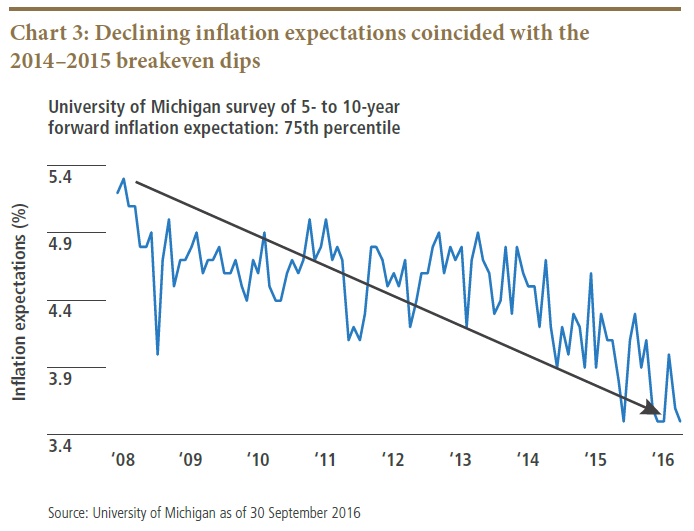

Survey-based measures of the distribution of longer-term inflation expectations realized similar shifts: The University of Michigan survey of five- to 10-year forward inflation expectations recorded a 1 percentage point (ppt) decline in inflation expectations for individuals who were previously expecting the highest inflationary outcomes (see chart 3). This led us to the simple yet elegant conclusion that the explanation for the U.S. inflation market’s behavior was a decline in the short- and long-term probability that realized inflation would overshoot the Fed’s 2% target.

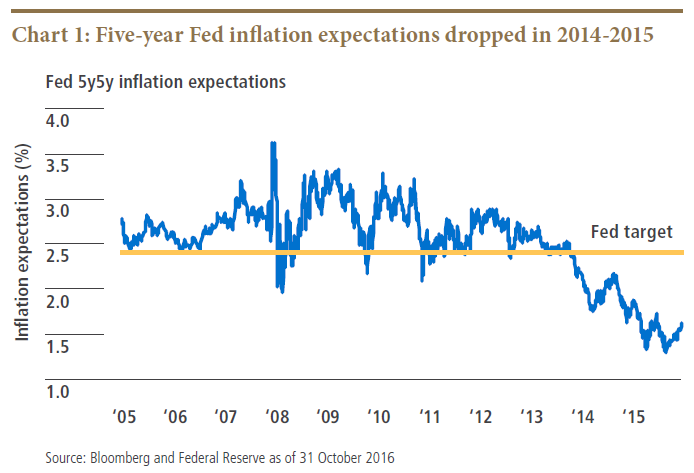

The 2014–2015 collapse in TIPS breakevens also coincided with a prolonged period of elevation of the output gap and choppy real growth in the wake of the 2008 financial crisis. We believe these factors, coupled with the more recent commodity price shock and glaring economic imbalances from Asian trading partners, raised questions about the Fed’s ability to reach its inflation target.

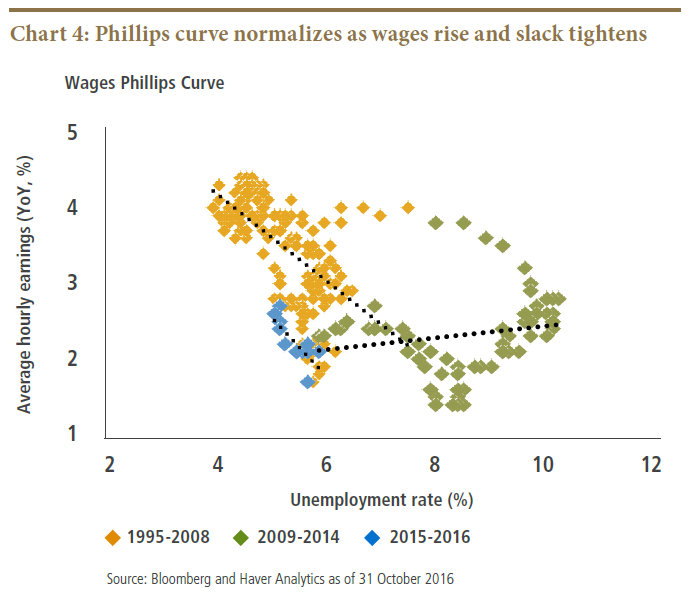

Things began to turn around in 2016, when easy monetary policy finally appeared on track to address labor market slack and deliver some promised realized inflation. Nominal wages were beginning to gradually accelerate, and as the previous commodity shocks faded, realized inflation (and the so-called Phillips curve) started to normalize (see chart 4). Not surprisingly, TIPS breakevens also began to rise off a very low base, and the Fed was preparing to re-engage in a slow but welcome normalization of interest rates.

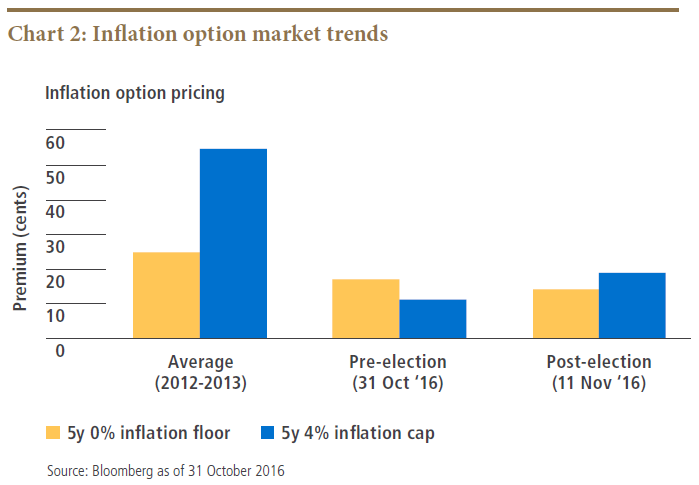

Then came Donald Trump (and a Republican sweep of Congress), with a policy agenda that has the ability to supercharge inflation markets.

Trump’s expected policies raise the probability of higher inflationary outcomes

Trump’s fiscal and immigration policies are likely to boost the near-term inflation trajectory, in our view.

Proposals for fiscal stimulus amounting to 2%–3% of GDP through a mix of tax cuts and infrastructure spending, if enacted, could boost aggregate demand by 0.3-0.5 ppts on average in the years after implementation. Such stimulus would come at a time when labor markets are very close to potential and could thus result in a somewhat faster acceleration of wage inflation than we would otherwise expect.

Trump’s immigration policies, as currently envisioned, could further accelerate wage pressures by shrinking the U.S. population by 2 million–3 million through deportations of illegal immigrants. These policies could also tighten labor markets by reducing inflows of legal potential workers.

Although the impact Trump’s trade policies may have on real growth is somewhat less clear, we view policies that restrict trade as broadly inflationary. If Trump follows through on expanding import tariffs, U.S. consumers will likely see an increase in the price levels of a range of goods. Meanwhile, if foreign governments place retaliatory tariffs on U.S. goods, the resulting supply chain disruptions could send prices soaring.

Plusses and minuses of higher inflation

From a longer-term perspective, one unambiguous benefit of a shift toward fiscal and away from monetary policy is that it could reduce the odds that the Fed will hit the zero lower interest rate bound in the future. We calculate that accelerating realized inflation and a declining output gap would allow the Fed to hike interest rates several more times over the next several years than it otherwise could. In the medium term, this should reduce the probability of deflationary outcomes, as the Fed would have more room to maneuver in the face of adverse economic shocks.

In addition, a growing amount of literature suggests that a “high pressure” economy could actually repair lingering supply-side damage from the crisis and raise trend growth rates. Higher trend growth rates could also allow the Fed to hike more aggressively, further reducing the probability of longer-term deflationary outcomes resulting from monetary policy exhaustion at the zero lower bound.

The bottom line for growth? We are not convinced that Trump’s specific mix of policies is better suited to boost trend growth than another policy mix that includes fiscal expansion. We believe Trump’s immigration and trade policies could be detrimental to productivity, while the impact of his fiscal policies would be broadly similar to (but perhaps no better than) any number of other reflationary policy mixes that would reduce pressure on the Fed.

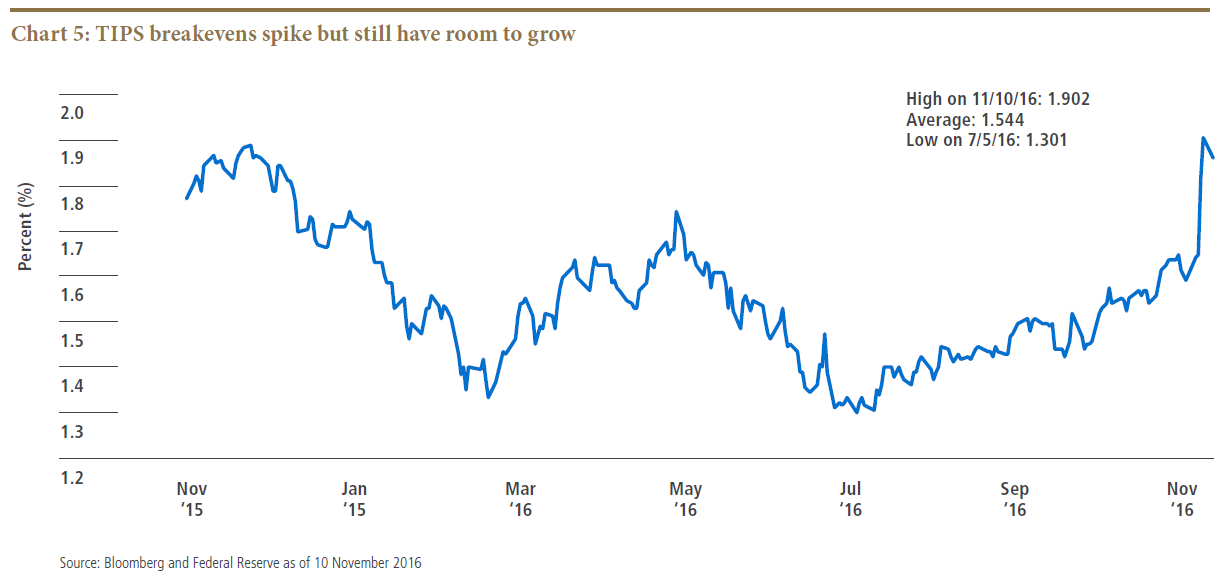

TIPS breakevens have room to widen

We think the market reaction since the election is justified, and we see room for a further rise in TIPS breakevens as actual policies roll out (see chart 5). The launch of fiscal stimulus when we are already well into the second half of a business cycle, coupled with an aggressive immigration policy and restrictive trade, should accelerate core inflation and boost the probability of higher inflationary outcomes.

We view this environment as potentially fertile ground for inflation-sensitive assets. Now more than ever, we believe real assets in general and TIPS in particular are an important allocation to a diversified portfolio.

All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Sovereign securities are generally backed by the issuing government. Obligations of U.S. government agencies and authorities are supported by varying degrees, but are generally not backed by the full faith of the U.S. government. Portfolios that invest in such securities are not guaranteed and will fluctuate in value. Inflation-linked bonds (ILBs) issued by a government are fixed income securities whose principal value is periodically adjusted according to the rate of inflation; ILBs decline in value when real interest rates rise. Treasury Inflation-Protected Securities (TIPS) are ILBs issued by the U.S. government. There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market. Investors should consult their investment professional prior to making an investment decision.

This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed.

© PIMCO

© PIMCO

Read more commentaries by PIMCO