Today’s Consumer Price Index (CPI) release was a bit of a mixed bag, but overall it doesn’t change our view that headline year-over-year inflation should accelerate toward 2.0%–2.5% over the coming year, as the drag from past energy price declines fades and core inflation holds around the current 2.2% pace.

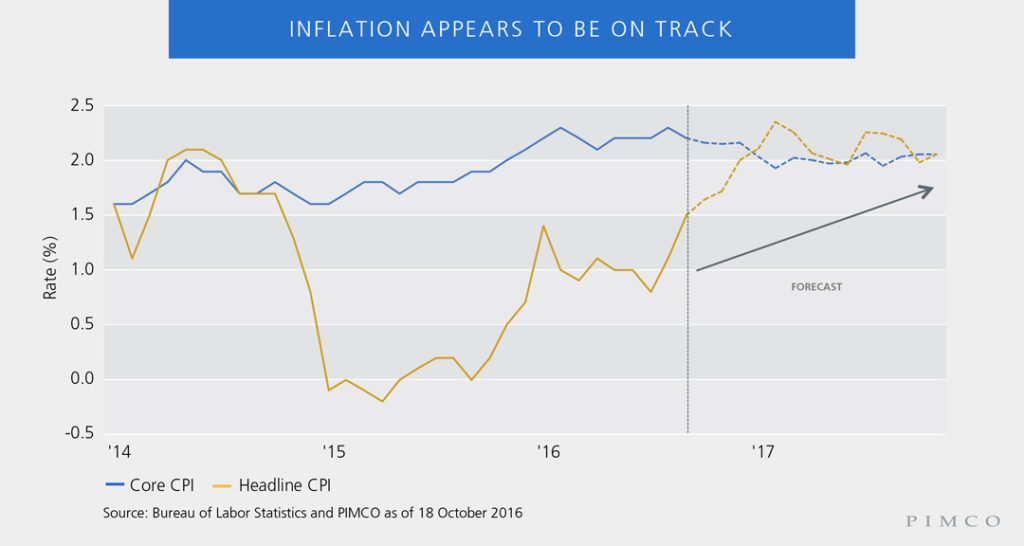

September headline inflation of 0.3% was broadly in line with our forecasts, while core inflation of 0.1% was slightly softer, but primarily owing to prices of goods and services that were notably firm in August. So when looking past the noise, inflation appears to be on track (see chart).

Headline CPI: a solid advance

Looking at today’s report in greater detail, the 0.3% increase in headline CPI was the strongest advance in over a year, driven by a 6.0% increase in retail gasoline prices. Over the past six months, retail gasoline prices have stabilized and recovered somewhat after the oil price collapse in 2014 and 2015. The recent stabilization has been enough to pull up the year-over-year rate of headline inflation from 0.0% last September to 1.5% now. As we emphasized in a recent post, over time, this acceleration should support longer-term inflation expectations.

Core inflation: a bit soft

The 0.1% increase in core prices, while slightly softer than we were expecting, was concentrated in areas that will likely reverse. For example, apparel prices were notably weak, declining 0.7% in September. However, even slight differences in discounting relative to typical seasonal patterns can affect apparel prices, which tend to peak in September on a non-seasonally-adjusted basis as retailers introduce their fall clothing lines. The September softness in seasonally adjusted prices was particularly notable in outerwear, likely indicating some early discounting as a result of warmer-than-average temperatures.

Meanwhile, medical services prices were unchanged in September after a very firm 1% increase in August and average monthly increases of 0.5% over the past six months. Hospital and physician service prices measured by the CPI have been rising as insurance companies increase out-of-pocket premiums. The September outcome likely reflected some bounce-back from a particularly large price increase in August, and we expect prices to revert to their recent trends next month.

Finally, used car prices were also relatively weak, declining 0.3%. However, we find that used car auction prices tend to lead new car inflation, and auction prices continue to point to some acceleration ahead.

Pockets of strength

It’s important to note that core inflation wasn’t universally soft. Shelter inflation, which makes up the largest portion of the CPI basket, was surprisingly firm: September rents and owners’ equivalent rents advanced 0.3% and 0.4%, respectively, and prices of lodging also rose a notable 1.0% (on the back of a 2.0% advance last month). Rent prices tend to track housing prices with a lag, so the recent moderation in the pace of housing price increases should start to filter through to rents in the coming months. However, a continued decline in labor market slack and a gradual acceleration in wages should be broadly supportive of rents and shelter inflation over the next few years.

Tiffany Wilding is a PIMCO economist focusing on the U.S.

© PIMCO