The second principle, agreed by a majority but not unanimously after a heated debate, is that while markets are romancing a “New Paradigm” of permanently higher U.S. growth, inflation and equilibrium interest rates, we believe that our secular New Normal / New Neutral theme remains intact, at least for now. Many of the secular drivers of low New Neutral interest rates – demographics, inequality, the global savings glut, elevated debt levels and technology – are unlikely to change anytime soon (see also the December Macro Perspectives, “New Paradigm?”).

However, there were several dissenting voices arguing forcefully in favor of a “New Paradigm,” and most PIMCO investment professionals acknowledge both the possibility of a regime shift if the right set of policies gets implemented, and even more so the potential for markets to try to anticipate such a secular shift.

The third principle guiding our cyclical outlook is that even though it is likely that The New Neutral will remain intact, we have to be alert to cyclical over- and undershoots versus that secular baseline. Recall that earlier this year, markets had clearly undershot our New Neutral estimate of the real policy rate of 0% by pricing in a below-neutral real fed funds rate for many years to come. This form of “irrational despondency” is now in the process of being corrected. At minimum, we see increased risk that the Federal Reserve will step up the pace of rate hikes compared with market expectations in anticipation of fiscal stimulus that comes late in the cycle when wage inflation is already accelerating.

The fourth principle is that not only the secular but now also the cyclical outlook in the new political environment is characterized by very high uncertainty, or “Radical Uncertainty,” to use the phrase coined by our Secular Forum speaker Mervyn King – which resounded with our own “stable but not secure” secular theme back in May. As Chicago economist Frank Knight pointed out in the 1920s, uncertainty is fundamentally different from risk: The latter can be quantified and priced based on statistical analysis and historical experience. As investors, we are used to attaching probabilities to “known unknowns” and positioning portfolios accordingly. Uncertainty, however, consists of the “unknown unknowns,” the stuff that hits you before you know it, the things to which it is difficult or impossible to attach probabilities. And to the extent that we can still attach probabilities to different macro outcomes, it is important to acknowledge that the tails of the distribution have become fatter. Fatter tails and a lower probability of the baseline scenario unfolding imply that, more than ever, we have to think about the outlook in terms of different scenarios and be open to scenario switching depending on the actual policies that get implemented.

This leads us to our fifth principle before we dive into the outlook for 2017. We agreed that the path for the economy and markets will likely be determined by how three difficult transitions will play out on the cyclical horizon:

- The transition from monetary to fiscal policy, which has gained speed with the European Central Bank (ECB) tapering the monthly run-rate of its asset purchases to €60 billion, the Bank of Japan (BOJ) abandoning its money supply target in favor of a yield target, and the next U.S. administration likely to embark on a more expansionary fiscal policy.

- The transition from globalization to de-globalization, which has been underway for some time but now looks set to accelerate as governments in the U.S. and elsewhere are likely to become more inward-looking.

-

China’s currency regime transition from what was a U.S. dollar peg until August 2015 to the current quasi basket peg to what may become a managed or even free float of the yuan.

Journey into the unknown

Once we had agreed on our guiding principles and key macro transitions, we sought to bring some order into the radical uncertainty by discussing our baseline view of the cyclical outlook, as well as the bull and bear scenarios, each powered by different assumptions on how the three difficult transitions would play out. Helped by our economic models, decades of experience and plenty of creative thinking, our regional portfolio committees constructed specific forecasts for growth, inflation and economic policy in these scenarios.

Baseline outlook: ‘Stayin’ Alive’

In our baseline scenario, the aging economic expansion, now already in its eighth year, becomes the third-longest in postwar history next March and stays alive and kicking during the remainder of 2017. Why? Because in this scenario, all three transitions are assumed to progress in relatively orderly and gradual fashion rather than becoming disruptive:

- Fiscal policy becomes supportive, even though fiscal stimulus in the U.S. on the order of $1.5 trillion over the next 10 years only passes Congress around midyear and is enacted from the start of fiscal year 2018 (i.e., October 2017).

- Central banks play ball and largely maintain their stimulus, thus limiting the rise in bond yields.

- A full-blown trade war is avoided, and the Chinese yuan depreciates only gradually by about 7% over the next 12 months.

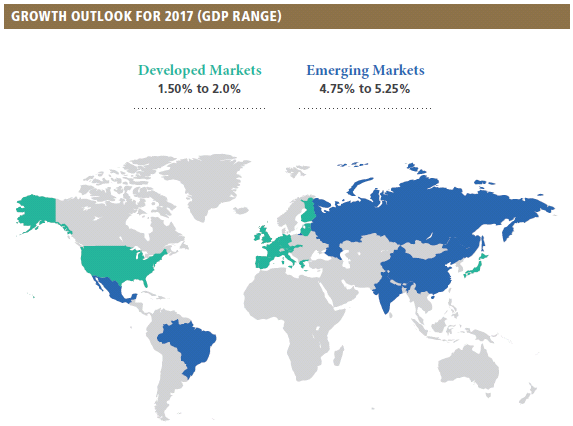

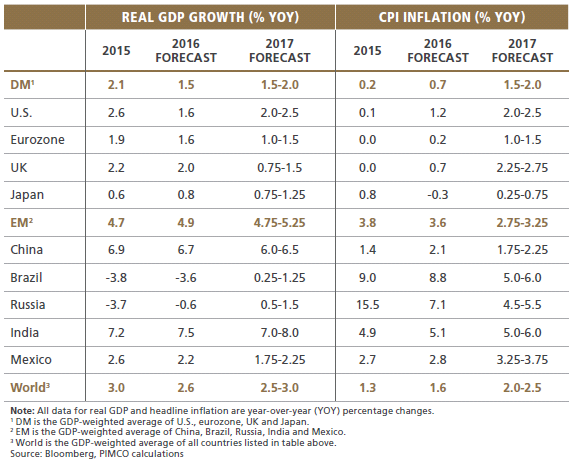

Based on these assumptions, world nominal output growth accelerates by one percentage point to 5% in 2017. World real GDP growth remains in the 2.5%–3% range that has held over the past five years, but headline inflation in developed markets (DM) picks up from the depressed 2015–2016 levels while high inflation in emerging market (EM) economies like Brazil and Russia ebbs significantly. Growth, inflation and policy divergences become more pronounced both within and between DM and EM, but the world economy keeps muddling through. More specifically (and also see the baseline forecast table):

-

U.S. GDP grows in an above-trend 2%–2.5% channel in 2017, twice the annualized growth rate realized from the fourth quarter of 2015 through the second quarter of 2016, but below the 3.2% realized in the third quarter of 2016. Business investment snaps back, helped by higher energy prices and more (eventual) clarity on corporate tax reform. Consumer spending is supported by a further decline in unemployment, rising wages and expectations of personal income tax cuts to be enacted at the end of 2017. Meanwhile headline CPI inflation rises to converge with core inflation above 2% and the Federal Reserve manages to raise interest rates two or three times during 2017 (with risks to the upside).

-

Eurozone growth hovers sideways in a 1%–1.5% range as political uncertainty remains elevated ahead of crucial elections in France, Germany, the Netherlands and, potentially, in Italy. However, the populists/nationalists don’t seize governmental power in any of the large countries. Headline inflation rises above 1% but core inflation makes little headway toward the ECB’s “below but close to 2%” objective. The ECB keeps buying bonds at the recently announced reduced pace of €60 billion through December 2017 but starts to discuss tapering its purchases further around the time of the German elections in September.

-

In the UK, growth slows into a 0.75%–1.5% range, reflecting fairly robust momentum so far but also the ongoing uncertainty over the modalities of Brexit; inflation exceeds the 2% target, inducing the Bank of England to keep policy rates unchanged and complete the existing QE program at the end of January – and then do no more.

-

Japan’s fiscal stimulus and recent yen weakening propel GDP growth into a 0.75%–1.25% zone in 2017 while inflation remains subdued significantly below the 2% target. The BOJ keeps targeting the overnight rate at −0.1% and the 10-year bond yield at 0% and thus continues its standing invitation to the government to engage in more fiscal policy. The invitation gets accepted sometime during 2017 and some further fiscal stimulus starts to get enacted.

-

China’s public sector credit bubble and its private sector capital outflows remain under control and growth slows into a 6%–6.5% band as policymakers prioritize financial stability over economic stimulus ahead of the 19th National Party Congress in the fourth quarter of 2017. Any trade war with the U.S. is engaged via words (and tweets) rather than action, and the yuan depreciates gradually by some 7% against the U.S. dollar.

- In EM, Brazil and Russia see moderate growth returning as their deep recessions end. With inflation dropping from elevated levels, both countries’ central banks can cut rates multiple times. Meanwhile, Mexico’s Banxico tightens policy following the Fed’s lead to support the peso and quell inflation. As a consequence, growth in the U.S.’s southern neighbor slows into a 1.75%–2.25% band.

Downside risk scenario: 'The Dark Side of the Moon'

In our left-tail scenario, all three difficult transitions go badly: U.S. fiscal reform gets delayed in Congress, European politics turns uglier as populism and nationalism gain further ground and Brexit-related concerns materialize. Severe trade tensions emerge between the U.S. and China, Mexico and others, and China retaliates by letting its currency drop by 15% or more against the U.S. dollar.

As a consequence, in our downside scenario EM growth decelerates rather than accelerates, with Russia and Brazil stuck in recession and China and Mexico slowing sharply. EM currencies and oil prices plunge. Weaker trade growth and the tightening of global financial conditions push smaller, more open economies like Japan and the UK into a mild recession, while the larger, less open U.S. and eurozone economies see GDP growth falling close to zero.

Finally, in this scenario the Fed’s interest rate normalization gets stuck as the dollar appreciates, the Bank of Japan pushes short rates (though not the 10-year government bond yield) further negative, and the ECB is forced into an embarrassing U-turn and steps up its asset purchases again. Meanwhile Banxico in Mexico has to tighten aggressively in response to a sharply weaker peso while room for rate cuts in Brazil and Russia is shrinking fast. In short, it gets really dark on the other side of the moon.

Upside risk scenario: 'Here Comes the Sun'

Our right-tail scenario assumes governments more quickly take over the baton of easing from central banks, led by a U.S. $2.5 trillion 10-year fiscal package. Presidents Trump and Xi Jinping practice the art of the (trade) deal that opens Chinese markets for U.S. exports and capital inflows, which in turn helps to stabilize or even appreciate the yuan. The populists/nationalists in Europe have minimal or no electoral victories, and policy reforms in EM proceed.

On this sunny side of the street, Lord Keynes’s “animal spirits” gain the upper hand over Knightian uncertainty, boosting consumption and investment. World real GDP growth exceeds 3%, U.S. inflation climbs to 3% and EM economies leave the misery of the last three years behind.

Finally, in this upside scenario DM economies finally reach escape velocity, so the Fed is comfortable hiking the policy rate four times in 2017, the ECB further tapers its bond purchases ahead of schedule (and Mario Draghi finally admits that tapering is tapering) and the BOJ exits negative short rates and cautiously nudges the 10-year Japanese government bond yield target above 0% as inflation accelerates. Conversely, strongly appreciating currencies and faster declines in inflation allow Brazil and Russia to cut interest rates by even more. A pretty picture, indeed.

Investment conclusions

Against the backdrop of a highly uncertain outlook and fatter than usual tails, we expect to be cautious in overall portfolio construction, sticking closely to our secular framework that emphasizes these key factors:

- A focus on capital preservation and a focus on tail risks, not just the most likely baseline

- De-emphasizing trades that rely on a high level of central bank support

- Guarding against the asymmetric risk of rising yields and especially against negative yields

- Focusing on bottom-up security selection

- Utilizing our teams across the world to find the best investment opportunities

- A very selective approach on the eurozone

- Careful overall portfolio positioning combined with active management to take advantage of periods of volatility and market dislocation

The experience of the past year has highlighted political risk and central bank policy exhaustion. At a time of fair to expensive valuations and less liquid financial markets, we have seen that it does not take much to prompt bouts of market volatility. By keeping portfolios lighter on risk and by being tactical and flexible as active managers, we can prepare for and look to benefit from market turning points. We think that patience will be rewarded.

Duration

We expect to continue to run fairly neutral duration overall in most portfolios, balancing our view that we will see a gradual rise in the level of yields over time with the uncertainty in the outlook, and we still expect to maintain some spread positions in our portfolios. We will react when we get greater clarity in the outlook and see better opportunities.

Amid the global macro uncertainty, we see clearly increased risk that the Fed will have to increase the pace of rate hikes compared with market expectations, in part reflecting anticipation of fiscal stimulus that is coming late in the cycle. On curve risk, we therefore expect to be underweight the front end of the U.S. yield curve.

Valuations and the prospect for higher inflation in the U.S. and other developed markets argue for maintaining an overweight to U.S. Treasury Inflation-Protected Securities (TIPS), which have repriced significantly but still do not price in the prospect of the Fed hitting its inflation target over time and continue to offer an attractive hedge against inflation overshoots. We see U.S. agency mortgage-backed securities as offering attractive valuations and expect to maintain an overweight in that sector as well.

In the U.S. and globally we favor underweighting the long end of the sovereign bond yield curve, based upon valuations and the balance of risks slanted toward some further curve steepening. This view reflects a combination of fundamental and policy-related considerations, including – in the case of the BOJ and the ECB – less support for the long end of the curve.

Credit

We expect to maintain modest spread exposure, with the aim of both increasing portfolio liquidity and looking to benefit from the relative value ideas from our global team of credit analysts. As well as using more liquid credit derivative indices, we expect to favor corporate credit exposures that are short-dated and self-liquidating. U.S. non-agency mortgage-backed securities remain our preferred spread sector, reflecting seniority in the capital structure and attractive return potential across a range of economic scenarios. This excess return potential reflects low ratings, low liquidity, the complexity of the securities and uncertain cash flows rather than their non-callable bullet structures. We have a large and experienced team and we continue to favor the relative value offered by this challenging sector.

Emerging markets

We expect to cautiously increase EM risk in our portfolios, balancing the substantial uncertainty in the outlook against attractive valuations and the fact that the significant Trump-related bad news for EM has been priced in (especially in currencies and local debt), providing an opportunity for long-term investors and the potential for diversification versus other risk factors. For now, we will focus primarily on high carry and commodity-related EM currencies to add carry to portfolios and utilize the most liquid vehicles for EM risk. Against that we plan to be underweight EM Asian currencies, given our expectation for ongoing China depreciation, low carry and the potential for monetary policy easing in that region to support weak domestic demand. Low inflation in the region would support the case for easing as well.

Europe

The Italian referendum outcome underlines the cyclical and secular political risk in the eurozone outlook. The ECB’s decision to reduce the monthly run-rate of QE purchases from March 2017 reinforces our secular caution on European peripheral sovereign risk in particular, and for de-emphasizing trades that rely on heavy central bank support in general. We expect to have very light positioning in eurozone peripherals and eurozone banks in most portfolios.

Equities

The outlook for equity returns has moved higher: Not only have markets emerged from the deep earnings slump of the last couple of years, but the prospect of accelerated future earnings growth seems higher given likely corporate tax reform and a generally more business-friendly environment. While we are optimistic about future earnings growth, we caution that companies will still face headwinds from the expected rise in real interest rates and potentially higher labor costs. We expect greater dispersion in equity returns based on regions, industries and even at the single name level than seen over the past few years, when central bank liquidity was the main factor driving most equity markets.

Commodities

Improvement in the macro outlook, as well as signs of some producer discipline from OPEC and general signs of advanced supply-side adjustment in various commodities, has boosted the outlook for commodities broadly. At current valuations, commodities continue to offer value as diversifiers and inflation hedges. However, given the rally in broad commodities in 2016, the burden is likely on OPEC to deliver on its agreements and on fiscal stimulus and other positive macro drivers to move from expectations to reality.

All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Sovereign securities are generally backed by the issuing government. Obligations of U.S. government agencies and authorities are supported by varying degrees, but are generally not backed by the full faith of the U.S. government. Portfolios that invest in such securities are not guaranteed and will fluctuate in value. Inflation-linked bonds (ILBs) issued by a government are fixed income securities whose principal value is periodically adjusted according to the rate of inflation; ILBs decline in value when real interest rates rise. Treasury Inflation-Protected Securities (TIPS) are ILBs issued by the U.S. government. Equities may decline in value due to both real and perceived general market, economic and industry conditions. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio. Mortgage- and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and while generally supported by a government, government-agency or private guarantor, there is no assurance that the guarantor will meet its obligations. Commodities contain heightened risk, including market, political, regulatory and natural conditions, and may not be suitable for all investors. Derivatives may involve certain costs and risks, such as liquidity, interest rate, market, credit, management and the risk that a position could not be closed when most advantageous. Investing in derivatives could lose more than the amount invested. Diversification does not ensure against loss.

There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market. Investors should consult their investment professional prior to making an investment decision.

This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only. Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America L.P. in the United States and throughout the world. THE NEW NEUTRAL is a trademark of Pacific Investment Management Company LLC in the United States and throughout the world.

©2016, PIMCO.

© PIMCO

Read more commentaries by PIMCO