With improved growth and inflation prospects, exhausted central banks are likely to move closer to the exit from ultra-accommodative monetary policies. And it’s not certain whether highly leveraged private and public borrowers around the world will be able to keep dancing when the music stops.

As we learned in recent weeks, Janet Yellen and her colleagues at the Fed are now more confident that the time for “scaling it back” has come. The Fed will likely hike its policy rate twice more in the remainder of this year and looks set to allow assets to roll off its balance sheet gradually in 2018 by tapering reinvestment. Moreover, the likely replacement of almost the entire Board of Governors (including the chair and vice chair) over the next year and the potential for fiscal expansion at a time of full employment raises the uncertainty about the Fed’s future monetary policy reaction function (i.e., its targeted “if-this-then-that” response to new economic data and conditions – a function that itself can change over time along with the Fed’s policy approach).

In Europe, we expect the ECB to change its forward guidance on policy rates around midyear and to scale back its asset purchases further starting in early 2018, which raises the specter of sharp adjustments in euro area sovereign yield levels and peripheral sovereign spreads over Bunds.

One final note, and as mentioned earlier, with the Chinese authorities’ focus shifting from growth to stability, the strong Chinese credit impulse that supported global reflation in 2016 and into 2017 is likely to wane in the course of this year.

Needless to say, we will revisit and thoroughly discuss the longer-term risks associated with many of these issues in our annual Secular Forum in May.

Investment implications

Turning to our investment conclusions, financial markets have priced in the stronger baseline growth outlook, somewhat reduced left-tail (downside) risks and the faster path for Fed rate hikes, which we had anticipated. At current valuations we see it as appropriate to moderately scale back our credit exposures in our fixed income portfolios, while we expect to be broadly neutral on equities in our asset allocation portfolios. (For details on our asset allocation views and strategy, please visit our Asset Allocation Outlook page.)

The U.S. economy may indeed be graduating from multiple years of recovery following the global financial crisis, and there is some potential for the Fed to proceed on a more traditional tightening path (though that is not our baseline outlook). However, this is set against the combination of still muted growth in the rest of the developed world and the prospect of central banks moving closer toward the exit in Europe, the UK and Japan. One significant source of uncertainty is the prospect for U.S. dollar strengthening and the Trump administration’s words and actions in response to further dollar appreciation.

Duration

While there is the potential for a rise in the level of global interest rates, it remains the case that higher yields will be limited by still high levels of public sector debt and in some cases private sector debt, as well as demographic influences and slow growth in both productivity and credit availability. The greater normalization we have seen in U.S. rates compared with Europe, the UK and Japan and historically wide spreads mean that there is the potential for global yields to reprice closer to the U.S., and this also leaves the U.S. as the most attractive source of hard duration in the event of a shock.

Given valuations and the ongoing uncertainties in the global outlook, we continue to see the current environment as one in which we should avoid big calls on macro trades and instead look to grind out alpha, take advantage of mispricings and relative value opportunities, and respond to new information. Maintaining a sufficient level of liquidity (or “dry powder”) should allow us to respond as active investors to market volatility and high conviction opportunities when they present themselves.

We expect to keep portfolios fairly neutral on overall duration, with a preference for the U.S. over European, UK and Japanese duration and to maintain a bias toward curve steepening, based on the opportunity to generate income, expectations of a still measured pace for the Fed and other central bank tightening and the prospect that markets will price in greater risk premium at the longer end of global curves.

In our view, U.S. Treasury Inflation-Protected Securities (TIPS) continue to offer reasonable valuations and an attractively priced hedge against higher-than-expected inflation outcomes – particularly given the uncertainty over the extent of U.S. fiscal expansion at a time when the economy is at full employment.

Credit

We have moderately scaled back corporate credit exposures but generally expect to remain overweight in credit. We expect to continue to reduce generic investment grade and high yield positions in our portfolios, and focus instead on “bend but don’t break” credits: defensive, high quality, short-dated and default remote credit exposures. Financials continue to provide some good opportunities, but we will be careful on scaling of these positions. As always, rigorous credit research is paramount.

We expect to be overweight non-agency mortgage-backed securities (MBS), which again offer defensive qualities in the event of weaker-than-expected growth outcomes in addition to attractively priced risk premia for liquidity, complexity and uncertainty over the timing of cash flows. U.S. agency MBS also offer reasonable valuations and a source of income, although we will carefully monitor the prospects for the Fed reducing the reinvestment of coupons and the market impact.

We remain cautious on eurozone peripheral risk, based upon the challenging secular outlook for the eurozone, political risks and the ECB’s decision to scale back its quantitative easing (QE) program and the prospect for further tapering later in the year. The ECB’s tapering at a time when core inflation is a long way from target in the eurozone has called into question the extent to which the ECB will support both reflation in the eurozone and peripheral sovereigns in the event of political or economic shocks. We also expect to be underweight European corporate credit at current valuations.

Currencies

While we see some potential for modest U.S. dollar strengthening versus other major currencies, this is subject to significant uncertainty over the Trump administration’s response to a stronger dollar. Higher-yielding emerging market currencies offer attractive income-generating potential, but we will be careful in terms of the scaling of these positions.

Emerging markets

More generally on emerging markets, while we do not anticipate running large risk positions at current valuations, we will continue to look for good opportunities to add diversified positions to our portfolios.

Equities

We expect to be neutral on overall equity risk in our asset allocation portfolios. Equity markets have continued to rally, driven by the earnings recovery and the stronger global growth outlook. But we do not see significant upside potential for U.S. equities at current valuations in the absence of a breakthrough on corporate tax reform in the U.S. The stronger global expansion has the potential to boost cheaper cyclical markets, notably Europe, but this remains subject to eurozone political risk.

Commodities

Returns in and prospects for the commodity markets have improved materially since last year due to a combination of improved macroeconomic activity as well as material advances in the supply-side adjustment. We believe commodity allocations should be broadly at benchmark weight, as an expected increase in global GDP supports commodity demand. The correlation of commodities to other asset classes, as well as correlation within the commodity space, has returned to historical norms, pointing to the likely return of commodities as a portfolio diversifier. The positive correlation to inflation and inflation surprises also points to the benefits commodities may offer a portfolio, especially as infrastructure spending increases globally and austerity declines, as we anticipate.

All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Sovereign securities are generally backed by the issuing government. Obligations of U.S. government agencies and authorities are supported by varying degrees, but are generally not backed by the full faith of the U.S. government. Portfolios that invest in such securities are not guaranteed and will fluctuate in value. Inflation-linked bonds (ILBs) issued by a government are fixed income securities whose principal value is periodically adjusted according to the rate of inflation; ILBs decline in value when real interest rates rise. Treasury Inflation-Protected Securities (TIPS) are ILBs issued by the U.S. government. Mortgage- and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and while generally supported by a government, government-agency or private guarantor, there is no assurance that the guarantor will meet its obligations. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets . Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio. Equities may decline in value due to both real and perceived general market, economic and industry conditions. Commodities contain heightened risk, including market, political, regulatory and natural conditions, and may not be suitable for all investors. Diversification does not ensure against loss.

There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market. Investors should consult their investment professional prior to making an investment decision.

This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only. Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America L.P. in the United States and throughout the world.

© 2017, PIMCO.

© PIMCO

Read more commentaries by PIMCO