There has been a litany of articles written recently discussing how the stock market is set for a continued bull rally. The are some primary points that are common threads among each of these articles which are that interest rates are low, corporate profitability is set to recover and the Central Banks monetary accommodations continue to put a floor under stocks. I do not disagree with any of those points.

The concern with each of those points, which are supporting higher asset prices, is they are all artificially influenced by outside factors. Interest rates are low because of the Federal Reserve’s actions, corporate profitability is high due to accounting rule changes following the financial crisis and Central Banks globally are pushing liquidity directly into the financial system.

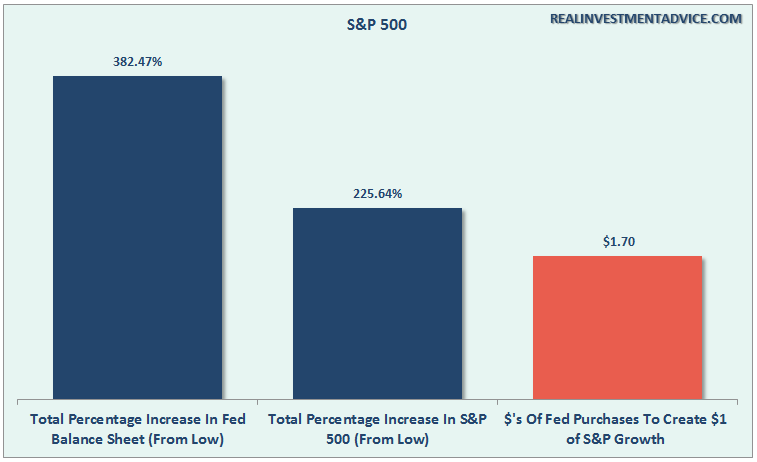

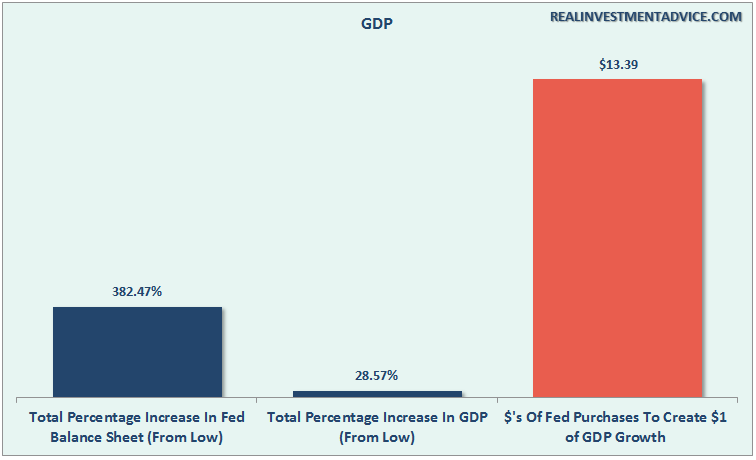

The stock market has rallied sharply in direct correlation to the expansion of the Fed’s balance sheet yet economic growth has floundered much to the dismay of the Federal Reserve.

With this in mind, I do have a few questions that would like to ask in order to stimulate your thinking?

Employment

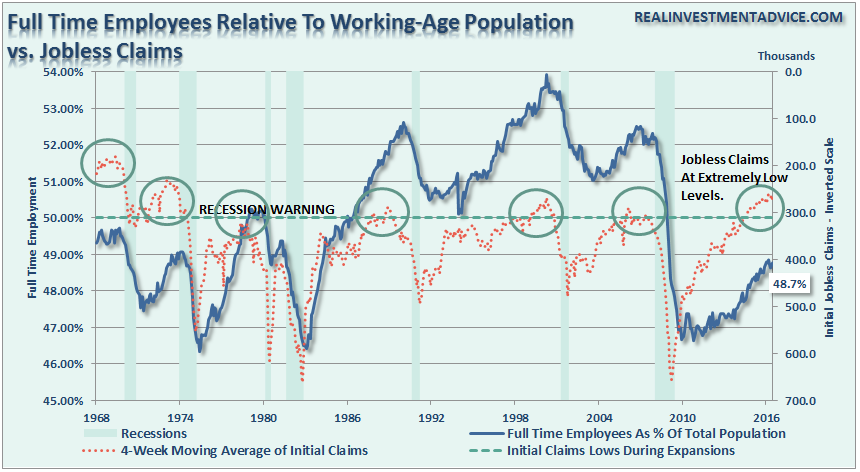

Employment is the lifeblood of the economy. Individuals cannot consume goods and services if they do not have a job from which they can derive income. Therefore, in order for individuals to consume at a rate to provide for sustainable, organic (non-Fed supported), economic growth they must be employed at a level that provides a sustainable living wage above the poverty level. This means full-time employment that provides benefits and a livable wage. The chart below shows the number of full-time employees relative to the population. I have also overlaid jobless claims (inverted scale) which shows that when claims fall to current levels, it has generally marked the end of the employment cycle and preceded the onset of a recession.

Question: Does the current level of employment support current asset valuations and the assumption of a continued bull market?

Personal Consumption Expenditures (PCE)

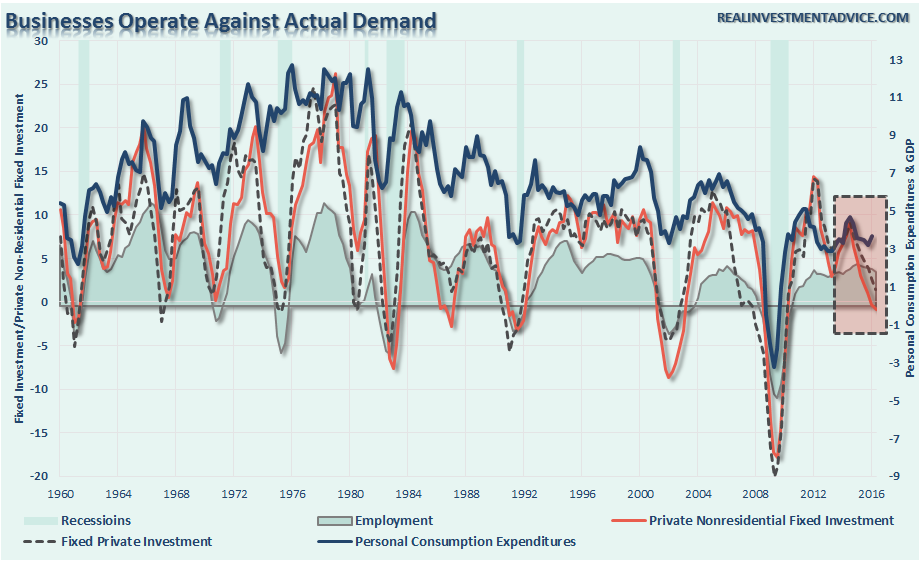

Following through from employment; once individuals receive their paycheck they then must consume goods and services in order to live. Personal Consumption Expenditures (PCE) is a measure of that consumption and comprises more than 70% of GDP currently.

PCE is also the direct contributor to the sales of corporations which generates their gross revenue. So goes personal consumption – so goes revenue. The lower the revenue that comes into companies the more inclined businesses are to cut costs, including employment, to maintain profit margins.

The chart below is a comparison of the annualized change in PCE to businesses fixed investment and employment.

Question: Does the current weakness in PCE and Fixed Investment support the current rise in asset prices or expectations of continued “strong” employment?

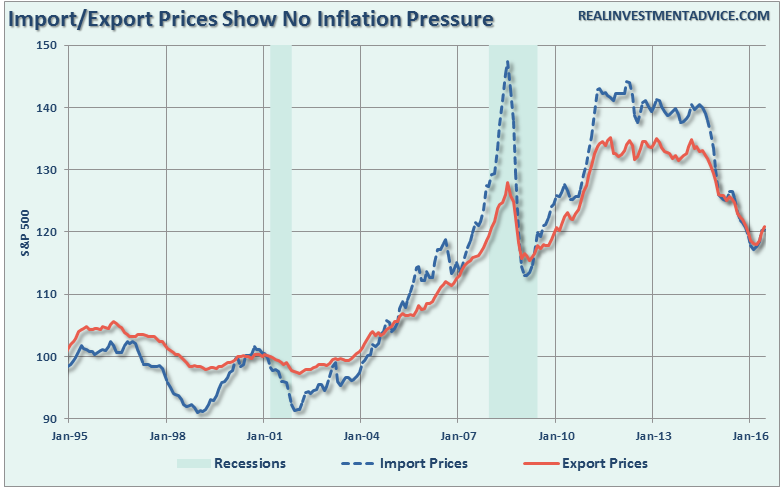

Import / Export Prices

As we continue to “follow the money” it is important to review what corporations are receiving for the goods and services that are being exported as well as what they are paying for goods and services being imported. More than 40% of corporate profits today come from the exports of goods and services. Therefore, declines in prices received from exported goods directly affect profit margins. Declines in prices of imported goods and services are a reflection of consumer demand. The chart below looks at import and export prices. Historically, sharp declines in prices have either been a precursor to, or coincident with, the onset of a recession.

Question: Are falling import and export prices supportive of the current market?

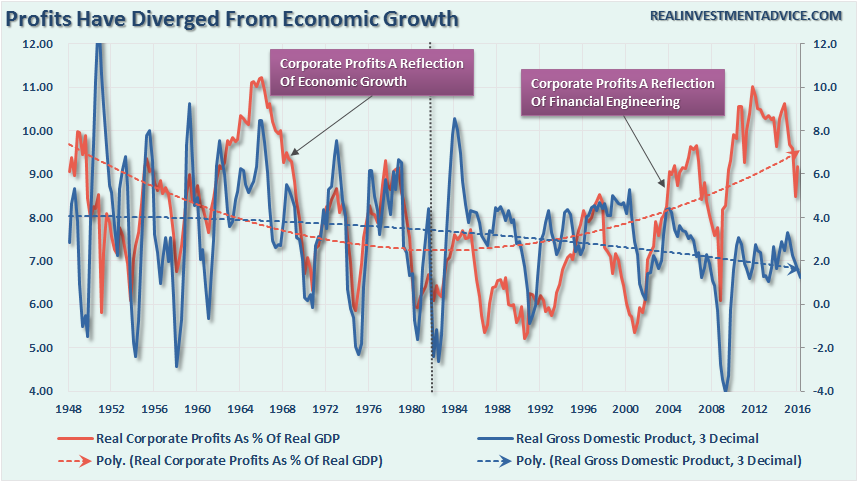

Corporate Profits As % Of GDP

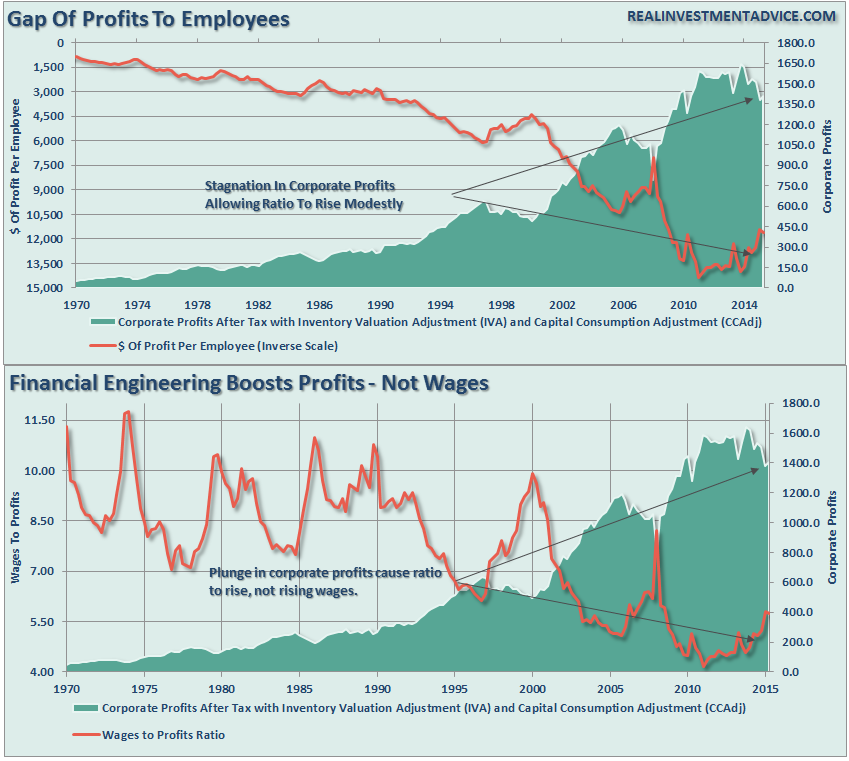

Following the corporate profit story, we can look directly at corporate profits. Over the last several years, companies have manufactured profitability through a variety of accounting gimmicks, expanded share buybacks through increased leverage and continued increases in productivity. However, that profitability has come at the expense of“Main Street” as employment and wages have not risen. I discussed this recently stating:

“The annual rate of change in personal incomes has been on a decline since the turn of the century. This is a function of both the structural shift in employment (higher productivity = less employment and lower wage growth) and the drive to increase corporate profitability in the midst of weaker consumption.

The chart below shows the disparity between corporate profits and employment and wages.”

“While corporate profitability has surged since the financial crisis, those profits have come at the expense of employees. Since 2009, wages for “non-supervisory employees,” which is roughly 83% of the current workforce, is lower today than when Obama first took office.”

The decline in economic growth epitomizes the problem that corporations face today in trying to maintain profitability. The chart below shows corporate profits as a percentage of GDP relative to the annual change in GDP. As you will see the last time that corporate profits diverged from GDP it was unable to sustain that divergence for long and economic growth subsequently declined with it.

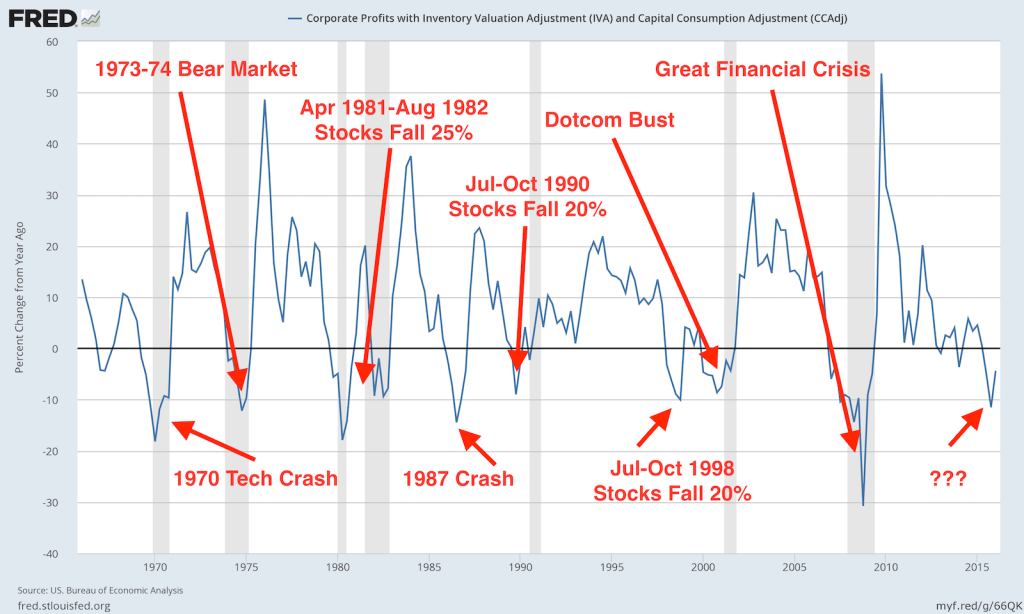

As Jesse Felder recently noted:

“It’s earnings season once again and it looks as if, as a group, corporate America still can’t find the end of its earnings decline since profits peaked over a year ago. What’s more analysts, renowned for their Pollyannish expectations, can’t seem to find it, either.

In other words, buying the new highs in the S&P 500 today means you believe ‘this time is different.’ It could turn out that way, but history shows that sort of thinking to be very dangerous to your financial well-being.”

Question: How long can asset prices remain divorced from falling corporate profits and weaker economic growth?

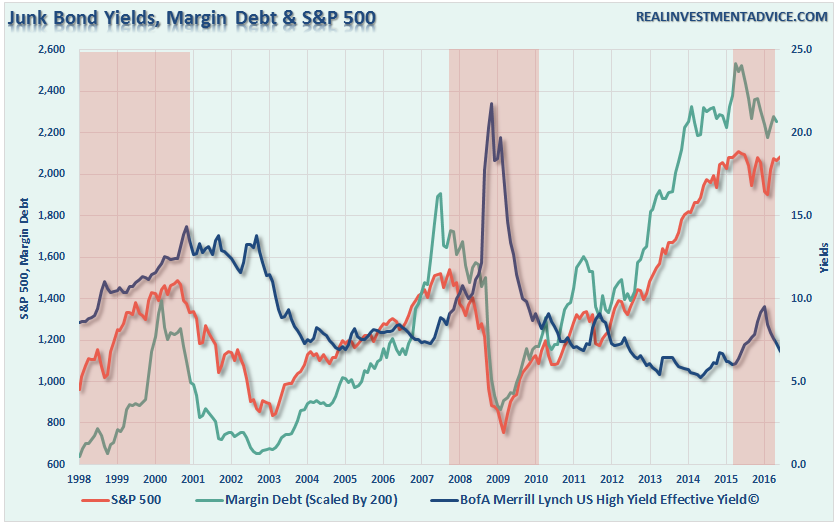

Margin Debt Vs. Junk Bond Yields

As stated above, global Central Banks have lulled investors into an expanded sense of complacency. The problem is it has led to a willful blindness and disregard of the underlying fundamentals as asset prices have risen with seemingly reckless abandon. The complete lack of “fear” in the markets combined with a “chase for yield” has driven “risk”assets to record levels. The rise in leverage also supports this idea.

The chart below shows the relationship between margin debt (leverage), stocks and junk bond yields. This didn’t end well last time as the reversion in the assets triggered repeated margin calls leading to a cycle of forced liquidations.

Question: What is the possibility of this divergence being maintained indefinitely?

Being bullish on the market in the short term is fine – you should be. Central Banks have rushed in every burning building with a “fire hose” of liquidity each time a crisis has presented itself. So far it has worked.

However, the problem is that a crisis, which is ALWAYS unexpected, inevitably will trigger a reversion back to the fundamentals. What will that catalyst be? I don’t have a clue and neither does anyone else. But disregarding reality in a quest to chase market-based returns has ALWAYS ended badly when the “herd” inevitability turns.

It has never been, and will not be, a slow and methodical process but rather a stampede with little regard to valuation or fundamental measures. As prices decline it will trigger margin calls which will induce more indiscriminate selling. The vicious cycle will repeat until margin levels are cleared and selling is exhausted.

The reality is that the stock market is extremely vulnerable to a sharp correction. Currently, complacency is near record levels and no one sees a severe market retracement as a possibility. The common belief is that there is “no bubble” in assets and the Federal Reserve has everything under control. The question you have to answer, is whether or not that is actually the case?

“Wall Street is a street with a river at one end and a graveyard at the other.” – Fred Schwed, Jr.

Lance Roberts

Lance Roberts is a Chief Portfolio Strategist/Economist for Clarity Financial. He is also the host of “The Lance Roberts Show” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, and Linked-In