Can we stop this nonsense? Please.

One of the biggest reasons why investors consistently underperform over the long-term is primarily due to the extremely flawed advice promoted by Wall Street, because they have a product or service to sell you, and the media, because they don’t know better.

The latest bit of advice that you should immediately hit the “delete” key on is from Simon Moore via Forbes. The article, while it certainly fits the “buy and hold” narrative, is rife with flawed assumptions and analysis. To wit:

“You shouldn’t worry about market corrections. Not because they won’t come — they will. There is just no way of knowing when. Consider the data. It turns out that since corrections can’t be predicted, the best strategy is to remain invested for the long haul.“

Yes, as I will explain in just a moment, you should definitely worry about corrections as the destruction of capital is far more important than chasing returns.

However, the point of saying “corrections can’t be predicted” is inherently flawed. Yes, you definitely can not pinpoint the exact date and time of corrections, but THEY CAN be avoided.

There is a simple reason why every great investor has a simple rule that varies in form: “buy low, sell high.” Purchasing an investment is only ONE-HALF of the investment process, without the “sell” no money is ever actually made. Furthermore, it is the “sell” process that ultimately minimizes the effect of the correction and, most importantly, if you don’t “sell high,” you can’t “buy low.”

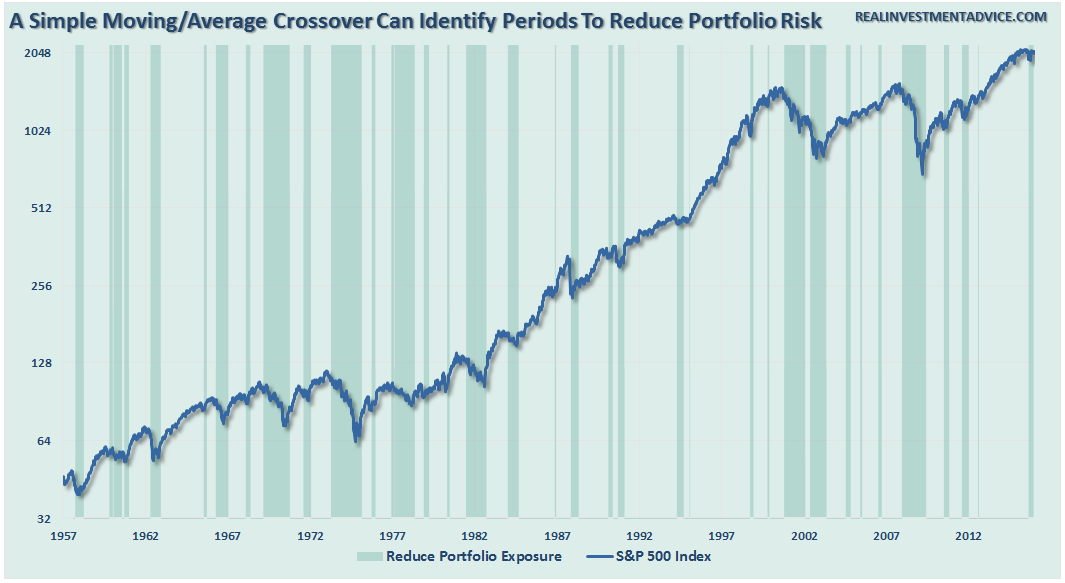

However, there are some basic premises around understanding the “when” corrections are most likely to present themselves. As shown in the chart below, a simple analysis of moving-average crossovers on a longer-term time frame can help investors avoid corrective processes in the market.

Did it work every time?

Of course, not. No investment discipline works 100% of the time. But that is not the point of investing to begin with. Missing a majority of the corrective processes, over the long-term, significantly improves returns. The chart below is $1000 invested on a “buy and hold” basis as Simon suggests versus using the simple moving-average crossover analysis in the chart above.

Not only did the risk managed portfolio achieve better long-term returns, it did so with significantly less volatility. That lower level of volatility allowed investors to remain adhered to their investment discipline versus eventually being flushed out at the bottom of major market corrections due to the inherent emotional biases we all possess.

Okay, let’s get on with the rest of the nonsense.

The Fallacy Of Long-Term Returns

Simon states:

“One of the best datasets on long-term returns comes from Elroy Dimson and colleagues at London Business School. They look at 116 years of data and find that a dollar invested in 1900 becomes $300 in 2015.

That’s a real return before any fees and commissions that equates to 5% per year.

Furthermore, that time period includes 2 markets that experienced a total loss during the period – Russia and China when they moved to Communism. The period also includes 2 World Wars, the assassination of 2 sitting Presidents (McKinley and Kennedy), 23 US recessions, and at least one hundred revolutions or major insurrections in many countries around the world.”

First, let me just say for the record everything in the statement above is absolutely correct.

The problem is you DIED long before ever achieving that 5% annualized long-term return.

Let’s look at this realistically.

The average American faces a real dilemma heading into retirement. Unfortunately, individuals only have a finite investing time horizon until they retire.

Therefore, as opposed to studies discussing “long term investing” without defining what the “long term” actually is – it is “TIME” that we should be focusing on.

Think about it for a moment. Most investors don’t start seriously saving for retirement until they are in their mid-40’s. This is because by the time they graduate college, land a job, get married, have kids and send them off to college, a real push toward saving for retirement is tough to do as incomes, while growing, haven’t reached their peak. This leaves most individuals with just 20 to 25 productive work years before retirement age to achieve investment goals.

This is where the problem is. There are periods in history, where returns over a 20-year period have been close to zero or even negative.

This has everything to with valuations and whether multiples are expanding or contracting. As shown in the chart above, real rates of return rise when valuations are expanding from low levels to high levels. But, real rates of return fall sharply when valuations have historically been greater than 23x trailing earnings and have begun to fall.

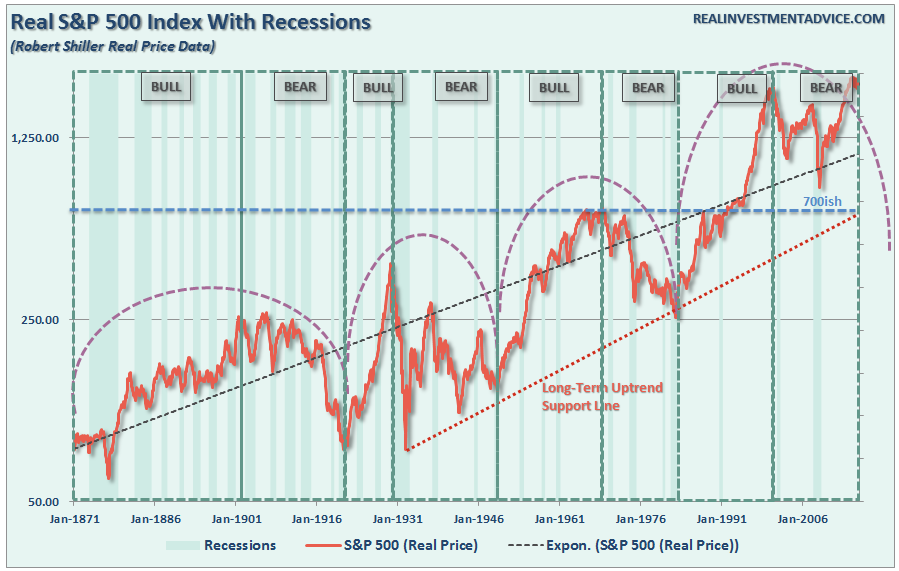

Long-term investment success depends more on the WHEN you start investing. This is clearly shown in the chart below of long-term secular full-market cycles.

Here is the critical point. The MAJORITY of the returns from investing came in just 4 of the 8 major market cycles since 1871. Every other period yielded a return that actually lost out to inflation during that time frame.

So, yes, major events do matter.

If you were unlucky enough to start investing in 1929, given life expectancies during that period, it is likely you died long before getting back to even.

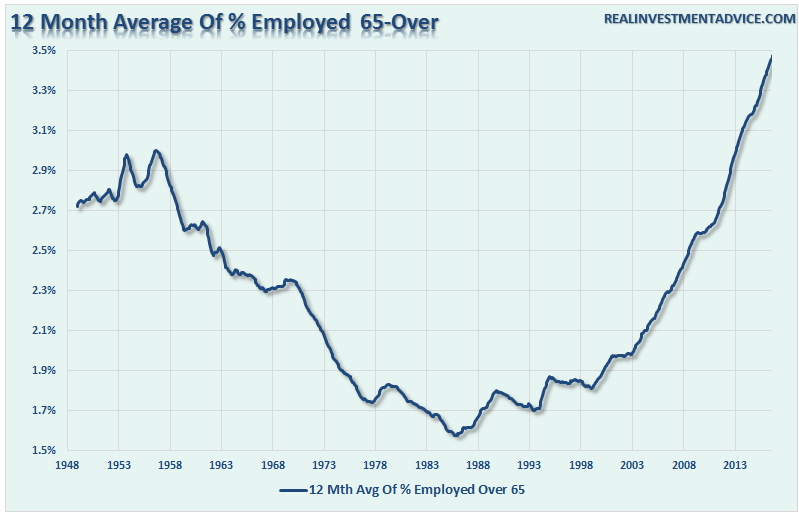

For those who were about to retire heading into the turn of the century, it is unlikely they are any closer to retiring today than they were 16-years ago. Maybe that is why the number of individuals over the age of 65 still in the labor force is at its highest level on record.

The bottom line is that YOU don’t have 100+ years to invest in order to achieve those “average” long-term returns you have been repeatedly promised. Well, that is unless you have contracted “vampirism” during your recent visit to Transylvania.

Second, your “long-term” investment horizon is simply the time you have between today and when you retire. And spending a bulk of that time horizon “getting back to even” is not an investment strategy that tends to work out well.

No, Stocks Don’t Do Well During Negative Events

“Also, consider that even in recent history bad events can be associated with positive returns. 2013 was a year that included a US government shutdown causing almost a million government workers to be furloughed, a $13 billion fine for a major bank (JP Morgan), major revelations on government data collection from Edward Snowden, and an attack at the Boston Marathon. Internationally, there was turmoil in Egypt and Syria, a major typhoon in the Philippines and a terrorist attack that killed 69 people in Kenya. The US economy grew at a relatively meager rate of 2.2% and unemployment held above 7% for most of the year. Yet in this rather bleak environment with many bad news stories the S&P 500 grew 32% for the year. It was the best return for the S&P 500 in 18 years.”

Really!

Uhm…you kind of forgot that 2013 was likely an anomaly driven by $85 billion dollars of liquidity injected each month by the Federal Reserve to offset the potential ramifications of the “fiscal cliff.”

It would have likely been a far different outcome ex-QE.

Historically speaking, stocks do NOT do well during negative events. Do events such at “Long-term Capital Management,” “Asian Contagion,” “Financial Crisis,” etc. ring any bells?

2008 Was a 30-Year Event?

“In fact, since 1928 there has been only one worse year for the S&P 500 than 2008. On average, a negative year for the S&P 500, which has occurred on average about every 3-4 years, means a decline of just under 14% on average.

It’s important to remember that 2008 was extreme, and more than double the average decline we have seen in a bad year for the market. We should consider it the sort of event we’d experience once every 30 years if history is any guide, rather than a standard bad year for the markets.“

Well, there are just a lot of things wrong with that statement.

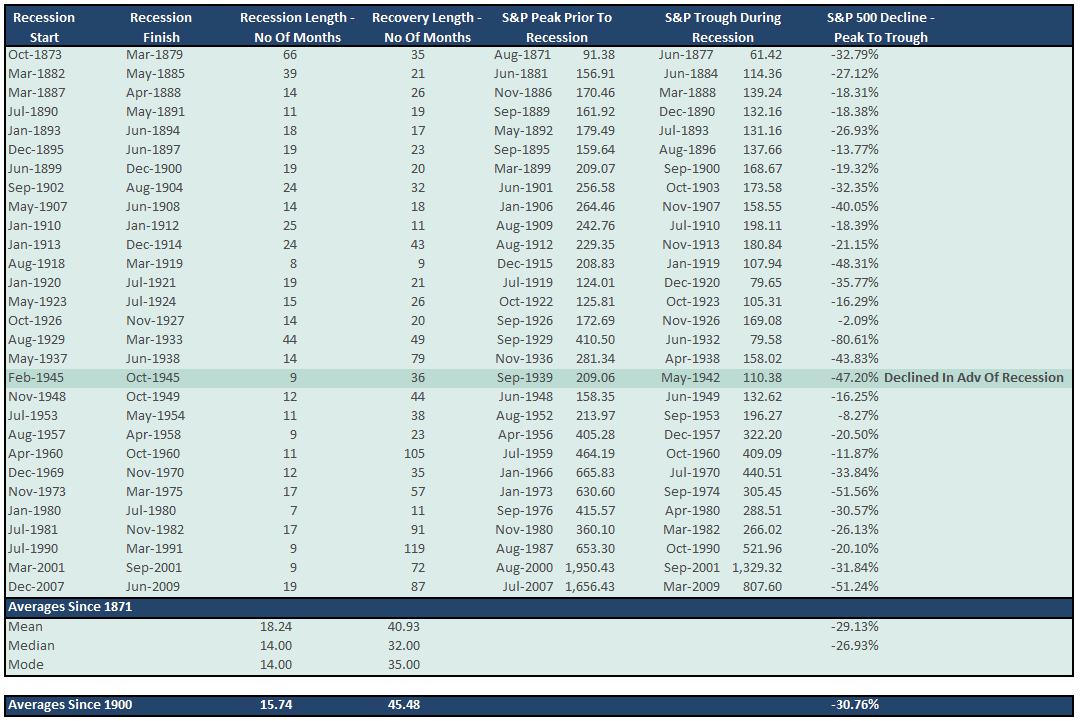

First, as shown in the table below, average corrections, particularly when associated with recessions, tend to be far worse than 14% on average. Try closer to 30%.

Second, if 2008 was a “once-in-30-year event,” then what are we calling the near-32% decline during the “dot.com” crash just seven years prior?

Yes, Please Worry About Corrections

In all fairness, Simon is only reiterating the “buy and hold” nonsense that continues to flood the mainstream media. This is the problem that occurs when people who don’t actually manage money for a living, write commentary about how you should manage your money.

With retirement plans having a finite time span for both accumulation and distribution of assets, the time lost in“getting back to even” following a major market correction is the primary consideration.

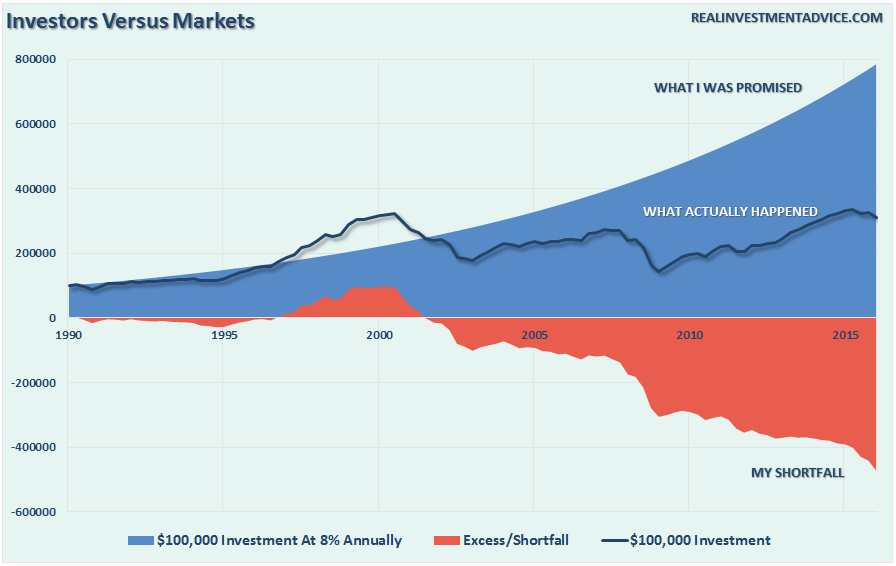

The chart below, which shows the difference between the inflation-adjusted returns on a $100,000 investment in the S&P 500 growing at 8% annually as opposed to the impact of gains and losses in market returns over time, illustrates the difference between expectations and reality.

The reason the chart begins in 1990 is, despite analysis showing 116-year investment returns, roughly 80% of all investors today began investing. Of that 80%, roughly 80% of those began after 1995. If you don’t believe me, go ask 10 random people when they started investing in the financial markets and you will likely be surprised by what you find.

Unfortunately, most investors remain woefully behind their promised financial plans. Given current valuations, and the ongoing impact of “emotional decision making,” the outcome is not likely going to improve over the next decade or possibly two.

For investors, understanding potential returns from any given valuation point is crucial when considering putting their “savings” at risk. Risk is an important concept as it is a function of “loss”. The more risk that is taken within a portfolio, the greater the destruction of capital will be when reversions occur.

Many individuals have been led believe that investing in the financial markets is their only option for retiring. Unfortunately, they have fallen into the same trap as most pension funds which is believing market performance will make up for a “savings” shortfall.

However, the real world damage that market declines inflict on investors, and pension funds, hoping to garner annualized 8% returns to make up for the lack of savings is all too real and virtually impossible to recover from. When investors lose money in the market it is possible to regain the lost principal given enough time, however, what can never be recovered is the lost “time” between today and retirement. “Time” is extremely finite and the most precious commodity that investors have.

In the end – yes, market corrections are indeed very bad for your portfolio in the long run. However, before sticking your head in the sand, and ignoring market risk based on an article touting “long-term investing always wins,” ask yourself who really benefits?

This time is “not different.” The only difference will be what triggers the next valuation reversion when it occurs. If the last two bear markets haven’t taught you this by now, I am not sure what will. Maybe the third time will be the “charm.”

Lance Roberts is a Chief Portfolio Strategist/Economist for Clarity Financial. He is also the host of “The Lance Roberts Show” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“.

© Real Investment Advice