The Geopolitics of Helicopter Money: Part 2

Last week, we described in some detail the process of “monetary funded fiscal spending” (MFFS). Part 1 of this series included a discussion of why MFFS might be implemented, how it would work and the potential problems that come with using it. In this week’s report, we will examine two historical examples where forms of MFFS were implemented, Japan in the 1930s and the U.S. during WWII. Next week, we will conclude the final report of the series with market ramifications.

Japan in the 1930s

Japan’s industrialization began with the Meiji Restoration which started in the late 1860s. The country became a rapidly advancing power in the region, defeating China in the First Sino-Japanese War (1894-95) and Russia in the Russo-Japanese War (1904-05). The former gave control of the Korean Peninsula to Japan and the latter announced Japan’s entry as a major world power.1

Japan continued to expand its influence in the Far East. It was aligned with the Allied Powers during WWI and played an important role in protecting sea lanes from German attempts to disrupt shipping. It also expanded its influence in China, a point of contention with the U.S. The post-WWI period initially began with strong economic growth but a series of supply and demand shocks rocked Japan’s economy in the 1920s. Important events included the Great Kantō Earthquake in 19232 and a financial crisis in 1927, which was caused by expectations of a return to the gold standard. Japan’s decline was capped off by the onset of the Great Depression, which coincided with fiscal austerity and another attempt to return to the gold standard.

In the face of a dramatic downturn, Takahashi Korekiyo became finance minister. He immediately ended the previous government’s austerity program with a series of measures, including taking Japan off the gold standard, which led to a rapid depreciation of the yen, and increasing fiscal spending, which rose by 58% from 1931 to 1933. This spending lifted government spending from 10.7% of GDP in 1931 to 14.7% in 1933. In 1931, the government balance was a small surplus (0.1% of GDP); it became a deficit of 6.1% of GDP by 1933. However, one of the most controversial measures Takahashi implemented was to engage in MFFS by prevailing upon the Bank of Japan (BOJ) to purchase the bonds created by the deficit, effectively monetizing the debt.

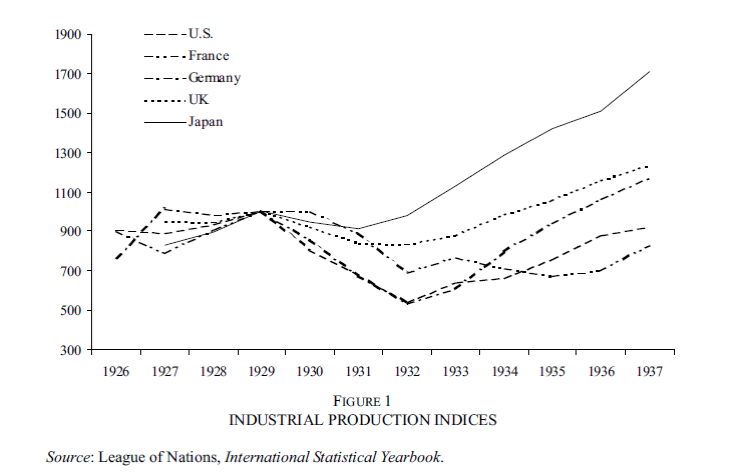

These measures were quite effective, allowing Japan to recover much faster than other industrialized nations.

This chart shows industrial production for various nations indexed to 1929. Note that Japan recovered the quickest.

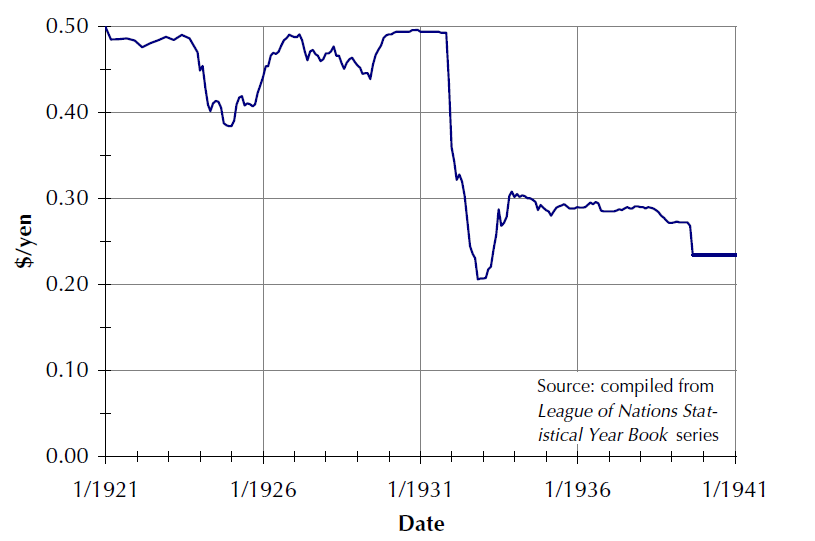

The fiscal measures and MFFS led to a sharp depreciation in the yen. The yen depreciated from 50 cents to 20 cents, a 60% decline. That would be roughly equivalent to the yen falling to 175 ¥/$ in today’s market.

As the global economy and global trade began to recover after Roosevelt took the dollar off the gold standard, Japan was able to benefit from this currency weakness.

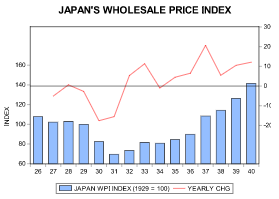

Interestingly enough, price levels did not rise sharply until after Takahashi’s assassination in 1936.3 Although the data isn’t available, we suspect this was due to ample excess capacity in the Japanese economy and the increased demand from government spending was absorbed without significant increases in inflation. It should be noted that Japan also implemented a series of capital controls that probably prevented a larger selloff in the yen and helped keep prices under control.

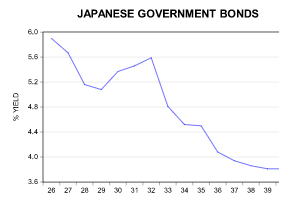

Due to the BOJ’s continued engagement in MFFS, government bond yields remained low even as inflation began to rise after 1936.

Takahashi is credited with using unorthodox economic policies to lift Japan out of the Great Depression. Although he may be most remembered for MFFS, the other policies also played a role, which included leaving the gold standard, increasing infrastructure and defense spending, and allowing for currency depreciation. After his assassination, Japan’s defense spending soared, which led to rapidly rising inflation; BOJ debt monetization prevented interest rates from rising which is a form of financial repression.

The U.S. during WWII

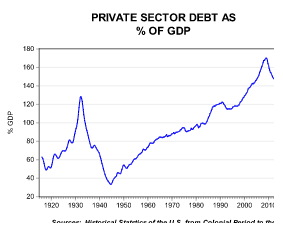

Scholars continue to discuss the causes of the Great Depression. Like any major event, there are multiple reasons for its occurrence, ranging from being between global hegemons4 to income disparities5 to disastrous policy decisions.6 Although I believe that all three, and others, were contributing factors, the one that doesn’t get much attention is the role of private sector debt.

This chart shows the level of household debt along with non-financial corporate debt as a share of GDP.7

In the 1920s, private sector debt rose sharply, with business borrowing accounting for 84% of private sector debt by the early 1930s. The Great Depression was exacerbated by severe deleveraging.

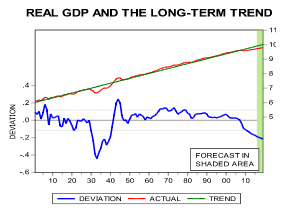

Although the U.S. economy was recovering from the worst of the Great Depression by the late 1930s, growth was still below trend.

This chart shows the inflation-adjusted level of GDP on a logarithmic scale, regressed against a time trend. The lower line on the chart shows the deviation from trend. Note the huge drop in GDP during the Great Depression and the “hitch” in the recovery that represents the 1936-37 recession, which occurred after the Roosevelt administration tried to normalize fiscal policy by balancing the budget. Even by 1940, GDP was well below trend and didn’t rise above trend until 1942.

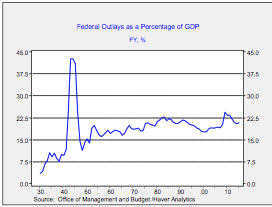

World War II represented a massive expansion of fiscal spending.

Government spending as a percentage of GDP peaked at 42.7% in 1944. The war-related fiscal spending pushed GDP well above trend. In addition, government spending along with other policies effectively led to a private sector/public sector debt swap.

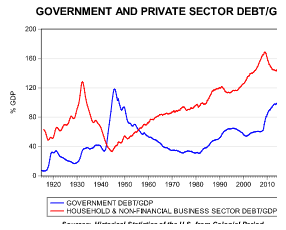

Government spending and borrowing allowed the private sector to complete its deleveraging. Military spending supported businesses by providing orders for equipment and supported households by creating jobs in the defense industry. At the same time, household spending was restrained by rationing. The non-financial private sector used the increase in government spending to complete the deleveraging process. At the same time, government debt soared to 120% of GDP.

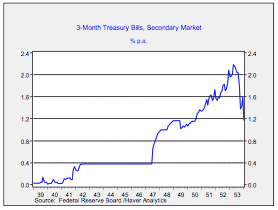

The Federal Reserve’s official stance during the war was “…to use its powers to assure at all times an ample supply of funds for financing the war effort.” Although taxes were raised to fund the war effort,8 the level of government debt clearly rose, indicating that deficits increased significantly. The Federal Reserve pegged interest rates at 3/8% for T-bills. This peg became effective in July 1942 and remained in place until June 1947.

The Federal Reserve Act was amended to allow the central bank to purchase government securities directly from the Treasury, fostering MFFS.9 In addition, Executive Order 9112 allowed the Reserve Banks to directly guarantee loans to industries engaged in war production.

The combined effect of these measures appears to be a form of MFFS. By the end of the war, private sector debt fell to historic lows, at 33% of GDP. This low level of debt allowed the private sector to borrow after the war’s end. The pent-up demand for goods and services, coupled with financial repression, allowed for private sector debt to rise to more normal levels and also allowed government debt to decline below 40% of GDP by the 1970s.

Bill O’Grady

May 9, 2016

1 In the Russo-Japanese conflict, Japan effectively destroyed Russia’s Pacific Fleet. Tsar Nicholas ordered the Baltic Fleet to make the epic journey from Russia to Japan, initially to relieve the Pacific Fleet and then to respond to its destruction. The Baltic Fleet was forced to use the route around the Cape of Good Hope because it mistakenly fired on British fishing vessels and the British denied the Baltic Fleet access to the Suez Canal (it should be noted that the British and Japanese were sharing intelligence as the British saw Russia as a threat). This long trip degraded the fighting capacity of the Russian fleet. Finally, after reaching Japan, the Baltic Fleet was virtually destroyed by the Japanese navy. This impressive success signaled Japan’s entry on the world stage and came as a shock to Western powers.

2 This earthquake, which registered 7.9 on the Richter scale, led to 105,385 confirmed deaths.

3 Takahashi was trying to thwart growing militarism by restricting military spending. He was planning on ending the BOJ’s participation in MFFS. Rebelling military officers assassinated Takahashi in February 1936.

4 Charles Kindleberger’s primary reason.

5 J.K. Galbraith’s contention.

6 Milton Friedman’s favorite.

7 Financial sector debt is excluded in this calculation because it may lead to double counting; if the financial system generates debt to provide a loan to a household or a corporation, the collateral for the financial system debt is probably coming from the loan to the household or the corporation. Thus, the usual practice is to exclude financial sector debt from the calculations of indebtedness.

8 http://www.federalreservehistory.org/Events/Deta ilView/75

9 Ibid.

This report was prepared by Bill O’Grady of Confluence Investment Management LLC and reflects the current opinion of the author. It is based upon sources and data believed to be accurate and reliable. Opinions and forward looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

© Confluence Investment Management LLC

© Confluence Investment Management