The Trade Facilitation and Trade Enforcement Act

In February, President Obama signed the Trade Facilitation and Trade Enforcement Act, a broad refresh of U.S. trade laws. Title VII of this law concerns exchange rate and economic policies. The earlier law, passed in 1988, required the Treasury Department to determine if a nation was “manipulating” its exchange rate. If a country was found to be doing so, the Treasury could engage in consultations to change the policies of the manipulator. In practice, the Treasury found few nations in violation of the earlier law. China was tagged with this designation five times from 1992 to 1995, Taiwan twice, in 1988 and 1992, and South Korea in 1988. In reality, being designated a manipulator didn’t trigger significant penalties.

In this report, we will discuss the history of exchange rate issues in trade, the new legislation and its potential impact on U.S. trading partners. We will review the reserve currency role and explain why this role almost precludes any effective trade policy designed to punish foreign trade practices. We will reflect on the new law in light of the current political situation in the U.S. and, as always, conclude with the impact on financial and commodity markets.

Currencies and Trade: A Background

The earlier law, passed in 1988, acknowledged that foreign nations could use exchange rates to enhance the value of their exports and effectively “steal” aggregate demand from the U.S. economy. It is important to note that the earlier law was enacted near the end of a major dollar market cycle that triggered two major currency agreements, the Plaza Accord in 1985 and the Louvre Accord in 1987.

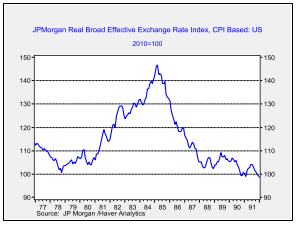

This chart shows the JP Morgan dollar index, which adjusts for trade flows and inflation. Note that the dollar rose by nearly 50% from 1978 to 1985. The combination of deregulation, loose fiscal policy and tight monetary policy made the dollar very attractive to foreign buyers as it led to falling inflation and very high real interest rates. However, the strong dollar undermined U.S. competitiveness, taking the current account from near-balance in 1981 to a 3.3% deficit (as a percentage of GDP) by 1987. In 1985, at the Plaza Hotel in New York, the G-5 (U.S., U.K., Germany, Japan and France) agreed that the dollar’s strength had become a danger to the global economic system and all agreed to push the dollar lower through direct intervention and “jawboning.” These measures, even in the absence of other policy changes, were effective in lowering the dollar. In 1987, the same group agreed to arrest the dollar’s decline by creating a set of “reference rates.” Although these trading bands were never enforced, they were effective in creating a period of relative exchange rate stability.

Up until the mid-1980s, most of the focus of trade negotiations was on tariffs and quotas. This was due, in part, to the fact that exchange rates were fixed until 1971, when President Nixon ended the Bretton Woods gold convertibility arrangement. After that, exchange rates began to fluctuate. With flexible exchange rates, nations noticed they could enhance their trade performance through a weak currency rather than restricting imports or subsidizing exports.

This chart shows U.S. net exports as a percentage of GDP. Note that trade was mostly balanced until the late 1970s but the U.S. has been in a deficit position since the early 1980s.

In general, domestic factors drive trade laws. Politicians are very sensitive to the labor markets as trade has an impact on labor markets even if they are near-balance because it forces workers to compete on a global scale. Trade deficits tend to exacerbate the problem. One reaction to trade concerns is to apply tariffs and quotas; however, U.S. leadership since WWII has steadily reduced these through various global trade agreements.1 Thus, nations looking to create an “edge” have been led to manipulate their currencies.

As we will discuss below, the provider of the reserve currency is virtually forced to run a trade deficit. However, the U.S. political class has never fully explained to the American people the burdens of hegemony. Consequently, instead of telling Americans who have lost their jobs to foreign competition that this is probably necessary because of the American superpower role, laws are passed to impose potential sanctions on currency manipulators that are essentially toothless. The 1988 bill lacked an automatic enforcement mechanism. The new bill lacks one as well.

The Trade Facilitation and Trade Enforcement Act of 2015

The section related to exchange rates is Title VII of the legislation. The 1988 law tended to view trading partners and manipulation so broadly that one only “knew it when they saw it.”2 In fact, the earlier law required the Treasury to divine “intentionality” in terms of why a country was manipulating its exchange rate. Simply put, a nation may be engaging in policies that manipulate its exchange rates (fixing the rate is, by definition, manipulation), but the intent of that policy may not be to boost a nation’s trade account. Even when the Treasury, who is in charge of foreign exchange policy, designated a nation as a “currency manipulator,” the executive branch had wide latitude on enforcement measures. Since trade retaliation is risky, there was no real enforcement of the law.

The new legislation does codify many issues surrounding trade and exchange rates. Here are several key components of the bill:

Ø The legislation formally defines “major trading partner.” First, it must have at least $55 bn of annual trade with the U.S. Second, it must run a bilateral trade surplus with the U.S. of $20 bn or more. Third, its overall current account surplus must be greater than 3% of that nation’s GDP.

Ø The legislation also requires the Treasury to monitor whether a nation is “engaged in persistent one-sided intervention in the foreign exchange markets.”

Ø If a nation meets the above criteria, then “the President…shall commence enhanced bilateral engagement.” The president can, after years of enhanced engagement, deploy a series of remedies. These include prohibiting the Overseas Private Investment Corporation from approving financing of projects,3 prohibiting government contractors from buying imports from a violating nation, calling on the IMF to also monitor the offending nation and considering adjustments to any bilateral or regional trade agreements.

Ø The law does allow the president to waive any penalties if such actions “…would have an adverse impact on the U.S. economy greater than the benefits of the action” or “…would cause serious harm to the national security of the U.S.”

Some members of Congress wanted to treat currency manipulation as a “countervailable subsidy,” which would allow the government to apply import duties to offset the estimated level of the “subsidy.” There were three problems with this alternative. First, it would be very difficult to actually measure the level of the subsidy and, given the tendency of exchange rates to adjust, conditions may have changed by the time the subsidy was established. Second, it isn’t clear if the WTO would have accepted this policy. Third, such actions would undermine the reserve currency role. After all, accumulating the reserve currency is normal behavior. The U.S. can’t really penalize a nation for doing so unless some other reserve currency is an acceptable substitute. The primary way foreign nations acquire dollars is by running a trade surplus with the United States.

The Reserve Currency Role

The reserve currency is really a global public good. Economists define a public good as a product or service that must be provided by governments because the private market either won’t provide the good or provides the good in less than optimal amounts. There are seven public goods a reserve currency nation should provide:

1. Act as a consumer (importer) of last resort;

2. Coordinate global macroeconomic policies;

3. Support a stable system of exchange rates;

4. Act as lender of last resort;

5. Provide counter-cyclical long-term lending;

6. Provide a truly riskless AAA asset for benchmarking purposes; and

7. Supply deep and predictable financial markets.

Charles Kindleberger, an economist who studied asset bubbles, provided the first five of the aforementioned public goods, and Mohamad El-Erian, the former co-CEO of PIMCO, provided the last two.

Because the reserve currency provides global liquidity, the reserve currency country must run a persistent current account (trade) deficit. If this nation ran a surplus, it would act as global monetary policy tightening. However, this deficit would need to be “manageable.” If it became too large, it could weaken foreign investors’ confidence in that risk-free asset.

Note the above chart on net exports. Initially, after World War II, the U.S. ran a large trade surplus. However, this surplus rapidly contracted as the U.S. carried out its role as importer of last resort. Although the trade balance tended to be positive for most of the 1960s, the U.S. was running persistent deficits with Europe, the first region to recover after the war. In the 1970s, trade deficits became more common after President Nixon closed the gold window.

However, from the 1980s forward, deficits became larger and more persistent. It has become apparent that the best way for an emerging nation to achieve developed status is through export promotion. This method includes constraining domestic consumption, boosting saving, creating a large industrial base and using the reserve currency nation to absorb the excess production. European nations, especially Germany, started with this program. Japan and other nations in Asia followed the same path. Over time, the U.S. has been required to take on larger levels of debt in order to supply the world with enough dollars to maintain global liquidity.

The reserve currency role has both benefits and costs. On the benefits side, the U.S. can run large sovereign deficits with less impact on the economy because there are foreign buyers of Treasuries. Because foreign nations have an incentive to run a trade surplus with the U.S. to acquire dollars, low-cost imports keep inflation under control. The downside is that U.S. firms face constant foreign competition, which is, almost by design, unfair. As long as there is a global consumer of last resort, other nations have an incentive to implement export-promoting policies.

The reserve currency role is a key part of global hegemony. Using the dollar as a reserve currency extends U.S. power and influence. It allows the U.S. to enforce sanctions by denying foreign banks access to the U.S. financial system and makes foreign nations dependent on the U.S. economy. However, it does carry costs to the American economy. It causes unemployment to rise in some industries and increases worker insecurity.

For these reasons, the government passes laws, such as the aforementioned Trade Facilitation and Trade Enforcement Act, which seem to signal a new willingness to offset the problems caused by the rising trade deficit. However, unless the U.S. is willing to end its superpower role and relinquish the reserve currency, the trade deficit will always be with us. Since most lawmakers should be cognizant of this fact, trade laws are more about giving the impression of addressing the trade deficit rather than actually ending it.

Ramifications

Overall, we would not expect this new law to actually lead to changes in U.S. trade policy. Although the legislation does a service in that it defines nations that have a major impact on the U.S. economy, without automatic penalties, we suspect that there will always be a reason not to implement trade restrictions. There is also one other major flaw with the legislation. By focusing on bilateral trade deficits, it ignores multilateral trade behavior that can be just as damaging to the U.S. trade sector. For example, some nations are part of a global supply chain that export partially made goods to the final exporter. The latter nation may be running a trade surplus with the U.S. but the partial assembler may actually have the manipulated currency.

At the same time, it does give the White House parameters to open conversations with our largest trading partners. At present, no nations fit all the criteria to trigger “enhanced engagement.” However, five nations meet two of the three conditions and have been placed on a monitoring list. These are China, Germany, Japan, Taiwan and South Korea. Monitoring these nations makes sense; they are important to the world economy and the U.S. has an incentive to steer their economic policies. At the same time, the U.S. has little reason to engage in a trade or currency war with any of these nations, and so we expect this new rule to lead to consultations but no change in trade policy.

The Plaza and Louvre Accords show that the U.S. can reduce the drag on trade by forcing misaligned currencies into fairer levels. At the same time, it is also important to note that this currency pact was arranged with just a few nations. The G-20 is probably too large a group to implement currency arrangements. If this new law creates a more workable group, maybe a “G-4,” it would be a positive development. However, in a political environment that has clearly turned against trade, it is important to realize that this law is little more than window-dressing. Nothing within it will bring about a trade surplus. As long as the U.S. provides the reserve currency and remains the global superpower, no renegotiation of trade deals will lead to a trade surplus. Thus, the overall market impact of this new law is minimal, but its political impact might be important in that it may act to ease some of the current political unrest tied to trade.

Bill O’Grady

June 13, 2016

This report was prepared by Bill O’Grady of Confluence Investment Management LLC and reflects the current opinion of the author. It is based upon sources and data believed to be accurate and reliable. Opinions and forward looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

Confluence Investment Management LLC

|

1 The most recent of these is the World Trade Organization (WTO).

2 Famously quoted by SCOTUS Justice Potter Stewart in reference to pornography.

3 OPIC is a government-sponsored corporation and uses private capital to support economic development projects.

© Confluence Investment Management