It’s been really busy as of late to cover all of the topics I have wanted to address. One topic, in particular, is the bond market and the ongoing concerns of a “bond bubble” due to historically low interest rates in the U.S. and, by direct consequence, historically high bond prices.

Bob Bryan, via Business Insider, recently penned the following note:

“Bond yields are low. Historically low. Yields on government bonds in the US, Europe, Japan, and beyond are at seriously depressed levels. Even corporate bonds are reaching multi-decade lows as more investors pour into the asset class.

While the serious flows into these debt instruments continue seemingly unabated, Scott Colyer, CEO, and CIO at Advisors Asset Management thinks that the continued support for the asset makes no sense stating:

‘Bond prices are the highest they’ve ever been, yields are the lowest they’ve ever been and we go back to 1776, this is such an anomaly it’s not even funny.'”

While many financial analysts, asset managers and the media have been quick to adopt the idea of a “bond bubble,”there are a few things to consider with respect to this concept. As I have discussed previously, we are currently in the midst of the third stock market bubble since the turn of the century, but a bubble in bonds is a bit of a different animal.

As always, it is important to remember the problem with bubbles is that they can last far longer, and rise further, than most would generally think possible.

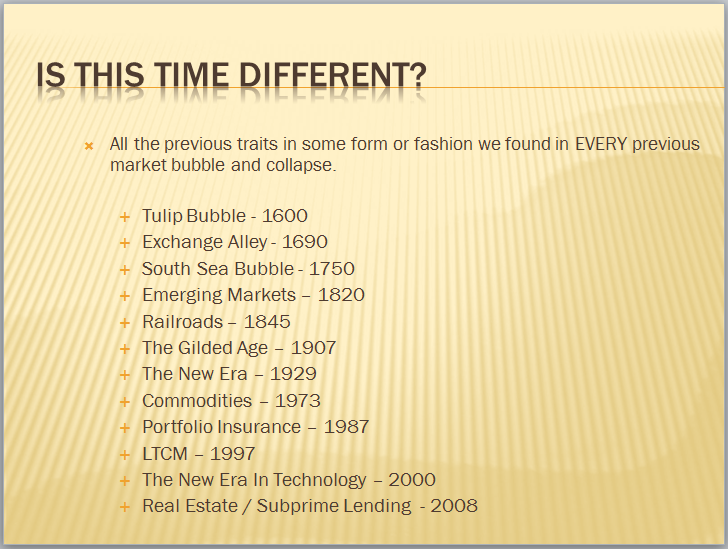

Throughout history, every bubble has been driven by a couple of common factors: excess liquidity, “a new era” mentality and speculative frenzy. Each time the bubble is formed it is believed that “this time is different” for one reason or another. The slide below was from a presentation that I did in March of 2008 when I was calling for the bursting of the equity market bubble at that time. No one believed me then because the markets were still surging higher as the belief was the economy had entered into a “Goldilocks” scenario.

The last bubble was driven by a speculative frenzy in real estate and debt which was spurred by loose lending standards, a collusion between banks and Wall Street (due to the repeal of Glass-Steagall), and the conversion of real estate into an ATM via mortgage equity withdrawals. As we all now know, despite repeated calls by Ben Bernanke everything was “contained,” it all ended very badly.

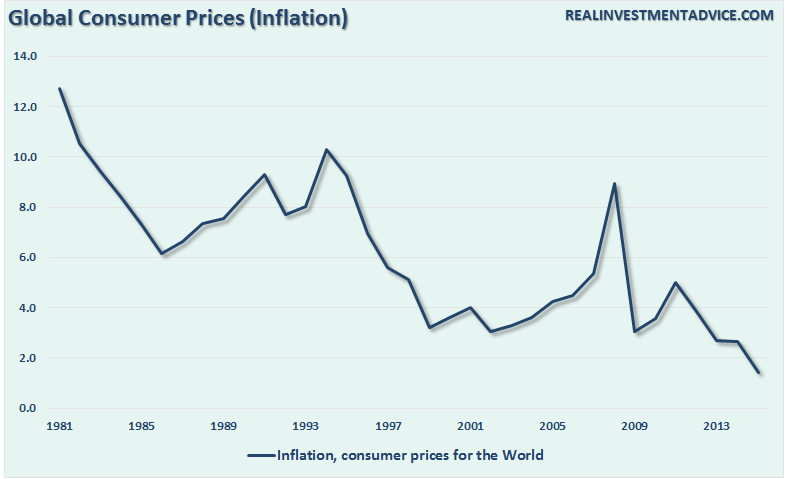

The current stock market bubble is different. It is being driven by a coordinated worldwide dump of liquidity into the financial system in order to suppress interest rates and inflate asset prices. The hope is this will eventually spark sufficient inflation to generate economic growth. However, after more than 8-years into the current experiment, such has yet to happen. In fact, globally, inflationary pressures continue to wane.

The “chase for yield,” due to the suppression of interest rates, has led investors into the fourth greatest bubble in the history of finance.

But that brings us to the bond market. With the longest-dated Treasuries now yielding less than one-third of the average 6.8% average yield over the past fifty-years, it’s not hard to see why forecasters say they’re bound to rise as the Federal Reserve tries to raise interest rates following the most aggressive stimulus measures in its 100-year history.

The premise is simple enough. With interest rates near their lowest levels on record, they have nowhere to go from here “but up,” right?

I am not in that camp, yet.

Here are the reasons why I remain convinced interest rates will remain in a very suppressed trading range not only into the end of this year, but likely for years to come. Furthermore, when the eventual reversion in the stock market occurs, bonds will continue to hedge long only portfolios against meaningful market declines while providing an income stream.

Economic Growth Drives Rates

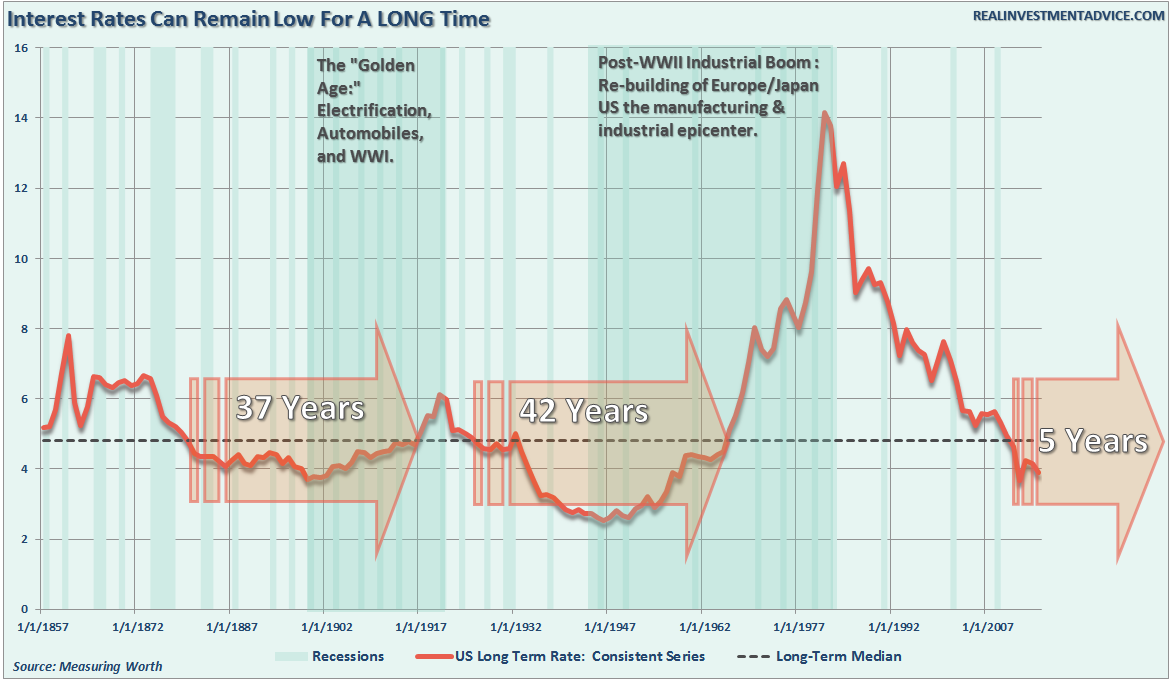

The chart below is a history of long-term interest rates going back to 1857. The dashed black line is the median interest rate during the entire period.

(Note: As shown, interest rates can remain low for a VERY long time.)

Interest rates are a function of strong, organic, economic growth that leads to a rising demand for capital over time.There have been two previous periods in history that have had the necessary ingredients to support rising interest rates. The first was during the turn of the previous century as the country became more accessible via railroads and automobiles, production ramped up for World War I and America began the shift from an agricultural to industrial economy.

The second period occurred post-World War II as America became the “last man standing” as France, England, Russia, Germany, Poland, Japan and others were left devastated. It was here that America found its strongest run of economic growth in its history as the “boys of war” returned home to start rebuilding the countries that they had just destroyed. But that was just the start of it.

Beginning in the late 50’s, America embarked upon its greatest quest in history as man took the first steps into space. The space race that lasted nearly twenty years led to leaps in innovation and technology that paved the wave for the future of America. Combined with the industrial and manufacturing backdrop, America experienced high levels of economic growth and increased savings rates which fostered the required backdrop for higher interest rates.

Currently, the U.S. is no longer the manufacturing powerhouse it once was and globalization has sent jobs to the cheapest sources of labor. Technological advances continue to reduce the need for human labor and suppress wages as productivity increases. Today, the number of workers between the ages of 16 and 54 is at the lowest level relative to that age group since the late 70’s. This is a structural and demographic problem that continues to drag on economic growth as nearly 1/4th of the American population is now dependent on some form of governmental assistance.

This structural employment problem remains the primary driver as to why “everybody” is still wrong in expecting rates to rise.

As you can see there is a very high correlation, not surprisingly, between the three major components (inflation, economic and wage growth) and the level of interest rates. Interest rates are not just a function of the investment market, but rather the level of “demand” for capital in the economy. When the economy is expanding organically, the demand for capital rises as businesses expand production to meet rising demand. Increased production leads to higher wages which in turn fosters more aggregate demand. As consumption increases, so does the ability for producers to charge higher prices (inflation) and for lenders to increase borrowing costs. (Currently, we do not have the type of inflation that leads to stronger economic growth, just inflation in the costs of living that sap consumer spending – Rent, Insurance, Health Care)

However, in the current economic environment, this is not the case. The need for capital remains low, outside of what is needed to absorb incremental demand increases caused by population growth, as demand remains weak. While employment has increased since the recessionary lows, much of that increase has been the absorption of increased population levels. Many of those jobs remain centered in lower wage paying and temporary jobs which do not foster higher levels of consumption.

Currently, there are few economic tailwinds prevalent that could sustain a move higher in interest rates. The reason is the higher interest reduces the flow of capital within the economy. For an economy that remains dependent on the generosity of Central Bankers, rising rates are not the outcome that “stock market bulls” want.

The Implications Of A Bond Bust

If there is indeed a bond bubble, a burst would mean bonds decline rapidly in price pushing interest rates markedly higher. This is the worst thing that could possibly happen.

1) The Federal Reserve has been buying bonds for the last 8 years in an attempt to push interest lowers to support the economy. The recovery in economic growth is still dependent on massive levels of domestic and global interventions. Sharply rising rates will immediately curtail that growth as rising borrowing costs slows consumption.

2) The Federal Reserve currently runs the world’s largest hedge fund with over $4 Trillion in assets. Long Term Capital Mgmt. which managed only $100 billion at the time nearly brought the economy to its knees when rising interest rates caused it to collapse. The Fed is 40x that size.

3) Rising interest rates will immediately kill the housing market taking that small contribution to the economy away. People buy payments, not houses, and rising rates mean higher payments.

4) An increase in interest rates means higher borrowing costs which lead to lower profit margins for corporations. This will negatively impact the stock market.

5) One of the main arguments of stock bulls over the last 8 years has been the stocks are cheap based on low interest rates. When rates rise the market becomes overvalued very quickly.

6) The massive derivatives market will be negatively impacted leading to another potential credit crisis as interest rate spread derivatives go bust.

7) As rates increase so does the variable rate interest payments on credit cards. With the consumer are being impacted by stagnant wages and increased taxes higher credit payments will lead to a rapid contraction in income and rising defaults.

8) Rising defaults on debt service will negatively impact banks which are still not adequately capitalized and still burdened by large levels of bad debts.

9) Commodities, which are very sensitive to the direction and strength of the global economy, will plunge in price as recession sets in.

10) The deficit/GDP ratio will begin to soar as borrowing costs rise sharply. The many forecasts for lower future deficits will crumble as new forecasts begin to propel higher.

I could go on but you get the idea.

The problem with most of the forecasts for the end of the bond bubble is the assumption that we are only talking about the isolated case of a shifting of asset classes between stocks and bonds. However, the issue of rising borrowing costs spreads through the entire financial ecosystem like a virus. The rise and fall of stock prices have very little to do with the average American and their participation in the domestic economy. Interest rates, however, are an entirely different matter.

I won’t argue there is much room left for interest rates to fall in the current environment, there is also not a tremendous amount of room for increases. Since interest rates affect “payments,” increases in rates quickly have negative impacts on consumption, housing, and investment. This idea suggests is that there is one other possibility that the majority of analysts and economists ignore which I call the “Japan Syndrome.”

Japan is has been fighting many of the same issues for the past two decades. The “Japan Syndrome” suggests thatwhile interest rates are near lows it is more likely a reflection of the real levels of economic growth, inflation, and wages.

If that is true, then rates are most likely “fairly valued” which implies that the U.S. could remain trapped within the current trading range for years as the economy continues to “muddle” along.

The irrationality of market participants, combined with globally accommodative central bankers, continue to push asset values higher and concentrate investors into the ongoing “chase for yield.” There isn’t much guessing on how this will end, history tells us that such things rarely end well.

© Real Investment Advice

© Real Investment Advice

Read more commentaries by Real Investment Advice