A man has rigged up a turkey trap with a trail of corn leading into a big box with a hinged door. The man holds a long piece of twine connected to the door, which he can use to pull the door shut once enough turkeys have wandered into the box. However, once he shuts the door, he can’t open it again without going back to the box, which would scare away any turkeys lurking on the outside.

One day he had a dozen turkeys in his box. Then one walked out, leaving 11. “I should have pulled the string when there were 12 inside,” he thought, “but maybe if I wait, he will walk back in.” While he was waiting for his 12th turkey to return, two more turkeys walked out. “I should have been satisfied with the 11,” he thought. “If just one of them walks back, I will pull the string.” While he was waiting, three more turkeys walked out. Eventually, he was left empty-handed. His problem was that he couldn’t give up the idea that some of the original turkeys would return . . .

“I should have” sold at 2190! Many a trader and investor went home last Friday night uttering those words. The S&P 500’s (SPX/2139.16) 2190 level has really been frustrating since early August. To be sure, the SPX has tried numerous times to vault above that level for the past seven weeks with eyes for 2200. “Surely,” participants thought, “Following the strong upside breakout above the 2120 – 2130 zone, which had contained the SPX since March of last year, the next logical price target should be the round number of 2200!” “Such round numbers are typically money in the bank,” was the cry, but a funny thing happened en route to 2200.

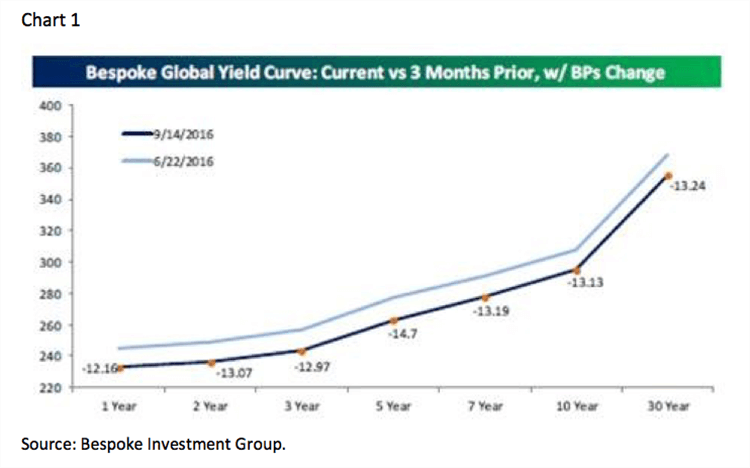

In past missives we have chronicled various indictors and events that concurred with our timing model’s message that mid-/late-September was the first point of downside vulnerability for the equity markets. Most recently it has been interest rate worries that slugged stocks, as participants pondered a rate increase at this week’s FOMC meeting. For our part, Andrew and I have been quite adamant for five months that rates are not going to be raised until after the presidential election. Nevertheless, the world is expecting interest rates to eventually increase as yield curves everywhere appear to be steepening (chart 1). Typically, when that happens it suggests either a stronger economy, or a pickup in inflation, and maybe both. In last Friday’s verbal comments we noted that Thursday’s action, where bond prices declined (higher rates) and the U.S. dollar rose, it implied Mr. Bond wants interest rates to rise. Moreover, a steepening yield curve is a decided positive for the financial complex, which is why most of the financial-centric indices have broken out to the upside in the charts.

Speaking to higher interest rates, while a quarter point increase in the Fed Funds rate would likely cause a stutter-step in the equity markets, the impact on the overall economy should be de minimis. In fact, it just might cause a flurry of refi’s on the assumption the low water mark for the mortgage market is “in.” Interestingly, it was the surge in mortgage refinancing years ago that caused the consumer to buy more “stuff” and helped drive a pickup in the economy. Importantly consider this, an argument can be made that the Federal Reserve is not really “tightening” until they raise interest rates above the embedded rate of inflation. Until that happens it can be said the cost of money is still relatively “cheap” and abundant. In the current case that would mean Fed Funds would have to rise above ~2% before it should be considered a “tightening.”

Turning to the equity markets, I found this gleaning from my friend, and savvy investor Joe Monaco, Ph.D., pretty interesting:

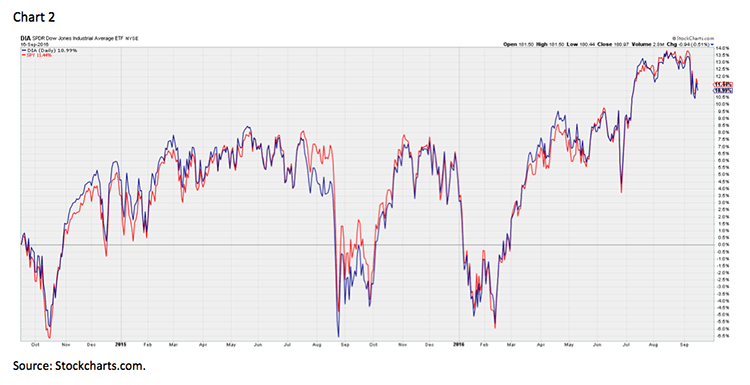

I keep hearing, from almost every source, that the entire market’s returns are being driven by four stocks, Netflix, Amazon, Apple and Google. However, did you know that over the past 24-months both the Dow Jones Industrial Average and the S&P 500 have had almost the exact same return with almost the exact same volatility? And yet, Netflix, Amazon, and Google are nowhere to be seen among the Dow’s 30 stocks. As proof of my analysis, please look at the comparative chart of the Dow Jones Industrial Average along with the S&P 500 (I actually used the DIA and SPY ETFs for charting purposes), courtesy of Stockcharts.com (chart 2). I think this reasoning is just portfolio managers justifying why they have so very much underperformed.

We have touched on this underperformance point before by noting, “If the active portfolio manager (PM) doesn’t outperform the bogey index, but outperforms the ETF that is supposed to track said index, is that a win for active management?” Indeed, except for the S&P 500, whose ETF tracking error is small, the tracking error for most of the other ETFs is large. The problem is that you can’t buy the index! Further, there are implementation costs for any strategy and “cash drag” for the active managers since they all hold a position of the portfolio in cash, which is earning nothing. Consequently, if you view active performance through this ETF comparison lens, you find more than 50% of active PMs outperform their respective ETF. What we found is that when stocks are undervalued, and the index is going straight up, you want to own “cheap beta.” However, when the markets are neutrally valued, or overvalued, you want active management. The reason is the active manager can say, “I don’t want to play in that particular game.” But what are individual investors currently doing? They are doing the exact wrong thing. They are selling active managers’ funds and buying passive funds.

Speaking to active management, I have always found Thomas Lee’s market insights to be net worth-changing; first, as J.P. Morgan’s Chief Investment Strategist, and now at his own firm (Fundstrat.com), where he currently makes a compelling case for buying the recent pullback. He writes, “Has our conviction changed about markets staging gains into yearend (YE)? No. Since 1940, to gauge what stocks do between 9/15 and YE is simply look at YTD performance. When stocks are up 5% or better, they rally into YE 87% of the time (90% when between 5% and 20%). In other words, we believe this 3% pullback NEEDS TO BE BOUGHT aggressively.”

The byline to his report reads, “Why we are buyers of this pullback and see 6%-8% gains into yearend: History says 90% likelihood of YE rally – 12 stock ideas.” Of course readers of these reports know that we too have stated the current pullback is unlikely to be anything more than a 3% - 6% drawdown setting the stage for a year-end rally. As a sidebar, MarketWatch’s Barbara Kollmeyer writes, “The crowd wants this stock market correction too badly for it to happen,” which inferentially bolsters our shallow correct “call,” but I digress. Parsing Thomas’ 12 stock ideas, which are also favorably rated by our fundamental analysts and screen positively on our proprietary algorithm, for your consideration include: Cisco (CSCO/$30.84/Outperform), Praxair (PX/$117.68/Strong Buy), Texas Instruments (TXN/$69.36/Outperform), Microsoft (MSFT/$57.25/Strong Buy), Xilinx (XLNX/$53.36/Strong Buy), Kinder Morgan (KMI/$21.47/Outperform), Union Pacific (UNP/$92.38/Strong Buy), and Apple (AAPL/$114.92/Outperform). To paraphrase Thomas, sell the outperformers over the past few years and buy the underperformers.

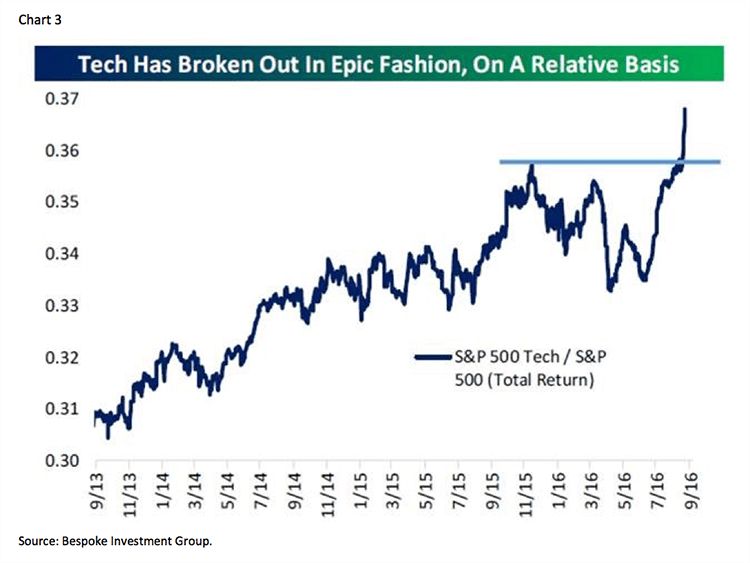

The call for this week: To discuss the current state of various markets, my friend Rich Bernstein (ex-investment strategist at Merrill Lynch and now eponymous captain of Richard Bernstein Advisors) and I will conduct a joint conference call tomorrow (Tuesday 9-20-16) at 4:00 p.m. The dial in number is (866) 393-4306 with the password Eaton Vance. Tactically speaking, this week the Fed and the BOJ (Japan) will provide their latest views on monetary policy. We think both will be a non-event. And then there was this from BlackRock’s Rob Kapito, “Stocks globally could continue to rise as interest rates remain low as investors who have stockpiled some $70 trillion in cash seek higher returns from the market. People are tired of earning zero," Kapito said at the Barclays Global Financial Services Conference in New York, “There's more cash in the system than ever before.” And don’t look now but tech has broken out to the upside in the charts (chart 3). Be optimistic my friends . . .