The year was 1964 when Reprise Records released the song “Baby Don’t Go.” Written by Sonny Bono, and recorded by Sonny & Cher (Cherilyn “Cher” Sarkisian), the song became a smash hit and set the duo’s career in motion. The repeating lyric in said song is “Baby don’t go, pretty baby please don’t go.” And that’s the song playing in the various streets of the European Union (EU) as the Brits contemplate leaving the coalition on June 23 (Brexit). The latest odds I saw were those of last Friday where Predata showed 46.04% of respondents wanted to stay “in,” while 59.96 wanted “out.” The media is spinning Brexit such that an exit might cause a domino effect with other EU members following the Brits, potentially setting the stage for a complete dissolution of the EU. I think the odds of that happening are remote, but the politics of a U.K. exit could be impactful. And as long as we are skirting the realm of politics, I found this story, written by my friend Arthur Cashin, to be intriguing and pretty funny. As Arthur writes:

After the close Monday, there was the customary meeting of the Friends of Fermentation. It was far from a plenary session with only a handful of members attending. Perhaps it was the marinating ice cubes, or just the small crowd, but something prompted one of the members to weave a rather illogical but intriguing (at least to me) political fantasy. Say you are a Reality TV celebrity and you decide to throw your hat into one of the presidential races of one of the major parties. To you it's a bit of a lark, primarily a vehicle to enhance your celebrity credentials around the country. In the beginning everything goes well. You claim that the powers that be are conspiring against you and trying to rig the election. Much to your amazement, the other candidates fall by the wayside and you become the presumed nominee. In some ways this is a problem; if you run and lose, the loss may diminish your brand. Worse yet, now that you stand alone, reporters are pestering you with very specific questions on world events, and if you are not fully up to date, they begin to portray you as someone who is less than knowledgeable. That will never do. To lose could be damaging enough to your reputation, but to lose and appear not to be on top of things could wound your image, or even destroy it. In my friend's fantasy, the candidate decides that the only way out is to do many outrageous things before the convention, forcing the party leaders to block the candidate and name a substitute. That allows the candidate to claim he or she was robbed and retain their newly enhanced image. It was an entertaining story but then the peanuts ran out. Guess we're stuck with our current logical election.

While termed a political fantasy, this essay certainly would explain some of the antics being unleased by Mr. Trump. And now you understand why every chance I get I meet with my counterparts of the Friends of Fermentation. Last week, however, I met with folks in Chicago. I would like to thank all of the people at BMO, Putnam, First Trust, Nuveen, and Harris for the ideas we shared, yet the highlight of the week was having dinner with my friend Kurt Funderburg, portfolio manager for First American Bank. Kurt and I worked together in a past life when he was my Healthcare analyst. Over dinner, we talked of old times and swapped investment ideas. One of his favorite names is Dollar General (DG/$91.44/Strong Buy), which is followed by Raymond James’ fundamental analysts with a Strong Buy rating. For more on the DG story, please see our analyst’s reports.

Another portfolio manager (PM) I spoke with was CEO, CIO, and PM of Perritt Capital, namely Michael Corbett. I have met with Mike before and have found him to be a good captain of capital. Two of the funds Mike manages are the Perritt MicroCap Opportunities Fund (PRCGX/$31.90) and the Perritt Ultra MicroCap Fund (PREOX/$14.57). For the record, microcaps have underperformed for the past few years. That underperformance is likely because they did so well in 2013 that valuations got stretched. To be sure, at last February’s low, the Russell MicroCap Index was down some 27%+ from its June 2015 high. Nevertheless, while the micro capitalization universe of stocks has been out of favor, I think it’s time has come. Like Wayne Gretzky states, “I skate to where the puck is going to be;” and I believe “the puck,” at least for some of your capital, should be micro caps going forward. Over the years, many investors have asked me, “If you were going to manage money again, how would you do it?” My response has been, “I would concentrate on micro caps where there is no or little research coverage because that is where the misvalued pieces of paper are.

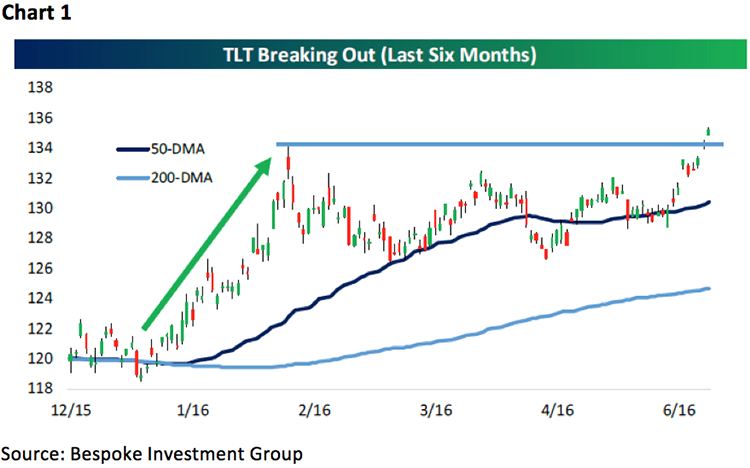

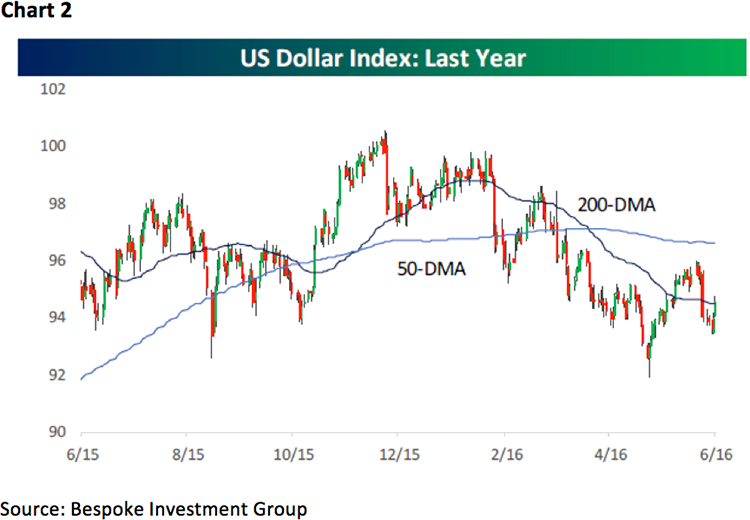

So what else did we see and/or learn in our travels last week? Well, I heard a lot of interesting investment ideas from the PMs I met with. One PM pointed out that the iShares 20+ Year Treasury Bond ETF (TLT/$134.78) is breaking out to the upside in the charts (read: lower interest rates/see Chart 1). Another complimented Andrew and me on our call for the past 10 months, that the Dollar Index (DXY/$94.66) topped last year (Chart 2), was correct and suggested select sectors that should benefit from a weaker greenback (Chart 3). Still another PM wanted to know more about the current “buying stampede,” which at session 84 is clearly the longest I have ever seen. To that point, the invaluable Bespoke organization recently wrote:

It’s been nearly four months since the S&P 500’s 2016 low on 2/11, and while it may seem like the market has just gone up every day since then, we were somewhat surprised to see that the frequency of up days over the last four months has been far from extreme relative to the rest of the bull market that began in 2009. The chart (Chart 4) shows the percentage of positive days for the S&P 500 over a rolling four-month period going back to March 2009. As of Wednesday’s close, the S&P 500 has been up in 48 of the prior 84 trading days, which works out to an average of 57.1% of all trading days. In order to compare the current reading to prior readings, whenever the line in the lower chart is red, it indicates that the percentage of up days over the prior four months was greater than the current reading, while the blue line indicates a lower reading. As shown in the chart, there is a lot of red. In fact, the S&P 500 has had a higher percentage of up days over a trailing four-month period on 38% of all trading days since the bull market began. In the top chart of the S&P 500, the red lines mean the same thing as the bottom chart. As shown, in the majority of instances, these periods of consistent up days tended to occur in bunches. Heading into this week, there was no denying that the market was overbought in the short term, and while a period of consolidation or modest declines is possible, the consistency of buying over the last four months has been far from extreme, so it’s not as though investors have been blindly buying.

And now, in addition to Friends of Fermentation, you know why I think serious investors should have access to Bespoke.

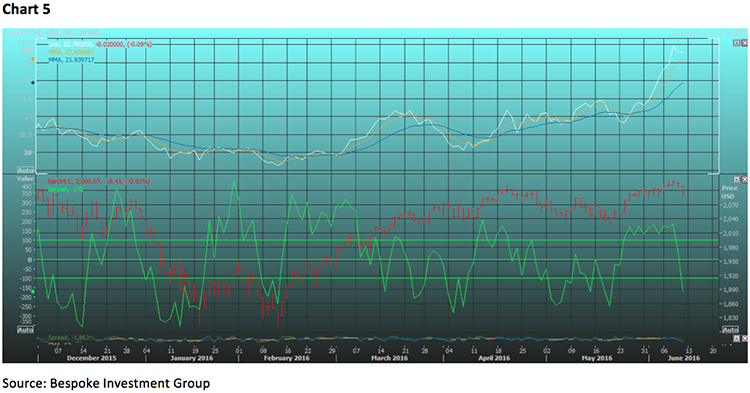

The call for this week: In last Thursday’s Morning Tack, I wrote, “Certainly this rally is extended, yet we still don’t see evidence of any ‘sell signals’ or much bearish data. In fact, one of the few cautionary ‘flags’ comes from the McClellan Oscillator, which is overbought on a short-term basis.” So while the past two trading sessions have been painful, it has indeed corrected the overbought condition (Chart 5) I spoke of and still leaves the S&P 500 (SPX/2096.07) above its 50 and 200-day moving averages. Also of note is that crude oil broke below its rising trendline last week and that we expect a decent rally attempt after the Brexit vote. This week, investors’ attention will focus on the FOMC meeting, where we have been saying for months there will be NO rate ratchet and likely no rate increase until after the November election. Many of these machinations will be discussed in this Wednesday’s 4:15 p.m. webinar with myself, Andrew Adams, and some of Putnam’s best and brightest. As I write this on Sunday night in Charleston, SC, the S&P futures are off eight points on Brexit fears, China’s slowing fixed investment flows (15-year low), this week’s FOMC meeting, the Bank of Japan meeting, and Friday option expiration. A close by the SPX below 2078.40 would trigger a short-term trader’s “sell signal” on the daily MACD indicator.