The analogy between the stock market and poker has always been irresistible. Interestingly, the stock market increasingly resembles a low-stakes recreational game among friends and less the sort of ‘there goes the ranch’ game favored by cutthroat professionals. Recreational poker is frustrating but ultimately profitable to the serious player. Recreational players come to play. They play every hand. They make long-odds bets. They are hard to read because fear of losing money is not a factor in the game. They can’t be bluffed. The serious player is a different animal, playing the odds, maximizing winnings on pat hands, and figuring that in the long run his superior abilities will prevail.

The stock market is dominated by institutional equity fund managers who are paid to own stocks. The decision to own stocks already has been made by an asset allocation committee or by the individuals who bought the mutual fund. Like the recreational poker player, equity fund managers are there to play. It is not their money and they are far less worried about losing money than underperforming the market. Put it this way: Individuals in the ‘business of investing’ want to out-perform their peers. It’s a different kind of game. If the market is down 20% and the equity professional is down 15%, he or she is ecstatic. If the market is up 20% and the equity professional is up 15%, he or she is despondent. The growing dichotomy of purpose between the owners of the money and the people managing the money is little understood.

When individuals played a bigger role in the stock market, those great allies of the serious independent – fear and greed – came more frequently into play. Every couple of years there would be compelling bargains or shorting opportunities. The market favored by institutions – the S&P 500 – is expensive by historical standards. But the institutions aren’t selling – as individuals might have done – because they have to be invested, and where else can they put all that money?

. . . Frederick “Shad” Rowe, Greenbrier Partners

The aforementioned prose was scribed by my friend Frederick “Shad” Rowe, of Greenbrier Partners fame, decades ago and it is just as relevant today as it was back then. I dredged it up this morning because I am in Dallas this week to attend Shad’s “Great Investors’ Best Ideas Symposium” (GIBI) tomorrow. Tonight I will be attending the speakers’ dinner convened at Shad’s home where Michael Price, David Einhorn, T. Boone Pickens, and Mario Gabelli (to name but a few) and I will dine to discuss the “state of the state.”

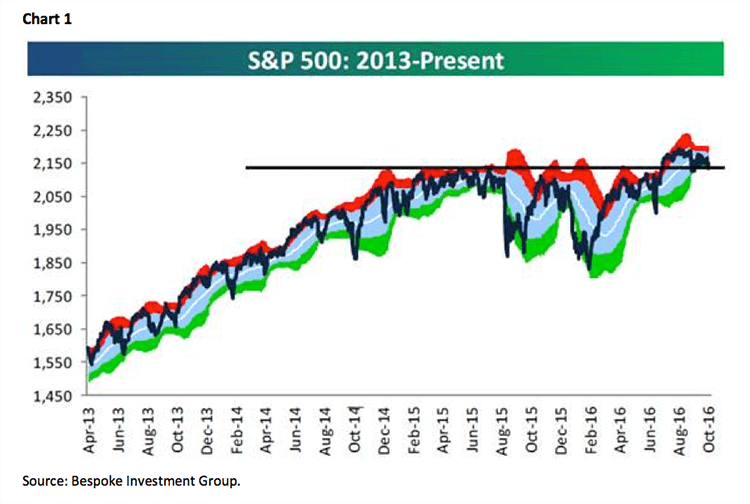

Obviously, one of the main topics of discussion will be about the recent stock and bond market consternations since mid-September. Of course my models suggested such consternations would be the case since late August, however I did not think the environment would be this frustrating. So, we got the first “consternation” on September 13 when the D-J Industrials (INDU/18138.38) fell 258 points, while the S&P 500 (SPX/2132.98) surrendered 32 points and, in the process, tested its 2100 – 2120 support level. That downside test proved successful, leading to a rally that carried the SPX back to its 2180 – 2200 overhead resistance zone. While many pundits believed that rally meant the correction was over, Andrew and I were less sanguine since our models failed to confirm that THE low was “in.” Sure enough, the SPX came back down and broke below the September lows in mid-October and again select pundits said the correction was over. Hereto, our models were not so sure. So far, all we have seen is the July upside breakout from the nearly two-year range-bound stock market and a subsequent downside retest of the support level of 2100 – 2120 (see chart 1). Last week we experienced more frustration with the Industrials up about 88 points on Monday, off 200 points Tuesday, better by 15 points on Wednesday, down 45 points comes Thursday, and up some 40 points on Friday, although we would note the Industrials were up over 100 points early in Friday’s session. That caused one savvy seer to lament, “Up mornings and down afternoons is not particularly good market action!”

For the week, the Industrials fell 0.56%, the SPX declined 0.96%, and the NASDAQ Comp surrendered 1.48%. On a sector basis, the worst sector was Healthcare (-3.27%) with Utilities (+1.33%) and Consumer Staples (+0.66%) the only sectors posting gains. The weekly wilt left the SPX and NASDAQ Comp at critical support levels. As often stated, 2100 – 2120 is the key support zone for the SPX with downside “pivot points” at 2108 and 2092. If these levels are violated on a closing basis, we will have to rethink our near-term strategy. But until then, as repeatedly stated last week, “What has happened this week is NOT a definitive break to the downside.”

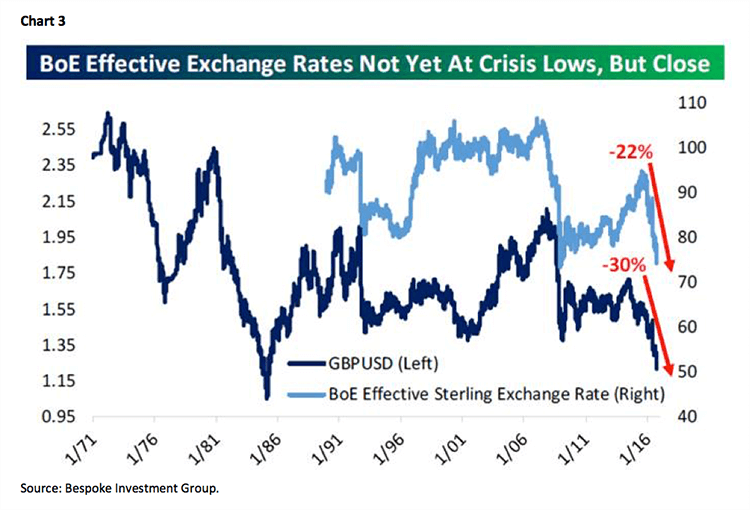

Two of the major events that occurred last week happened in the bond market, where the 10-year T’note yield broke out to the upside (read: higher rates – chart 2) and the collapse of the British pound (chart 3). The weaker British pound is actually quite bullish for British multinational companies and I am tilting portfolios accordingly. I am using select actively managed mutual funds to accomplish this. As often stated, I think individual investors are doing the exact wrong thing by selling actively managed funds, while buying passive funds. When stocks are undervalued, and the indices are going straight up, investors need to own “cheap beta” (passive funds). However, when stocks are neutrally valued, or by some measurements over-valued, you want actively managed funds. The reason is that an active manager can say, “I don’t want to play in that particular game because valuations do not make sense.” Case in point, for months Andrew and I have made the argument that the defensive stocks, or low volatility names (chicken longs) are extraordinarily expensive. And guess what, that space has “rolled over” in the charts and has broken down. We suggest pruning those names from portfolios.