One of the rarest traits on Wall Street is patience, yet patience is one of the biggest secrets of successful investing. As noted in R.W. McNell’s book Beating The Stock Market:

If there is ever a time when speculators should exercise patience, it is in waiting for a proper opportunity to buy stocks. The desire to make money is at the foundation of all commercial and financial transactions, but the mere desire to make money should never be the mainspring of speculative action. Knowledge or belief based on intelligent analysis that a speculative opportunity presents itself is the only safe basis for making purchases of stocks. It is in forgetting that principal that so many speculators err. They do not ask when they are preparing to buy stocks, ‘Is the stock cheap, and is it selling below its real value?’ but ‘Is that stock going up?’ The only sound reason for buying stock is that it can be had cheap. Granted that, and also that it represents ownership in one of our great essential American industries, a speculative profit is practically assured, if one have patience, regardless of whether the price goes lower before it goes higher. But when anyone buys a stock merely because he thinks or someone tells him it is going up, regardless of its real value, he is following a speculative plan which is absolutely certain to lead on to ruin. He may make a profit once, twice, or half a dozen times by that method, but sometime he is absolutely certain to be badly hurt.

It has been said if you don’t like the weather . . . wait a minute. Recently, the same can be said about the stock market. I mean really, here are the daily point gains and losses for the D-J Industrials over the past two weeks: +200, -196, +111, +133, -167, -131, +99, +164, +10, -363. Evidently Mr. Market has had a case of schizophrenia since mid-September. And that, ladies and gentlemen, is why we have elected to have patience until our models render a clear-cut direction for the equity markets in the short run. For the longer term, we have not wavered in the belief the secular bull market remains alive and well. However, we have also tried to “call” some of the shorter-term vagaries of the equity markets in an attempt to help clients adjust their portfolios. For example, coming into September I recommended trimming some stocks from portfolios to raise a little cash for future investment opportunities. At the time we said history shows that all we should get in terms of a pullback is 3% to 6%; and what we got was 3.4%, at least so far. So the question du jour would currently be, “Is the pullback over?”

As repeatedly stated in these missives, while we hope the pullback is over, our models are currently unclear. Over the past 46 years we have learned that when that happens it is best to have patience and do nothing until the models “speak.” Therefore, until the S&P 500 (SPX/2168.27) closes above its 2187 “pivot point,” our models remain in a defensive posture. That does not mean I have not been adjusting portfolios. On Friday I sold two energy stocks that have rallied sharply since the February lows, and over the past few weeks I have actually bought some select stocks and mutual funds to rebalance my portfolio. My purchases, however, have NOT been in the defensive sectors that have been so popular year-to-date. As my friend Jason Goepfert (SentimenTrader) writes:

Defensive sectors have been the best performers so far this year. Through September, the most defensive sectors have been the most consistently good performers, while the most economically-sensitive sectors have lagged. If we create a score that ranks the performance of the sectors through the 3rd quarter, we see that 2016 ranks among the most extreme. When that's happened in the past, 4th quarter returns were okay, but much below returns when the most aggressive sectors had led through September.

In past reports we have commented on our friends at J.P. Morgan asset management’s work showing the “defensive sector” is massively over valued and should be way underweighted. In our recent conference call with Rich Bernstein he agrees and favors the Consumer Cyclical sector over the Consumer Staples sector. BTW, we favor a number of the Eaton Vance ETFs he actively manages. To that “active management” point, we think investors are doing the exact wrong thing in switching from active managers to passive managers at this stage of the market cycle. When stocks are cheap, and the indices are going straight up, you want to own cheap beta. Yet when stocks are neutral valued (like now) you need to have actively managed portfolios for reasons often stated in these reports.

In addition to Rich’s managed ETFs, and the video I did with SEI’s Steve Treftz, who manages the SEI Multi-Asset Income Fund (SIOAX/$10.56), if I had to buy another stock right here it would be Williams Company (WMB/$30.73/Outperform). Our fundamental analysts like WMB and I would note it is the last “Barbie Doll” on the shelf. Given Canada’s Enbridge recently announced acquisition of Spectra Energy, WMB is indeed the last “Barbie Doll” on the shelf. Williams Company has a terrific pipeline system, a great chemical business, and an MLP that any acquiring company could “drop down assets” into . . . well, you get the idea.

The call for today, according to thechartstore.com:

Mark ‘em up Friday for month/quarter’s end made for a slightly up week (S&P 500 +0.17%). Friday was another one of those rumor filled days centered this time on Deutsche Bank. The week was also filled with Yellen testimony and a never ending parade of Fed presidents spewing the party line. The Fed added talk of buying stocks to the discussion. Oh, for the good old days when price discovery was at play in the markets, not central banks.

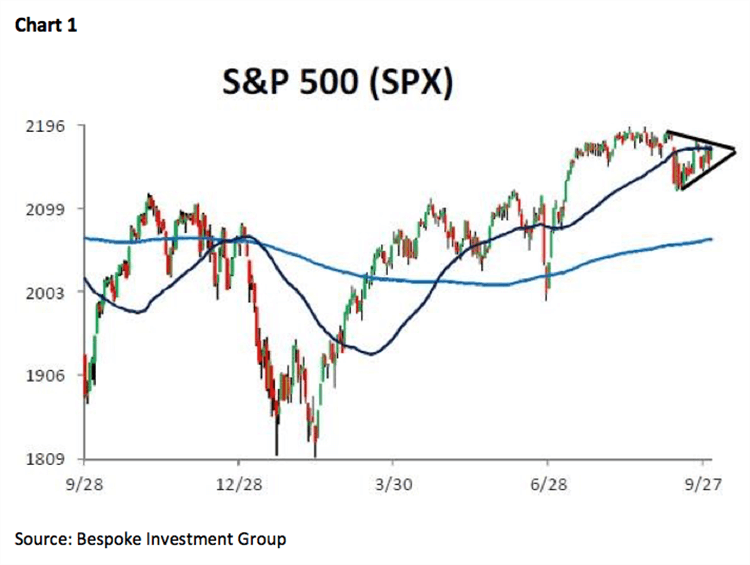

The call for this week: So on Friday the Agence France Presse carried a story that the DOJ was close to settling with Deutsche Bank not for the original $14 billion penalty, but for $5.4 billion. Combine that with rumors Germany will not let the bank go under (we have said for months that Angela Merkel would never let a bank with Germany in its name go bankrupt), and the D-J Industrials rallied 165 points helped by the bank and energy stocks. Meanwhile, earnings season is starting and we continue to think earnings will be solid, believing the “profits recession” ended in 2Q of this year. And don’t look now, but Wall Street strategists have been lowering their year-end price targets for the S&P 500 to where it currently changes hands. To that, FundStrat’s Thomas Lee writes, “That’s great news! When market prognosticators predict little or no gain, the S&P 500 has traded higher 12 months later 95% of the time, with an average gain of 11%.” Currently, the SPX has pinched itself into a tight triangle consolidation chart pattern (see chart on page 3). A breakout of that pattern to the upside would suggest an upside test of our 2187 “pivot point.” If the SPX can close above 2187 it will turn our short-term timing models positive, and the forecasted mid/late-September pullback should be over, as the secular bull market continues.

P.S. I will be on the West Coast all this week seeing accounts and speaking at events. I am writing this on Sunday night, and recording the verbal comments without the benefit of the preopening futures prices, because I am not getting up at 3:00 a.m. on Monday morning to do this live . . .