We live in a modern world of acronyms and buzzwords, and the financial industry is certainly no exception. In fact, it may be one of the worst culprits, what with FANG, ZIRP, TINA, BREXIT, QUITALY, BRIC, etc. all entering the lexicon over the last few years. Yet, creating some catchy collection of consonants remains one of the most surefire ways to attract attention in this business since it, admittedly, makes for a great headline and gives strategists like us something fun to write about (“fun” being a relative measure). Well, now the new eye-catching acronym to watch, according to Tom Lee of Fundstrat is C-R-A-P – Computers, Resources, American Banks, and Phone Carriers – which are all levered to the investment recovery, inflation, and deregulation expected over the next year. Before I comment further on those recommendations, though, I want to point out that I like to follow Tom Lee’s thoughts because, like us, he lets the data do most of his thinking, and, like us, he was one of the few pundits last year who actually saw potential for the U.S. stock market. He backed that up, too, with one of the highest S&P 500 targets among strategists for 2016 (2325), but now, according to Bloomberg, he has the lowest price target for 2017 among the fifteen strategists they track (2275), further proof that he doesn’t just parrot consensus numbers.

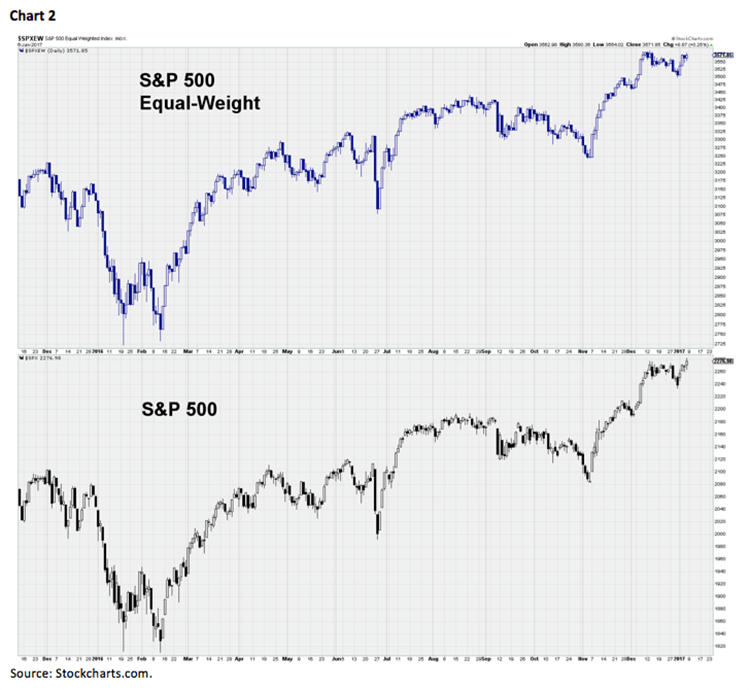

Reading between the lines of his comments, Lee does not see substantial upside for the stock market as a whole in 2017, at least not without a pullback first, but he does believe potential exists among individual areas of the market. This line of thinking is consistent with our view that passive indexing may be more frustrating in this type of investing environment because you will be dragged down by the underperforming sectors and the increased volatility may make it more difficult to hold onto positions long enough to achieve the eventual performance. We generally agree, too, that the C-R-A-P stocks should do well in the political and economic landscape that many expect is on the horizon. If inflation does pick up, driven by fiscal stimulus and more robust economic growth, Fundstrat argues that the contemporaneous increase in wages will not hit technology company margins as hard given their reliance on more high-skilled workers, and we, too, continue to advise an overweight of Tech to benefit from the Computers sub-sector. The big acronym of 2015 and 2016, the so-called FANG stocks, may already be coming back into favor, as well, with Facebook Inc. (FB/$123.41/Outperform), Amazon.com Inc. (AMZN/$795.99/Outperform), Netflix Inc. (NFLX/$131.07/Outperform), and Alphabet Inc. (GOOG/$806.15/Outperform) all breaking out to new reaction highs last week.

We also continue to like the Energy sector for the Resources play, as our fundamental analyst team in Houston still sees upside for the price of oil over the next couple of years and the companies should be run a bit more efficiently after all the cost-cutting that has been implemented. Their current favorites in the space are Oasis Petroleum Inc. (OAS/$15.58/Strong Buy), Unit Corporation (UNT/$30.25/Strong Buy), Kinder Morgan Inc. (KMI/$21.81/Strong Buy), and Tesoro Logistics L.P. (TLLP/$53.80/Strong Buy).

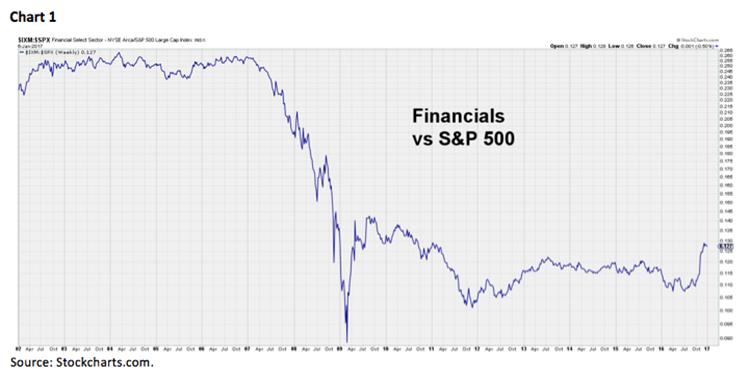

There are no shortage of American banks to choose from, either, but Bank of the Ozarks Inc. (OZRK/$52.36/Strong Buy) and Signature Bank (SBNY/$150.50/Strong Buy) are the two preferred by our analysts at the moment. I have actually received some questions lately asking if the run in banks is coming to an end, and not just in the short-term but for good. We think that’s ludicrous considering Financials have largely underperformed the broad market going all the way back to the early 2000s and it’s going to require more than a two-month run to begin to correct that divergence (Chart 1). In the near term, yes, many of the banks have likely come too far, too fast, but pullbacks should still be for buying, in our opinion as the yield curve is largely expected to steepen further.

Finally, the Phone Carrier part of C-R-A-P is a little trickier, as Donald Trump has already come out in opposition of at least one of the proposed mergers to further consolidate the industry and put more control in the hands of the major players. However, if we do experience a run of broad deregulation across the general business landscape, the big phone carriers could see some benefits in the form of pricing power (per Forbes), in addition to improving demand as the overall economy gets better. Verizon Communications Inc. (VZ/$53.26/Outperform), AT&T Inc. (T/$41.32/Outperform), and T-Mobile US Inc. (TMUS/$56.77/Outperform) are all rated “buys” by our fundamental analysts.