“Dry land is not just our destination, it is our destiny!”

. . . Deacon, from the movie “Water World”

As we dig out from Hurricane Hermine, where residents of Cedar Key experienced a nine-foot sea surge and consequently were looking for dry land, investors too have been seeking “dry land” for the past few months. To be sure, it has been a difficult environment with the S&P 500 (SPX/2179.98) trapped in a trading range between the August 2 low of ~2148 and the August 15 high of ~2191. In fact, looking at the closing prices of the S&P 500 (e-minis) shows an August range of just 1.54%. That’s the tightest range since August 1995 and the seventh smallest since 1928 (a tip of the hat to Ryan Detrick). That trend continued last week, yet from our water-soaked location we suggested the intraday low of last week (~2157) may represent the tradeable lows for this cycle, despite our model’s warning of vulnerability in mid/late-September. So what are longer-term investors to do? To answer that question, we harken back to our friends at the astute Riverfront Investment Group organization, a number of whom I worked with at Wheat First Securities in a life gone by. A few years ago I wrote:

For underinvested participants, we continue to like Riverfront Investment Group’s strategy for committing new capital to stocks. First, identify the quantity of cash to be put to work – example: 20%. Second, break the trade into digestible chunks – example: break it into four parts, 5% each. Third, implement the first trade today – example: invest 5% into equities today. Fourth, set a date for implementing the second trade – example: two months from today invest the second 5%. Fifth, implement third and fourth segment if a market pullback occurs – example: invest the remaining 10% of the cash on market pullbacks. And sixth, after the date of the second trade occurs, return to step one with the remaining cash – example: two months from today, if the market never provides the opportunity to buy on a pullback, break the remaining 10% up into 3-4 parts and follow a strategy similar to the one utilized for investing the first 10%.

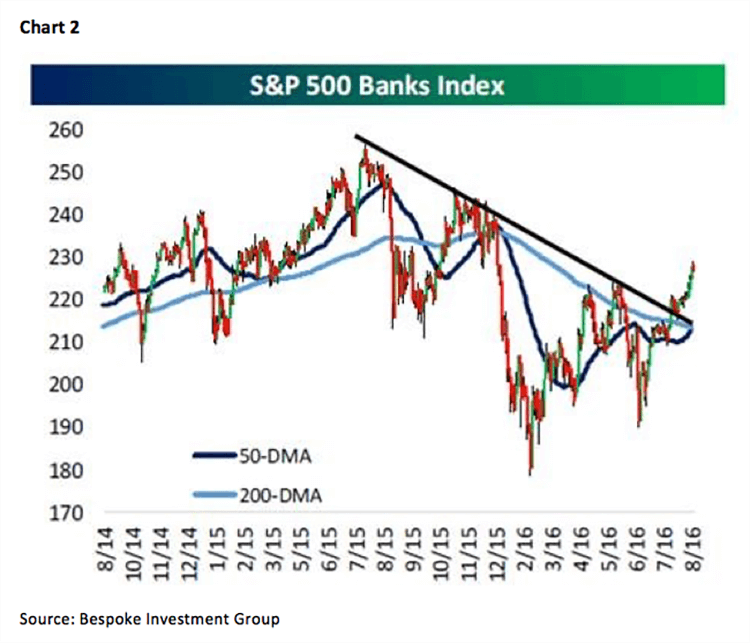

So now you have a strategy, the next step is what sectors should you consider? Studying chart 1 (see page 3) reveals the PEG ratio (price to estimated growth) is expensive for the alleged “safe sectors.” As can be seen, the cheapest sector is Consumer Discretionary (0.96), followed by Information Technology (1.52), Healthcare (1.57), and Industrials (1.80), all of which have a lower PEG ratio than the S&P 500 Index (1.83). Recently, Andrew Adams and I have been featuring the Financials (which at 1.92 have a marginally higher PEG ratio than the index) because there has been a massive upside breakout in ALL of the financial indices (chart 2). It is worth mentioning that last week the MSCI adjusted its Global Industry Classification Standards (GICS) by taking real estate investment trusts (REITs) out of the Financial sector and creating a new 11th sector for the S&P macro sectors (the mortgage REITs stay in the Financial sector). This has implications for select exchange traded funds (ETFs) like the Financial Select Sector SPDR Fund (XLF/$24.57) because without the REITs the dividend yield on the XLF should decline from roughly 2.0% to less than 1.4%. To see how big a contributor to performance the REITs have been, just examine chart 3 on page 4.

You now have an investment strategy on how to commit capital to the equity markets and which sectors offer the lowest valuations, so let’s turn to overall valuations. I read a report last Friday that this year’s “bottom up” earnings are estimated to be around $117 for the S&P 500. I don’t know where that estimate came from, but it certainly was not from Standard & Poor’s. S&P’s “bottom up” estimate for this year (as of 8/29/16) was $110.76 versus last year’s $100.45. If S&P’s estimate for 2016 is close to the mark, it implies stocks are pretty expensive with a P/E ratio of 19.7x earnings. However, S&P’s 2017 estimate is $132.91, leaving the SPX trading at 16.4x next year’s estimate with an earnings yield of 6.1% (earnings ÷ price, or $132.91 ÷ 2180 = 6.1%). When compared to other investment alternatives those valuation metrics are not all that expensive. Moreover, as often expressed in these reports, we believe the secular bull market is transitioning from an interest rate to an earnings-driven bull market. This should become more evident over the next 12 months.

Turning to the asset classes, and using trailing 12-month earnings, shows most asset classes are expensive. For example, these are the P/E multiples for the five major asset classes: U.S. Large Cap 22.43x; U.S. Mid Cap 24.69x; U.S. Small Cap 22.61x; Non-U.S. Developed 19.35x; and Emerging Markets 15.81x. Hereto, however, the P/E multiples are more parsimonious using 2017 estimates.

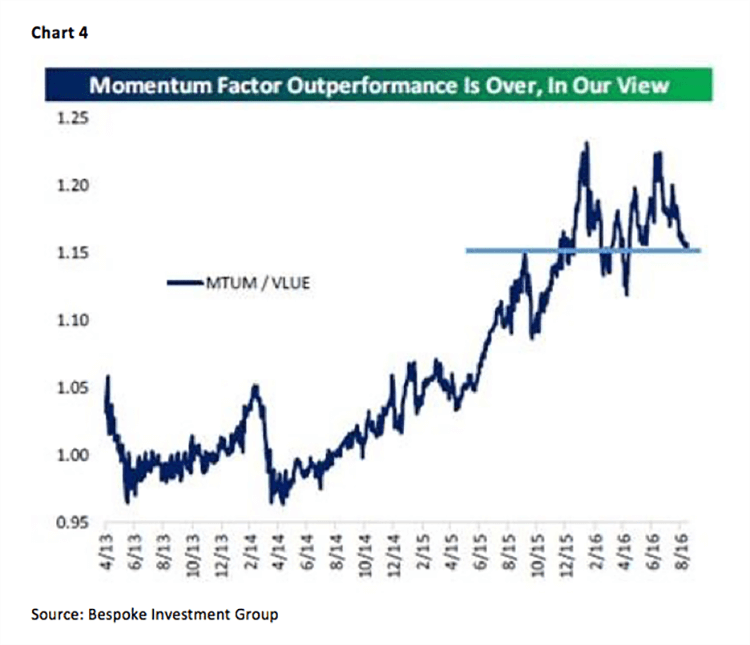

Finally, speaking to the question of momentum versus value, it is worth considering there is a chance that after a few years of underperformance, “value” may start to outperform. Using iShares MSCI MTUM ETF (MTUM/$77.82) as a momentum proxy, and iShares MSCI VLUE ETF (VLUE/$65.40) as a value proxy, Bespoke creates a ratio chart (chart 4). When the ratio line is rising momentum is outperforming and when it is falling value is outperforming. As can be seen, the chart is potentially at an inflection point. Using the top weighted 10 components in the VLUE, which have favorable ratings from our fundamental analysts and screen positive on my proprietary algorithm, produces this list: Apple (AAPL/$107.73/Outperform); Cisco (CSCO/$31.83/Outperform); and Wal-Mart (WMT/$72.50/Strong Buy). As for a list of names that could benefit from the Hurricane Hermine tragedy, which also carry favorable ratings from our fundamental analysts: Beacon Roofing Supply (BECN/$46.55/Strong Buy) and PGT, Inc. (PGTI/$11.98/Strong Buy).

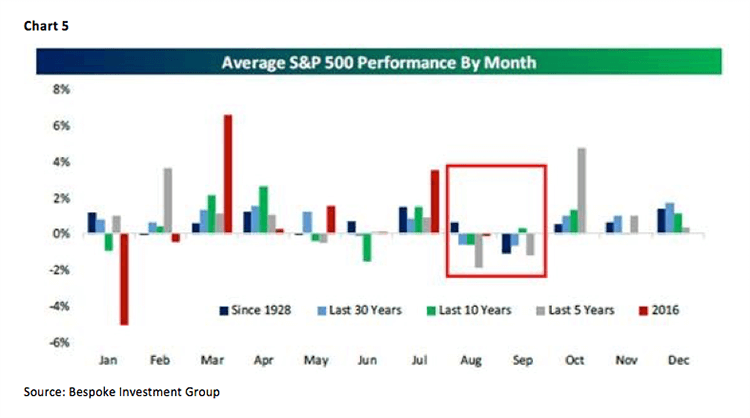

The call for this week: While everyone is focused on Hermine, almost unnoticed is that the Icelandic Meteorological Office, following two large earthquakes, is on alert for an eruption from Katla (Iceland’s largest volcano). Recall it was the Eyjafjallajökull eruption in 2010 that crippled Europe for a month and impacted the economy (Eyjafjallajokull). Meanwhile, bullish sentiment tags a three-year low among Wall Street strategists (not us), the negative nabobs continue to chant, “The D-J Transport refuse to confirm the D-J Industrial’s upside,” and the media is replete with how September is historically the worst month of the year for stocks (chart 5 on page 5). And that comment caused one old Wall Street wag to drag out Mark Twain’s stock market axiom, “OCTOBER: This is one of the peculiarly dangerous months to speculate in stocks. The other are July, January, September, April, November, May, March, June, December, August, and February.” We think a September interest rate ratchet is probably off the table and that the first point of potentially more serious vulnerability for the equity markets doesn’t arrive until mid/late-September. This morning the preopening futures are relatively flat on no real news overnight.