The high yield municipal bond market continues to attract strong inflows as yields in other fixed income sectors are expected to be low for long periods. David Hammer, head of municipal bond portfolio management, and Sean McCarthy, head of municipal credit research, discuss PIMCO’s outlook for the high yield municipal market, the themes that have contributed to PIMCO High Yield Municipal Bond Fund’s recent performance – and why rigorous, forward-looking credit selection is the key to generating alpha.

Q: What are the broad trends you are seeing in the high yield municipal market?

A: The asset class has experienced strong performance and municipal funds have received $33 billion of inflows year to date through June 30. Valuations continue to rally. The Barclays Municipal Bond Index returned 4.33% in the first half of 2016 while the Barclays High Yield Municipal Bond Index returned 7.98% over the same period.

Some investors wonder if there is still value in the municipal market at these elevated prices and lower yields. We believe the macro environment remains supportive of the municipal asset class. We see a U.S. economy that continues to expand, which is generally good for municipal credit fundamentals. At the same time, global aggregate growth has been lackluster and inflation expectations remain muted. This is important for municipals, as increasing rates, particularly in the long end, and periods of heightened interest rate volatility can lead to outflows from the asset class and periods of underperformance. We expect municipals will remain in a macro sweet spot of improving fundamentals, without a lot of upward pressure on long-term U.S. interest rates.

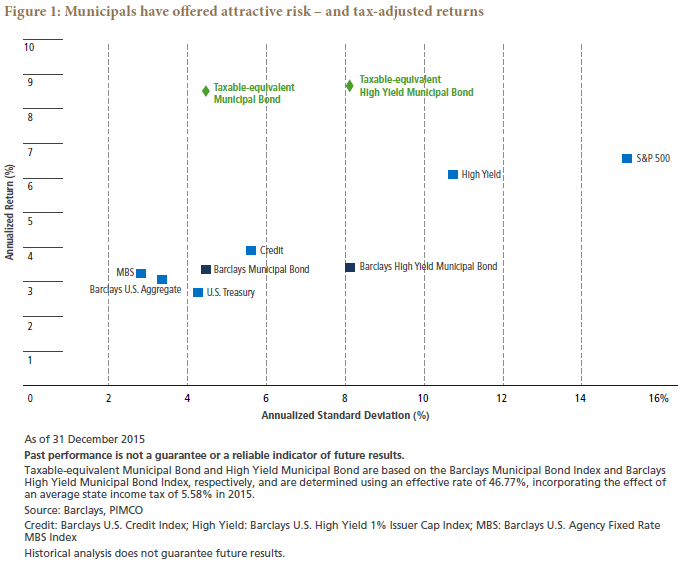

In addition, one of the powerful drivers of total returns in municipals is that their income streams are federally tax-exempt and, in some cases, exempt from state and local taxes as well. Over the last decade, tax-exempt municipals on a tax-adjusted basis have outperformed virtually all other asset classes, including equities, with about half the volatility of the S&P 500 (See Figure 1). In a New Neutral world of low absolute rates and lower expected returns, thattax-exempt income stream has become increasingly valuable to investors.

And municipal defaults remain low. Baa-rated municipals continue to default less frequently than Aaa-rated corporates (see Figure 2). High yield is a little bit of a misnomer in the muni market; it’s high yield relative to investment grade municipals, but historical default rates are significantly lower than high yield taxable counterparts.

Q: Looking at some of the areas where you’re investing, tobacco bonds have had a tremendous run in the past year. Are you

still bullish?

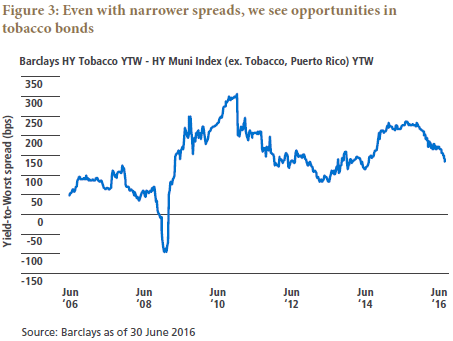

A: Yes, MSA (Master Settlement Agreement) tobacco bonds – which are secured by a claim on a perpetual stream of annual settlement payments owed from the U.S. tobacco manufacturers to the states following the landmark 1998 court settlement – remain relatively attractive. These bonds have been trading with an excess risk premium relative to most other below investment grade municipals aside from Puerto Rico, but with an improved liquidity profile. The sector continues to perform very well even after returns of 19.21% in 2014, 15.75% in 2015, and 13.65% in the first half of 2016. The spread has come in; it was as wide as 225 basis points a year ago versus other high yield municipal bonds (see Figure 3). After the rally, we still see that spread as approximately 100 basis points of additional pickup by owning tobacco bonds instead of on-the-run non-tobacco and non-Puerto Rico high yield municipals. We’ve reduced our weight to the sector somewhat as prices have rallied, but tobacco bonds remain a core fund holding. We still see value at current levels with the added benefit of increasing portfolio liquidity. MSA tobacco bonds are among the most actively traded municipal bonds.

Q: Several years ago, PIMCO’s municipal portfolios eliminated exposure to Puerto Rico bonds after determining they had too much risk in light of likely developments in the Commonwealth’s ability to service its debt. Now that President Obama signed a law to address the island’s economic and fiscal crisis, will the bonds be a good investment?

A: Puerto Rico still has a long way to go before an upward-sloping credit trajectory materializes. However, the situation may be reaching an inflection point following a historic default by the Commonwealth of general obligation debt on July 1 and the passage of the federal legislation referred to as PROMESA. PROMESA creates a seven-member federally appointed oversight board tasked with restructuring all of Puerto Rico’s liabilities, including unfunded pension obligations, in a manner that respects “relative” priorities of “lawful liens.” This assurance is helpful when considering Puerto Rico as an investment because it provides a modicum of comfort that local constitutional priorities will be respected under the federal law. Still, it is unclear who the U.S. Congress and President will appoint on the oversight board, and outcomes for all constituents will depend on the board’s composition.

It would be naïve to believe the oversight board’s overriding priority will be to fulfill all of its debt obligations. The oversight board has 14 requirements to consider when crafting a credible fiscal plan for the Commonwealth. These requirements include, among others, eliminating structural imbalances, maintaining essential public services, providing adequate funding of public pensions, examining debt sustainability and improving fiscal governance and internal controls. All of these items must be carefully balanced against an economy that continues to shrink and remains susceptible to exogenous shocks, including global recession, global central bank policy mishaps and, perhaps most topical, fear of a spreading Zika virus. Reports of increasing cases of the Zika virus should not be downplayed as it may have implications for Puerto Rico’s future migration patterns and tourism, an industry that has been among the few bright spots for the economy. Outmigration has always been a key risk and an argument against further austerity; it could potentially accelerate this year.

Puerto Rico bonds continue to trade at deep dollar price discounts and steep yields, which may create opportunity to the extent these discounts accurately capture the impending haircuts to bondholders. But determining how much cash flow relief is required to credibly and sustainably support the 14 requirements of the fiscal plan is something we may not understand until the oversight board is appointed and releases a draft of the plan. Until then, investors must be very cautious about relying on subjective probabilities ascribed to debt restructuring scenarios. Accordingly, we remain wary of debt issued by Puerto Rico’s primary government, including general obligation bonds, which remain subject to unknown unknowns and a high degree of variability around known fiscal parameters. At some point, we may become active in Puerto Rico, but investments in obligations of the primary government require demonstration that when Puerto Rico exits federal oversight, it does so with a sustainable debt burden and a credible economic model.

Q: Does PROMESA have implications for the broader municipal market?

A: We do not believe so. While some of the island’s fiscal difficulties, such as large unfunded pensions, are found elsewhere in the U.S. municipal market, Puerto Rico demonstrates many more serious structural problems that are unique and not observed elsewhere in the market on a similar scale. It is also important to understand that PROMESA is permissible only because of the Territorial Clause of the U.S. Constitution which ensures that no negative legal precedents will be established by the law. Finally, we believe PROMESA provides the market greater certainty to what was previously an uncertain situation. This solution is a good outcome for the municipal market as a whole.

Q: You also like senior living bonds. Why?

A: We’ve seen a lot of opportunity in senior living bonds over the last year; demographics are extremely supportive. Senior living retirement communities tend to be occupied by individuals in their late 70s to early 80s. Our preference for this sector is a reflection of baby boomers getting older: Outsized population growth in that age range is a secular trend that we expect to continue for a number of years.

Within this sector, we’re looking for areas with stable demand trends that have a need for additional capacity. We are also measuring affordability based on the relationship between local housing prices and anticipated entrance fees. We prefer operators with proven track records and those that can leverage economies of scale through larger systems.

Q: Where else do you see opportunities in high yield municipals?

A: We have found opportunities in a number of unique credits that leverage PIMCO’s ability to tap into experts from other areas of our firm, including our real estate team. One example is a recent high-rise project in lower Manhattan, a hybrid muni/CMBS (commercial mortgage-backed securities) deal that combines construction risk and tenant lease-up risk with public sector support. The project’s bonds have rallied to less than 3% as of June 30 from 5%-5.375% when they were issued in 2014. This was a unique construction financing opportunity that utilized our municipal team’s ability to examine hybrid assets with a commercial real estate bent. Our real estate experts helped our municipal team analyze the supply/demand trends of the New York City commercial real estate market and compare leverage and deal features to that of CMBS deals.

More recently, in January we found opportunity in a bond deal linked to a major medical school through the Build NYC Resource Corporation. This bond has rallied from 5.5% at issuance to under 3% as of June 30. While the credit was unrated by the rating agencies, our analysts saw an opportunity to invest in a prestigious medical school previously affiliated with an institution that struggled to properly manage the asset. The transaction allowed one of New York’s largest healthcare systems to acquire a controlling interest in the school and target operational efficiencies. The new management is implementing a successful turnaround strategy and a reinvigorated philanthropic campaign.

It’s interesting to note that Puerto Rico bonds have rallied in recent months as the market anticipated the passage of PROMESA, and PIMCO’s municipal strategies did not have exposure. As previously stated, PIMCO believes risks to most Puerto Rico governmental bonds remain skewed to the downside, but we continue to assess the opportunities in the Territory.

Q: Are high yield municipals in the commodity-related sector showing promise following the recent rebound in oil prices?

A: It’s not just oil, but also other commodities. Many industrial corporates issue parity senior unsecured debt in the tax-exempt muni market. We have seen some opportunity here, but there is still a big divergence in prices between the muni market and the taxable corporate market for a number of BB- and B-rated issuers. In the event of a restructuring, unsecured municipals and corporates will receive the same recovery, and because of this fact, the risk/reward profile in many of commodity-related muni bonds remains skewed to the downside.

That said, we have seen some opportunities in the commodity-related project finance space. For example, a bond was issued to build a major rail terminal in Texas. The project derives its revenues from terminal services, which include loading/unloading, blending and storage of crude oil and refined products delivered by train, truck or ship. PIMCO’s integrated investment process was key to analyzing the opportunity to purchase this unrated deal, as it required input from both our municipal and commodity teams. The bond has rallied from 7.25% when the deal was issued in February to around 5.5% as of June 30.

Q: How does PIMCO think about analyzing the municipal market?

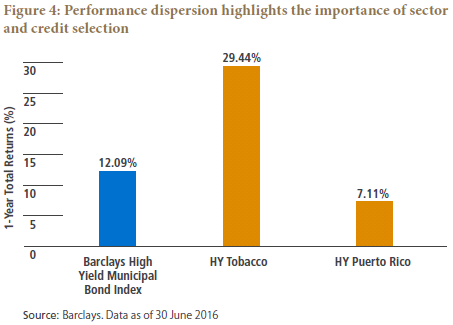

A: We’re not a standalone municipal business. For investors who rely on a more traditional municipal analysis or a ratings agency, Puerto Rico highlights the risk of not having access to an integrated investment process with forward-looking sector and credit selection (see Figure 4).

The diverse and complex high yield municipal market includes asset-backed securities, corporate-backed bonds, commodity-linked project-financed bonds and bonds with fundamentals based on trends in residential and commercial real estate. An integrated investment process with access to expertise in all of these areas is crucial to delivering long-term returns. Of course, all investments contain risk and even the most thorough, forward-looking investment process is not a crystal ball to see the future of markets and economies.

Our municipal team can rely on more than 50 global credit analysts at PIMCO. When we are deciding whether to buy a security, we have input from analysts who have expertise in a wide variety of specialties, such as corporate credit, mortgage-backed securities, asset-backed securities and commodity prices. This is what sets us apart. With the municipal market growing more complex, investors should consider active management.