Yesterday, we got the release of the minutes from the FOMC meeting in July. Not surprisingly, we see a Fed just as confused as ever as to what monetary policy actions should be taken. To wit:

- FED OFFICIALS SPLIT IN JULY ON WHETHER RATE HIKE NEEDED SOON

- A COUPLE FED OFFICIALS BACKED JULY RATE HIKE

- FOMC VOTERS AGREED TO WAIT FOR MORE DATA TO GAUGE ECONOMY

- SEVERAL FED OFFICIALS CONCERNED OF FIN. RISKS FROM LOW RATES

- SEVERAL FED OFFICIALS SAW AMPLE TIME TO ACT IF INFLATION RISE

- FOMC VOTERS DIVIDED ON WHETHER JOB-GAIN PACE WORRISOME

As I wrote previously, I think the Fed is making a major policy mistake.

“First, with the markets making new all-time highs, there is a ‘price’ cushion available for the markets to absorb a rate hike without breaking important downside support.

Secondly, with Central Banks globally flooding the markets with liquidity, a further ‘shock absorber’ is currently engaged in softening the impact of a rate hike.

Lastly, the economy is likely going to show a bit of ‘strength’ in upcoming reports, with slightly stronger inflationary pressures. This pickup in economic strength will be another inventory restocking cycle following several months of weakness. As has been in the past, it will be transient and that strength will evaporate as quickly as it came.

If I was Janet Yellen, I would hike interest rates by .50 bps immediately in a surprise announcement and use the price and Central Bank liquidity cushions to soften the blow. This would move the Fed towards its goal of reloading its primary policy tool while there is some ability to temporarily control the outcome of the rate hike.

But that is just me. She won’t do it.”

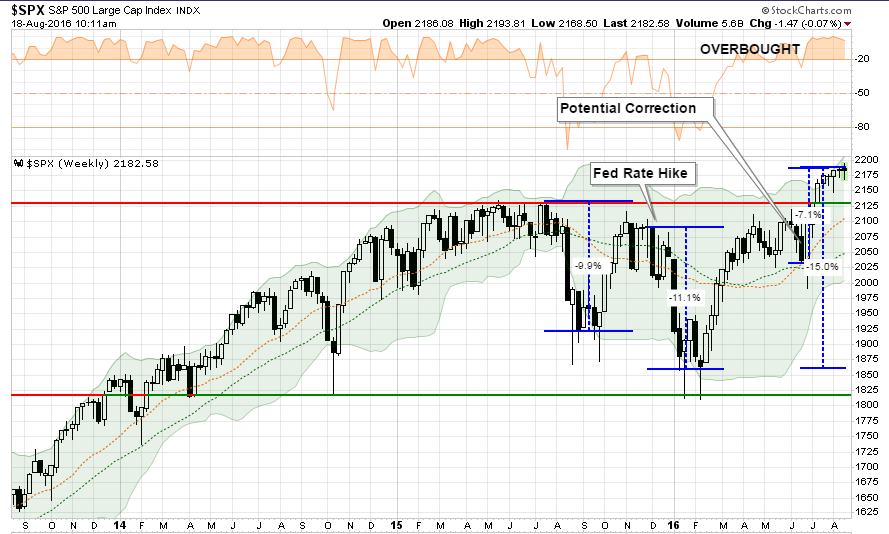

Technically, a correction due to a surprise rate hike might sting a bit but would likely remain well within the confines of a “bull market correction” as shown below. The previous two corrections, leading up to and following the last Fed hike, were between 10-11%. I have noted a minimum/maximum correction potential from a rate hike of between 7-15%.

My point, as stated above, is the Fed is likely missing a significant opportunity to use the market’s current “exuberance” to achieve two goals.

- Hike rates to catch up with LIBOR which is already tightening monetary policy, and;

- Reduce some of the exuberance in the markets which the Fed is now concerned with.

“… during the discussion, several participants commented on a few developments, including potential overvaluation in the market for CRE, the elevated level of equity values relative to expected earnings, and the incentives for investors to reach for yield in an environment of continued low interest rates.”

The Liquidity Trap

What the dichotomy of the data, markets, and Fed actions suggests, now more than ever, is the realization the Fed has gotten caught in a “liquidity trap.”

Here is the definition:

“A liquidity trap is a situation described in Keynesian economics in which injections of cash into the private banking system by a central bank fail to lower interest rates and hence fail to stimulate economic growth. A liquidity trap is caused when people hoard cash because they expect an adverse event such as deflation, insufficient aggregate demand, or war. Signature characteristics of a liquidity trap are short-term interest rates that are near zero and fluctuations in the monetary base that fail to translate into fluctuations in general price levels.”

Let’s take a moment to analyze that definition by breaking it down into its overriding assumptions.

First, there is little argument that Central Banks globally are injecting liquidity into the financial system.

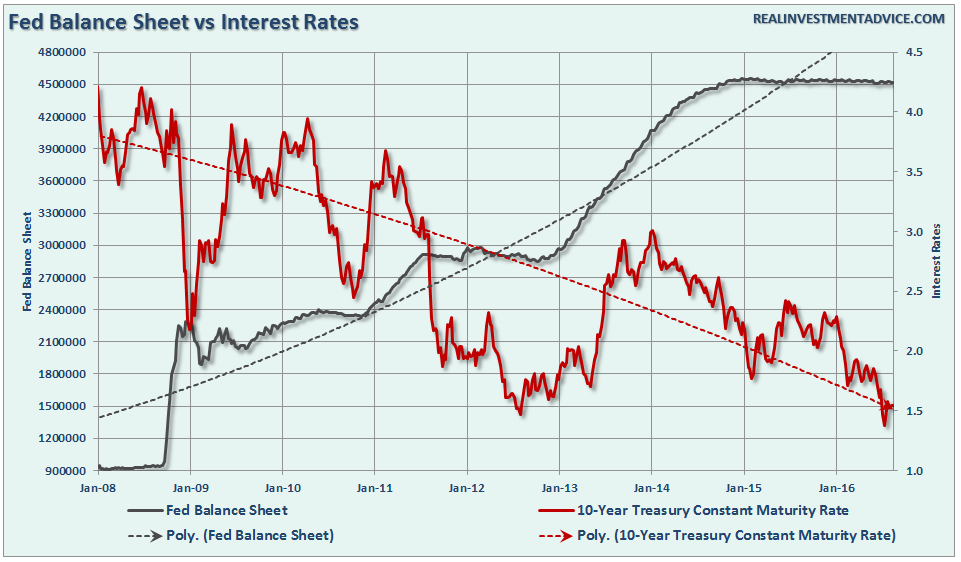

However, has the increase in liquidity into the private banking system lowered interest rates? That answer is also“yes.” The chart below shows the increase in the Federal Reserve’s balance sheet, since they are the “buyer” of bonds, which in turn increases the excess reserve accounts of the major banks as compared to the 10-year treasury rate.

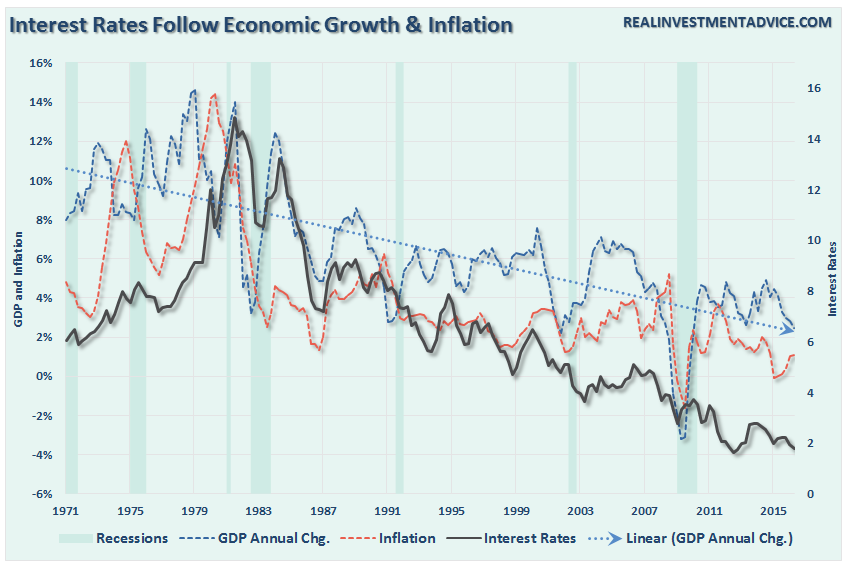

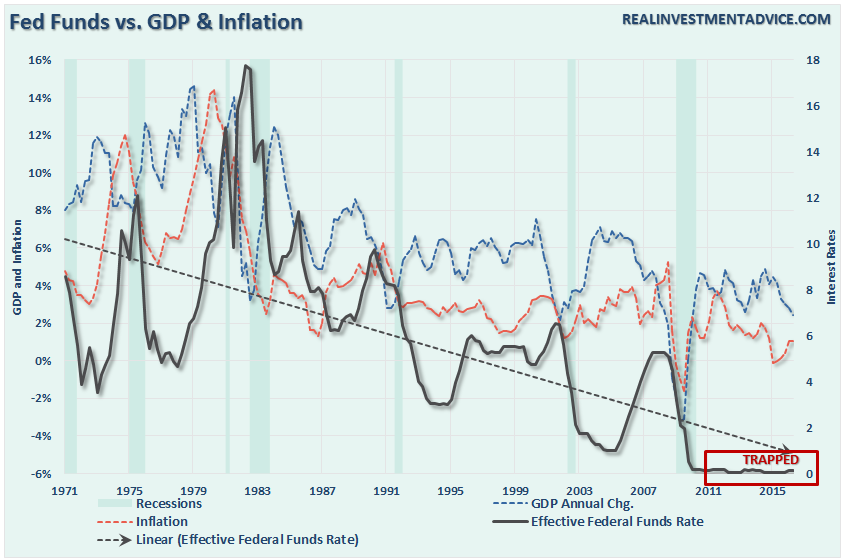

While, in the Fed’s defense, it may be clear that since the beginning of the Fed’s monetary interventions that interest rates have declined this has not really been the case. I would venture to argue that, in fact, the Fed’s liquidity driven inducements have done little to affect the direction of interest rates. I say this because interest rates have not been falling just since the monetary interventions began – it is a phenomenon that began three decades ago as the economy began a shift to consumer credit leveraged service society. The chart below shows the correlation between the decline of GDP, Interest Rates and Inflation.

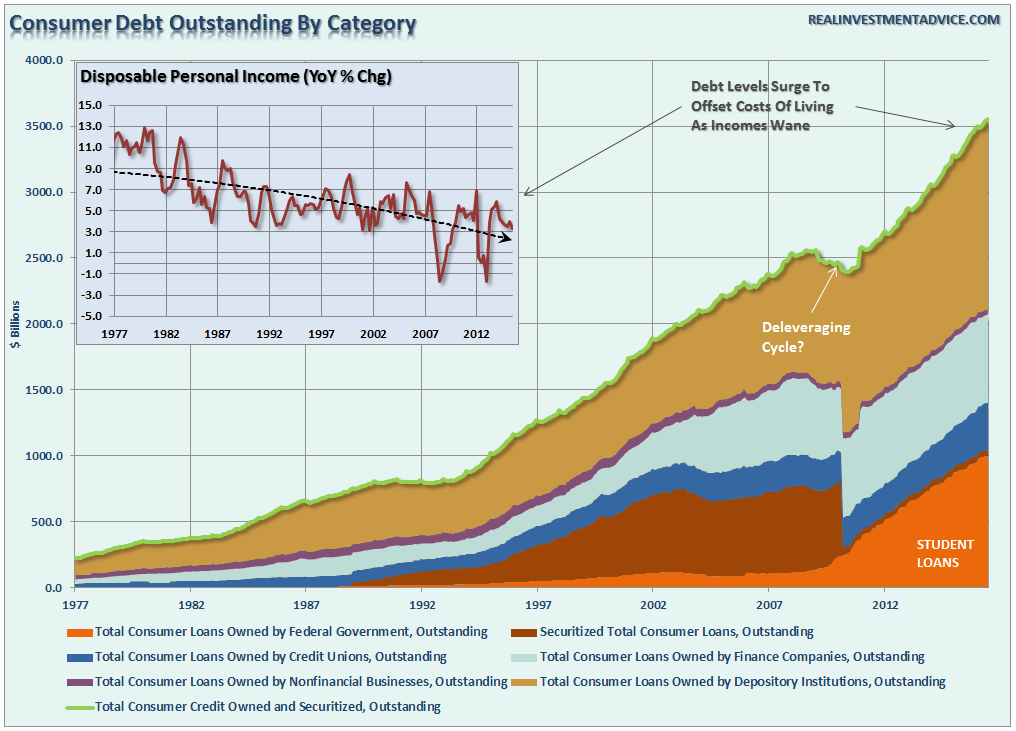

The ongoing decline in economic activity has continued to be the driving force behind falling inflationary pressures and lower interest rates and massive surges in consumer debt to sustain an increased level of living standards.

For these reasons, it is difficult to attribute much of the recent decline in interest rates to monetary/accommodative policies when the long term trend was clearly intact before these programs began. The real culprits behind the declines in economic growth rates, interest rates, and inflation are more directly attributable to increases in productivity, globalization, outsourcing and leverage (debt service erodes economic activity).

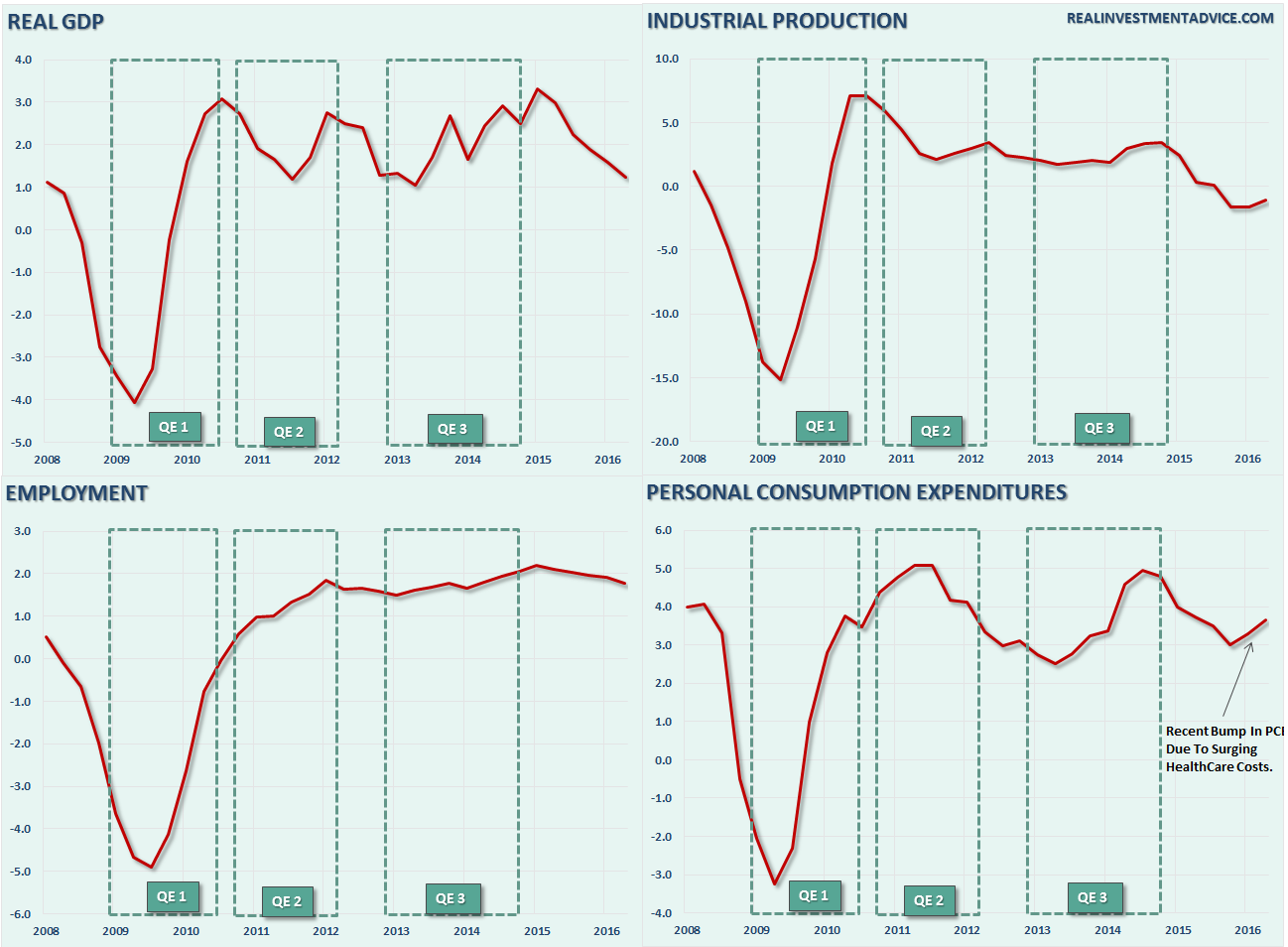

However, the real question is whether, or not, all of this excess liquidity and artificially low interest rates is spurring economic activity? To answer that question let’s take a look at a 4-panel chart of the most common measures of economic activity – Real GDP, Industrial Production, Employment, and Consumption.

While an argument could be made that the early initial rounds of QE contributed to the bounce in economic activity it is important to also remember several things about that particular period. First, if you refer to the long term chart of GDP above you will see that economic growth has ALWAYS surged post recessionary weakness. This is due to the pent up demand that was built up during the recession that is unleashed back into the economy. Secondly, during 2009 there were multiple bailouts going on from “cash for houses”, “cash for clunkers”, direct bailouts of the banking system and the economy, etc. However, the real test for the success of the Fed’s interventions actually began in 2010 as the Fed became “the only game in town”. As shown above, at best, we can assume that the increases in liquidity have been responsible in keeping the economy from slipping into a secondary recession. With most economic indicators showing signs of weakness it is clear that the Federal Reserve is currently experiencing a diminishing rate of return from their monetary policies.

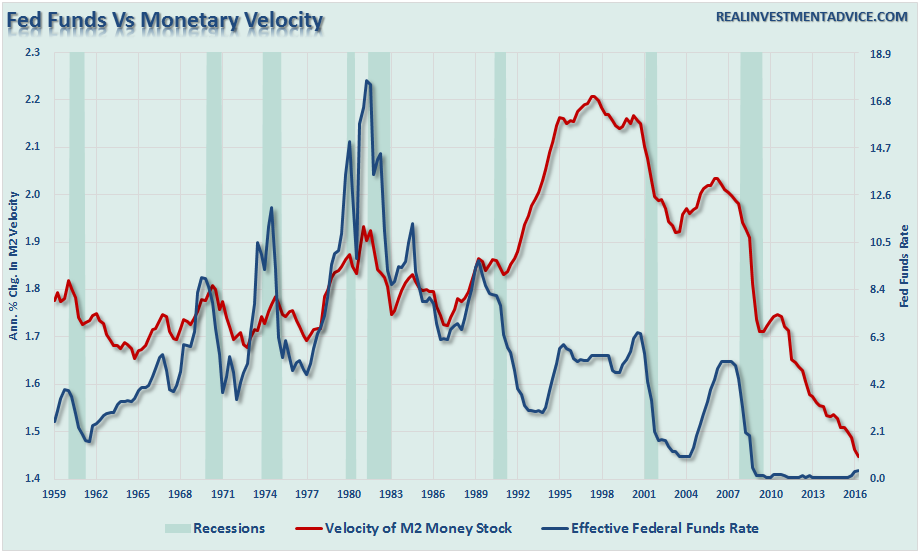

Lack Of Velocity

The definition of a “liquidity trap” also states that people begin hoarding cash in expectation of deflation, lack of aggregate demand or war. As the “tech bubble”eroded confidence in the financial system, followed by a bust in the credit/housing market, and wages have failed to keep up with the pace of living standards, monetary velocity has collapsed to the lowest levels on record.

The issue of monetary velocity is the key to the definition of a “liquidity trap.” As stated above:

“The signature characteristic of a liquidity trap are short-term interest rates that are near zero and fluctuations in the monetary base that fail to translate into fluctuations in general price levels.”

The chart below shows that, in fact, the Fed has actually been trapped for a very long time.

The problem for the Fed has been that for the last three decades every time they have tightened monetary policy it has led to an economic slowdown or worse. The onset of economic weakness then forced the Federal Reserve to once again resort to lowering interest rates to stabilize the economy.

The issue is with each economic cycle rates continued to decrease to ever lower levels. In the short term, it appeared that such accommodative policies did in fact aid in economic stabilization as lower interest rates increased the use of leverage. However, the dark side of those monetary policies was the continued increase in leverage which led to the erosion of economic growth, and increased deflationary pressures, as dollars were diverted from productive investment into debt service. Today, with interest rates at zero, the Fed has had to resort to more dramatic forms of stimulus hoping to encourage a return of economic growth and controllable inflation.

No Escape From The Trap

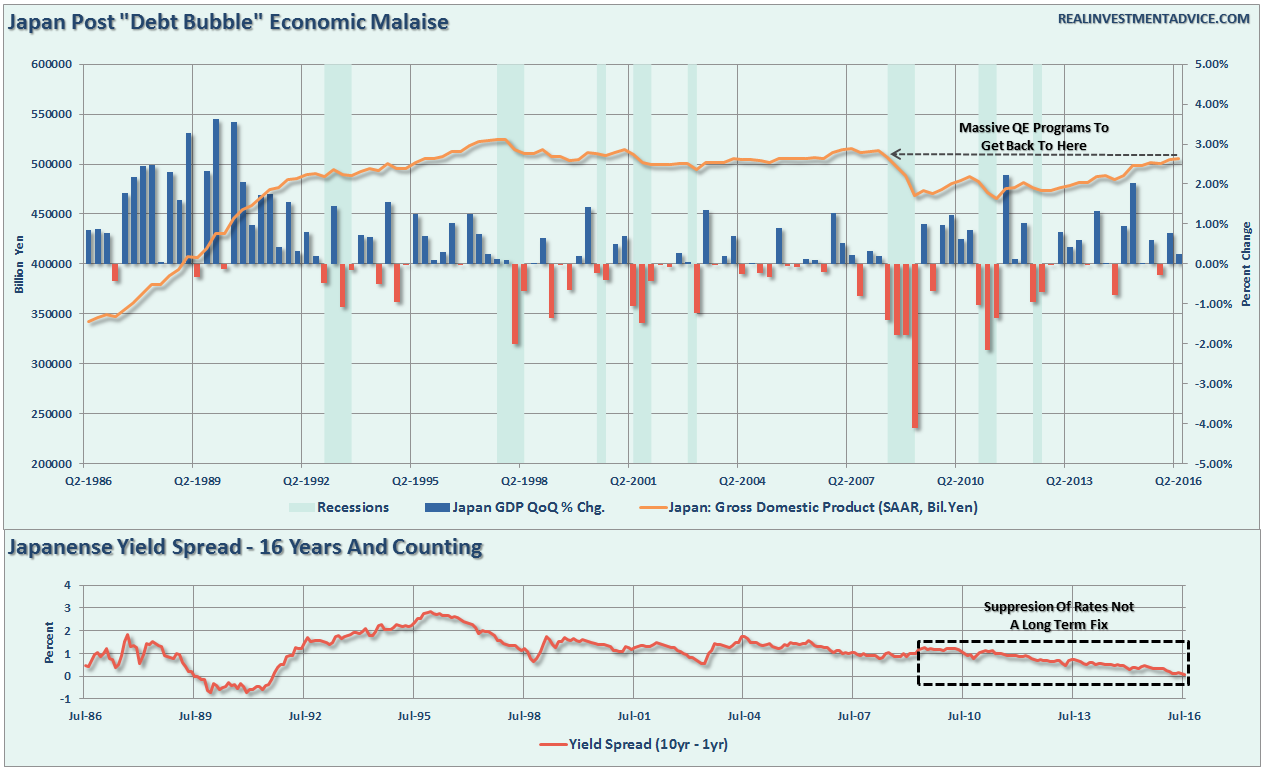

For the Federal Reserve, they are now caught in the same “liquidity trap” that has been the history of Japan for the last three decades. With an aging demographic, which will continue to strain the financial system, increasing levels of indebtedness and poor fiscal policy to combat the issues restraining economic growth it is unlikely that continued monetary interventions will do anything other than simply foster the next boom/bust cycle in financial assets. The chart below shows the 10-1-year Japanese Government Bond yield spread as compared to their quarterly economic growth rates. Low interest rates have failed to spur sustainable economic activity over the last 20 years.

The real concern for investors, and individuals, is the actual economy. We are likely experiencing more than just a ‘soft patch’ currently despite the mainstream analysts’ rhetoric to the contrary. There is clearly something amiss within the economic landscape and the ongoing decline of inflationary pressures longer term is likely telling us just that. The big question for the Fed is how to get out of the ‘liquidity trap’ they have gotten themselves into without cratering the economy, and the financial markets, in the process.

Should we have an expectation that the same monetary policies employed by Japan will have a different outcome in the U.S? More importantly, this is no longer a domestic question – but rather a global one since every major central bank is now engaged in a coordinated infusion of liquidity. The problem is that despite the inflation of asset prices, and suppression of interest rates, on a global scale there is scant evidence that the massive infusions are doing anything other that fueling the next asset bubbles in real estate and financial markets. The Federal Reserve is currently betting on a “one trick pony” which is that by increasing the “wealth effect” it will ultimately lead to a return of consumer confidence and a fostering of economic growth? Currently, there is little real evidence of success.

Are we in a “liquidity trap?” Maybe. Of course, no one recognized Japan’s problems either until it was far too late.

Lance Roberts

Lance Roberts is a Chief Portfolio Strategist/Economist for Clarity Financial. He is also the host of “The Lance Roberts Show” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report".

© Real Investment Advice

© Real Investment Advice

Read more commentaries by Real Investment Advice