Last Thursday was session 53 in the “buying stampede” and it was going along swimmingly. Well, I guess the surprise “no stimulus” announcement out of Japan caused an early morning stutter-step, but the equity markets seemed to stabilize after a somewhat weak opening. In fact it caused one market wizard to comment, “I love this market. Bad earnings can't take it down. Remember, the move most people least expect is the DJIA going right through all of that overhead supply and making all-time new highs. I'm in the minority camp, expecting major new highs. Buy in May and don't go away!”

And that was pretty much my feeling as well, since I too was expecting the S&P 500 (SPX/2065.30) to notch a new all-time high. However, last Thursday, when Carl Icahn appeared on CNBC, he said he no longer owned Apple and stocks “stopped!” Further, when he stated that unless there is more economic stimulus, a day of reckoning is coming, and then stocks swooned. The result left the SPX lower on the week by 1.26% and resting on its 40-day moving average (DMA). In past missives I have suggested there were two scenarios going into the month of May. My preferred scenario was for the S&P 500 to make new all-time highs, which would have used up its remaining internal energy, leaving the SPX susceptible to a pullback. The alternate scenario was for an immediate pullback into mid-May, which should actually set the stage for higher prices over the next few months. Yet Icahn’s CNBC comments seemed to derail my preferred path for stocks. Still, the Thursday/Friday downside two-step leaves the near-term directionality of the equity markets inconclusive (IMO). We should get a better read on direction this week.

Adding to last week’s downside drama was the government’s report on real GDP, which rose at an annualized rate of just 0.5%. In said report, consumer spending slowed (+1.9%), business fixed investment fell (-5.9%), University of Michigan Sentiment Index was lower (89.0 vs 91.0 in April), new home sales fell (-1.5%), the Fed dropped the phrase “global economic and financial developments continue to pose risks,” and maybe that was dropped because the flash GDP estimate for the Eurozone was better than expected (+0.6%). That caused me to re-read this quip from the managing director of the IMF, Christine Lagarde:

The good news is that the recovery continues; we have growth; we are not in a crisis. The not-so-good news is that the recovery remains too slow, too fragile, and risks to its durability are increasing. Certainly, we have made much progress since the great financial crisis. But because growth has been too low for too long, too many people are simply not feeling it. This persistent low growth can be self-reinforcing through negative effects on potential output that can be hard to reverse. The risk of becoming trapped in what I have called a “new mediocre” has increased.

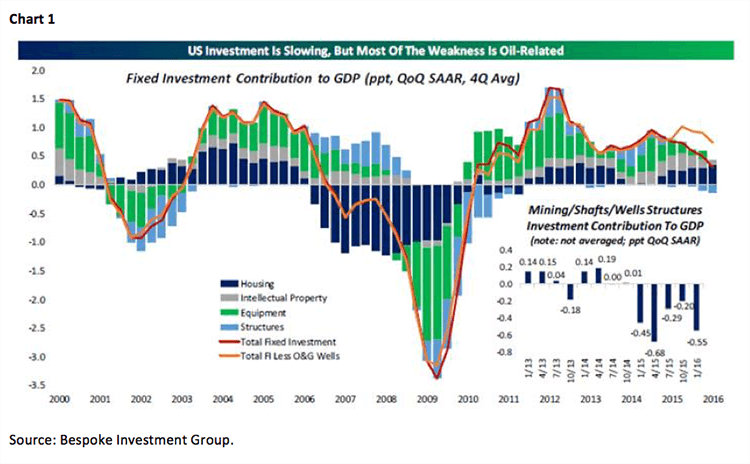

Read that paragraph again. She just as easily could have been talking about the U.S.! This week we will get a slew more of economic reports with eyes focused most closely on the ISMs, Durable Goods, non-farm productivity, and the all-important Employment Situation Report for April. I continue to believe last week’s economic reports will mark the low water point for the economy and look for things to strengthen going forward (chart 1).

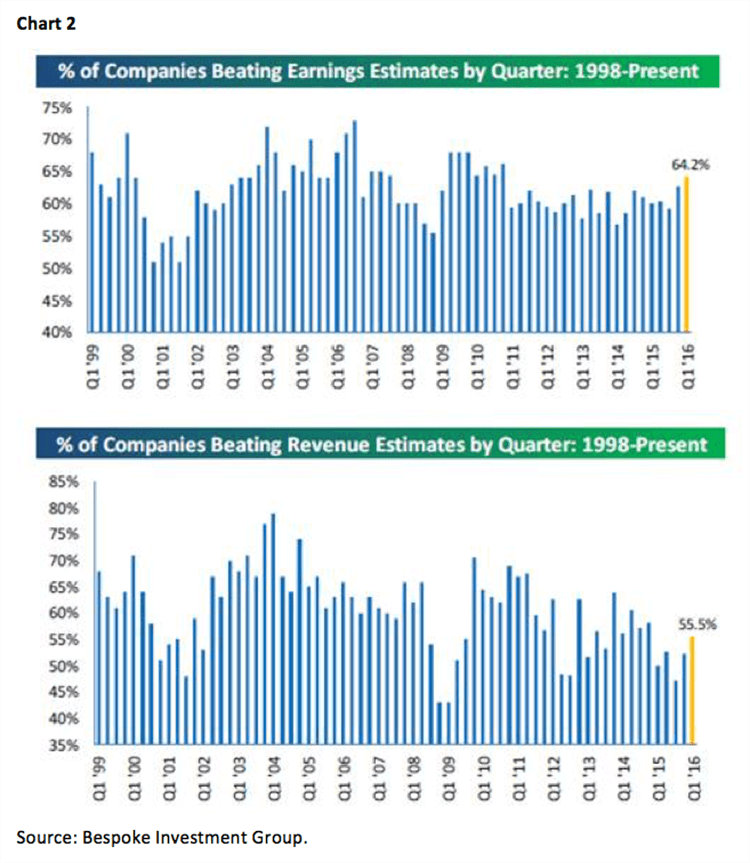

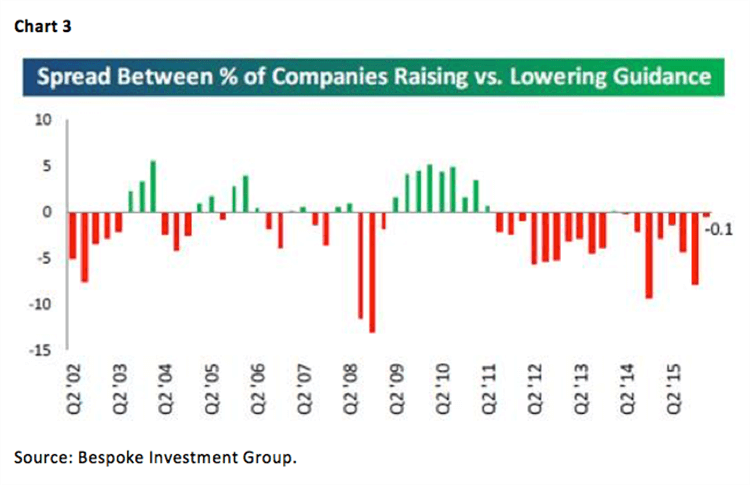

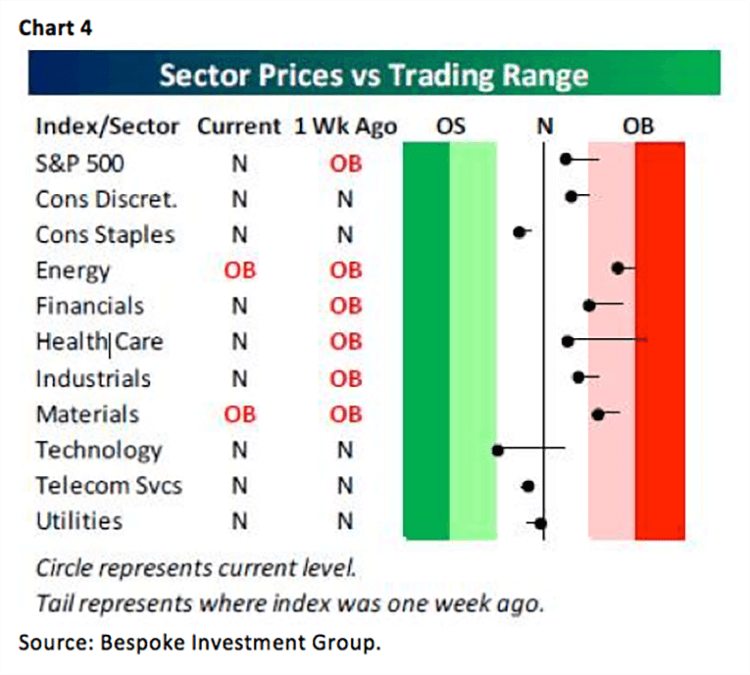

Speaking to earnings, the EPS season is now half over with roughly 1,100 companies reporting. As expected, at least by us, the percentage of companies beating estimates stands at 64.2%. That’s the strongest “beat rate” since mid-2010. While at 55.5%, revenues are not as strong as the earnings “beat rate,” hereto they are the strongest we have had over the trailing 12 months (chart 2). Even the forward earnings guidance is strong. As my friends at the must-have Bespoke organization write, “The forward expectations coming out of corporate America this earnings season are definitely stronger than what the narrative is in the financial media” (chart 3). Of the 10 S&P macro sectors (on September 1st there will be an 11th macro sector as REITs debut), the strongest “beat rate” comes from (in order of strength): Consumer Staples, Materials, Healthcare, and Consumer Discretionary. The weakest “beat rate” sectors are: Telecom, Utilities, and Energy. And as long as we are on the subject of sectors, after a ~16.6% rally by the SPX from its February 11, 2016 intraday low (we were bullish) into the intraday high on April 20, 2016, and the subsequent 2.8% pullback, the only sector that is even remotely oversold is Technology (chart 4). That’s very interesting since Technology is trading at a price to estimated growth (PEG) ratio of 1.27x, while Utilities trade at a PEG ratio of 3.34x. If you think Utilities are going to grow 2.5x faster than Technology, I have a few yards of swampland here in Florida I would like to sell you! As for this season’s earnings reports, ISI’s eagle-eyed Ed Hyman writes, “The biggest development last week was the dollar's 2% decline, which helped push up commodity prices including gold, oil, corn, and lumber. The yen's surge was very disturbing. But the combination of a lower dollar and higher commodity prices has significantly improved the outlook for S&P earnings. Earnings probably bottomed in 1Q.”

Obviously we agree, and regarding the earnings theme, we often talk about companies that have beaten their earnings estimates, beaten revenue estimates, raised forward earnings guidance, and are favorably rated by our fundamental analysts. Screening the companies that have done this so far, and using our proprietary algorithm trading system, shows six companies that qualify. We offer them to you for consideration on your potential “buy list” if the SPX does indeed pull back into mid-May. They are, in no particular order: Abbott Labs (ABT/$38.90/Outperform), Advance Micro (AMD/$3.55/Outperform), Gigamon (GIMO/$32.59/Outperform), Manhattan Associates (MANH/$60.54/Outperform), Newell Brands (NWL/$45.54/Outperform), and RingCentral (RNG/$19.08/Strong Buy).

The call for this week: Well, I will be in Denver this week seeing portfolio managers and presenting at events for our financial advisors. If past is prelude, something important will occur in the equity markets, just like happened late last week when I was giving a keynote presentation at Raymond James Financial’s national conference in Nashville where the music was GREAT. One of our advisors told me he loved the RingCentral (RNG) story since he has been using it with great results! I will be demoing it in the weeks ahead. This morning all is quiet on the western front with the pre-opening futures flat. But this week’s action should be a “tell” about how we play into mid-May . . .