“Market bubbles occur when the price of an asset significantly deviates from its intrinsic value. There have been numerous bubbles predicted in my 20 years as a professional investor. Fortunately, only two, from the perspective of U.S. investors, came to pass. The technology bubble in 2000 and the financial crisis in 2008.”

. . . Scott Kubie, Chief Strategist at CLS Investments

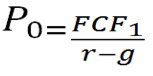

As many of you know, last week I traveled throughout Mississippi and Alabama presenting to our financial advisors and their clients. My message was upbeat, yet many of those investors think the equity markets are in a “bubble.” Why this “bubbleicious” sentiment is so pervasive is a mystery to me, because using S&P’s earnings estimates for this year and next (~$114 and ~$134) leaves the S&P 500 (SPX/2052.32) trading at 18x this year’s estimate and 15.3x next year’s. As written last week, “In 2000, the S&P Total Return Index was trading for more than 30x earnings (excluding negative earnings), and if one includes negative earnings, the P/E ratio was pushing 60x.” As I was attempting to explain such metrics to one of our clients last week, an email from a European account arrived. The prose was from Scott Kubie, sagacious strategist who hangs his hat at the insightful CLS Investments organization, and the first thing I saw was the equation that serves as the title for this report.

The author explains said equation by noting: 1) FCF is free cash flow one year in the future, 2) R is the required rate of return, and 3) G is the future growth rate. Scott Kubie then elaborates:

“Whether you totally grasp the equation or not, the key points are: higher cash flow and growth raise the value of the firm, and a higher required rate of return lowers the value. The last two U.S. market bubbles occurred because investors were fooled by inflated values in one of these numbers. Interestingly, the 2000 and 2008 bubbles occurred in different parts of the equation. In 2000, investors assumed Internet companies would take over every aspect of commerce. Small startups were projected to grow into behemoths down the road. The growth rates assumed far outpaced potential, and a bubble ensued. High price-earnings (P/E) ratios for technology stocks were an expression of high growth expectations. As growth (g) gets closer to the required rate of return (r), valuations can get very high. 2008 resulted from inflated cash flow. In this period, investors assumed the high profits and cash flow generated from housing loans were sustainable. Instead, those numbers were based on errant assumptions about the housing market. Those profits were restated as massive losses in the following years. In this case, the valuations looked legitimate the entire time; it was the profit numbers that were inflated. So, where should we look for the next bubble? Investors and generals are known for fighting the last war. People looking for financial decline due to increasing student loan debt or riskier car loans are looking in the wrong places. Even the optimism in Internet firms or biotech companies pales in comparison to 2000’s tech bubble. Instead, look to the variable in the equation that hasn’t caused a recent bubble. Required rates of return (r) may be too low for some assets.”

I agree with this analysis and would urge investors not to get too bearish despite the difficult stock market environment. To be sure, the past nearly two years has been one of the most challenging markets I have ever seen. As the good folks at Bespoke write, “Markets have basically gone nowhere for the last 24 months. With fixed income yields as low as they are and equity markets basically returning nothing, investors have had a very tough time generating any kind of returns since mid-2014. Sideways action is a lot better than down action, but another leg higher at some point would sure be nice.”

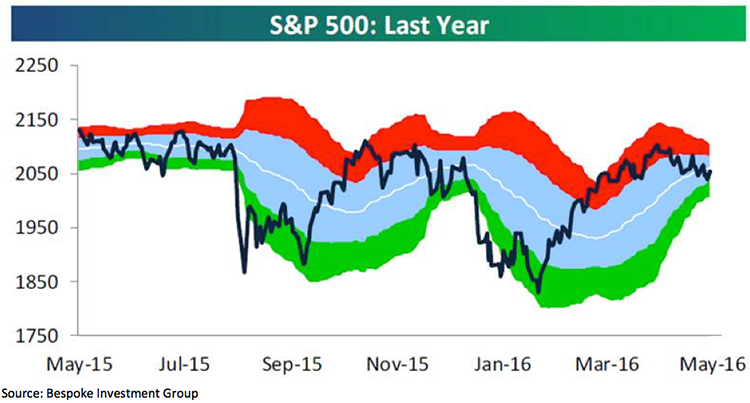

And that’s true; the SPX has been range-bound (~1800-2130) since October 15, 2014. During that timeframe, Andrew Adams and I have made a number of tactical trading “calls,” most of which have produced decent results. Speaking to the “bad calls” we have made, as often stated, “When you are wrong, be wrong quickly and for a de minimis loss of capital.” We had to admit to a “bad call” back in mid-April when the SPX failed to follow its brethren, the S&P Total Return Index, to new all-time highs. That action produced a “polarity flip” in our model, suggesting a move to the downside into the week of May 8 (∓3 sessions) with a downside price target of 1990-2000. So far, the timing model has been generally correct but precisely wrong given the “low print” of last week at 2025.91. Of course, that is inconsistent with our price target, yet in this business, you have to take what the markets give you. However, the past few weeks have produced another oversold condition with the SPX becoming as oversold as it was last February (chart 1). That’s interesting, because the SPX is only off ~2.4% from its mid-April closing high. At the February oversold reading, the SPX was down some 13.3% from its November reaction high.

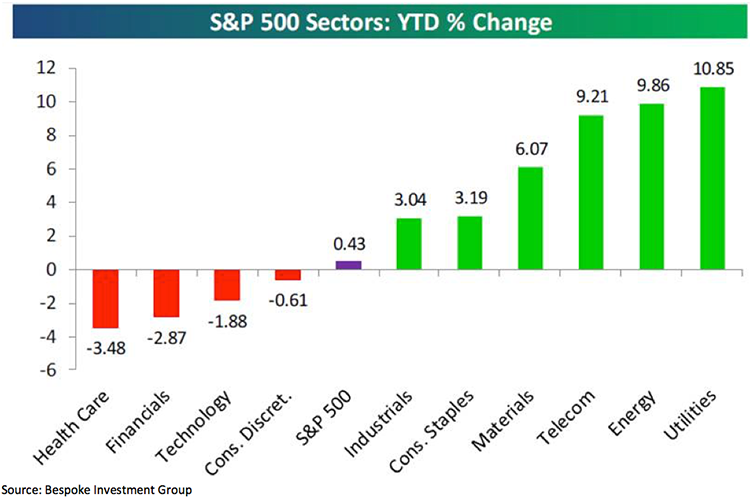

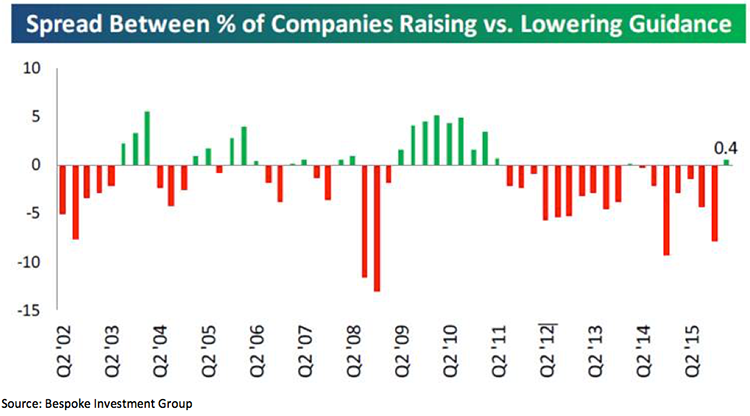

Given this year’s non-linear (trendless) performance, it is thought provoking to look at the sector performance year-to-date (chart 2). Utilities have been the clear winner with a YTD gain of 10.85% followed by Energy (+9.86%) and Telecom (+9.21%). That sector performance is a head scratcher, because Utilities, Energy, and Telecom have not had the best earnings momentum. Maybe the equity markets are looking forward to and anticipating better earnings. That certainly is what is occurring with forward earnings guidance, which is back in the “green” for the first time since early 2014 (chart 3). This is not an unimportant point, because the performance of companies the beat their earnings estimate, beat revenue estimates, and raised forward earnings guidance has been pretty good. Some such names from Raymond James’ research universe, which have favorable ratings from our fundamental analysts and screen well using my proprietary algorithm, include: C.R. Bard (BCR/$219.74/Outperform), NVIDA (NVDA/$44.33/Strong Buy), Newell Brands (NWL/$47.14/Outperform), UnitedHealth (UNH/$130.94/Strong Buy), and Wal-Mart (WMT/$69.86/Strong Buy).

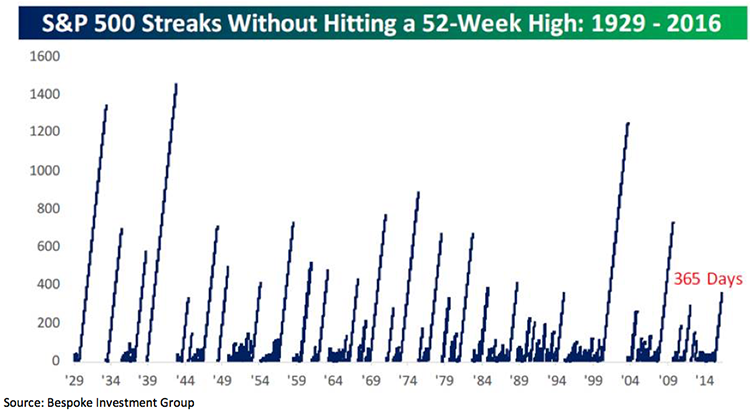

The call for this week: According to the perspicacious Jason Goepfert (SentimenTrader), “It has now been a year since the S&P 500 was at an all-time high. This is one of the longest streaks without seeing a new high, with one of the smallest losses during the streak. Other times the S&P went this long without a new high led to highly variable returns, but they were better when the maximum loss had been under 20% as it has been so far (chart 4).”

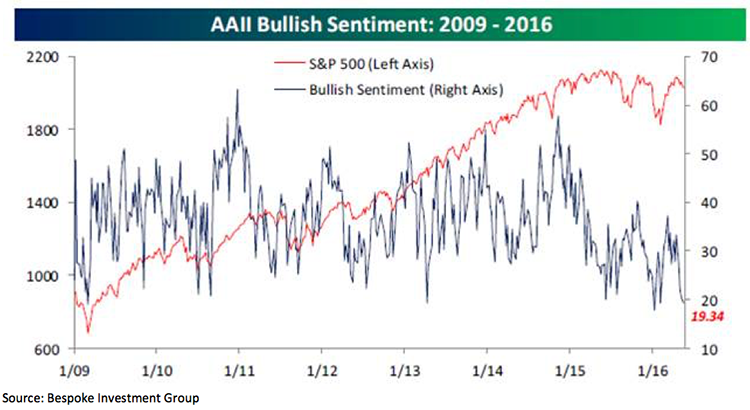

Of course, such action has left AAII Bullish Sentiment plumbing the lows (chart 5). Indeed, all the ingredients are here for a bottom. This morning, the preopening futures are down a frack as the Nikkei shed 1.63% overnight on some ugly trade data. I do find it interesting that the SPX is testing its April lows, but the Advance/Decline Line continues to trade higher. We continue to exercise the rarest commodity on Wall Street, patience…