SUMMARY

- Managed futures and multi-strategy mutual funds have soared in popularity over the past few years as investors search for strategies designed to provide reliable portfolio diversification and attractive returns.

- Yet investors need to select managers carefully: Style and performance vary widely, and only a subset delivered during sharp equity sell-offs.

- Pairing managers with differentiated yet complementary approaches may aid diversification and return potential.

Managed futures and multi-strategy mutual funds have soared in popularity over the past few years as investors search for strategies designed to provide reliable portfolio diversification and attractive returns. In total, investors poured $37 billion into these funds from December 2014 through May 2016 alone, according to Morningstar.

However, investors considering these categories would be wise to take a close look at how specific funds have performed. The past three years show a significant variation in style across managers. While some delivered attractive returns, only a subset delivered when it counted most – during sharp sell-offs in equity markets.

We think the traditional playbook for evaluating managers needs to be altered when picking funds in these categories. Assessing philosophy, process, people and performance remains important, but investors also need to ask a different set of questions to ensure they not only select the right managers, but also have an optimal pairing. Furthermore, wide variation in performance implies “over-diversification” is a key risk – having too many managers increases the chances results will likely be subpar.

Below, we offer a simple framework to help identify the right managers for investors who seek diversification benefits from these strategies.

State of play

Managed futures, also known as trend-following or momentum funds, are gaining popularity as a portfolio diversifier and a potent antidote to equity market sell-offs. Multi-strategy funds, which provide access to multiple strategies and/or managers in a single fund, continue to gain traction as a perceived “one-stop” solution for investors looking to allocate assets to liquid alternatives (see Figure 1). Combined, these categories have captured the majority of flows into liquid alternative mutual funds since December 2014.

Given relatively short track records, many of these funds can be difficult to evaluate. However, a review of the past three years’ performance, which encompasses track records for a sizable segment of funds in each category, provides valuable insights.

What is my manager’s equity beta?

Equity beta, which measures the magnitude and direction of a fund’s movement with the equity markets, is a useful metric to gauge how sensitive a fund’s performance is to equity market gyrations. On average, funds with low or negative equity beta tend to be better equity diversifiers.

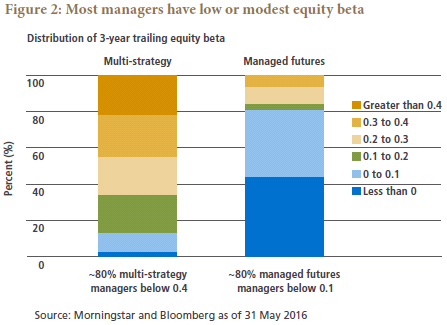

Looking at the last three years, overall diversification provided by most managers is good – the majority of managed futures and multi-strategy managers have low equity betas, as shown in Figure 2. However, investors still need to be careful. For example, one out of five multi-strategy managers has an equity beta higher than 0.4; i.e., a 10% decline in equities is likely to cause the fund to lose around 4%.

Along with low equity beta, did the manager deliver attractive returns?

Low equity beta is important, but not sufficient. There’s little benefit if the diversification potential comes at the cost of paltry, or worse, negative returns. As Figure 3 shows, performance dispersion across managers in both categories can be large. For example, returns delivered by the 20th and 80th percentile managers for multi-strategy funds differed by close to four percentage points. For managed futures funds, the difference was even higher, close to seven percentage points. Put simply, investors are getting paid to diversify with only a subset of managers, and some managers delivered far superior performance.

Does the manager provide diversification when it counts the most?

While most managers provided diversification on average, they differed in their ability to provide diversification during equity market downturns.

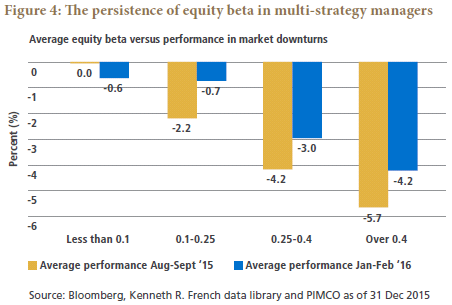

For example, although the last three years’ performance of multi-strategy managers didn’t reveal a strong relationship between returns and equity beta (i.e., managers with higher returns didn’t necessarily exhibit higher equity beta), there was a strong relationship during sharp market sell-offs. As shown in Figure 4, multi-strategy managers with high equity betas delivered the worst performance during August-September 2015 and January-February 2016. While this could be a result of poor timing decisions, the relationship seems to be quite persistent. In fact, we find there is almost a perfect correlation between average equity beta over the past three years and performance during down markets.

Do selected managers follow complementary approaches?

It is also important to consider whether selected managers follow complementary approaches.

Assessing whether managers are substitutes or complements requires a combination of qualitative and quantitative analysis. As an example, the responsiveness of signals1 used by managed futures managers can help in discerning whether they are good complements.

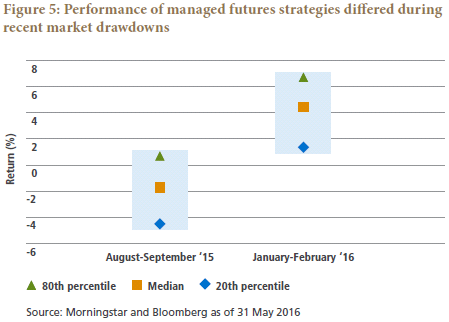

In both August-September 2015 and January-February 2016, the S&P 500 declined by over 10% before recovering in October and March, respectively. The sell-off path was different in each episode. In August-September 2015, the sell-off happened over just six trading days; the January-February 2016 sell-off transpired over 28 trading days.

Managed futures funds tended to do well in both these periods, but there was quite a bit of variation in performance across managers. A closer analysis shows much of this variation was driven by the level of responsiveness to market moves. In August 2015, managed futures funds that used short-term signals to go long or short the markets got “whipsawed” as they went short the market only to see it bounce right back, underperforming managers using longer-term signals. In contrast, these more responsive funds outperformed their slower-moving counterparts during the January-February 2016 market sell-off as the gradual nature of the market decline and subsequent recovery posed limited whipsaw risk (see Figure 5).

This illustrates a central point: Pairing managed futures managers with different levels of responsiveness would have provided a more consistent outcome across these two episodes.

Other considerations for manager selection

Although average equity beta in multi-strategy funds and responsiveness of managed futures strategies can help explain the direction of returns during recent market drawdowns, these factors still don’t fully explain the wide variation in returns across managers. As we’ve argued previously, manager selection is critical to investing in liquid alternative strategies, as broad investment guidelines and manager discretion can result in wide dispersion in returns across funds. However, even when selecting managers backed by an experienced team, sound process and deep resources, among other considerations, we still expect consistently high dispersion in manager performance to continue.

In managed futures funds, this dispersion reflects differences in algorithm, risk constraints and investment universe. Some strategies more rigidly target total volatility levels and contributions by asset class while others focus on the strongest trends, resulting in more variable levels of risk and more concentrated positions.

With multi-strategy funds, the overall fund structure, opportunity set and target level of risk and equity beta differ significantly across funds. For example, focusing allocations on multiple equity long/short and credit managers has the potential to generate meaningful equity risk, particularly during more volatile markets.

In sum, while overall objectives across managers may be similar within a category, the paths to those outcomes vary widely. Therefore, a closer evaluation of the considerations identified in this article can help investors identify managers with differentiated approaches. Overall, pairing a small number of these complementary managers may smooth the journey and increase the chance of realizing desired outcomes.