Altitude Adjustment: Investing During a Period of Lower Returns and Higher Volatility

It can be difficult to adjust to the end of a good run. For years following the financial crisis of 2008, investors benefited from a rally in financial markets facilitated in part by expansionary policies of the Federal Reserve and other central banks around the globe.

2015 marked a transition in markets as the Federal Reserve hiked rates for the first time in nine years, and the rally in risk assets dissipated, while volatility moved higher. 2016 has begun in a volatile fashion too as we continue to grapple with divergent central bank actions against a backdrop of deepening concern about corporate (and sovereign) earnings and viability in the face of low commodity prices and a strong U.S. dollar.

Increased volatility and lower prospective returns are trends we have highlighted in our previous asset allocation publications in which we suggested investors broaden their investment paradigm to include traditional as well as alternative risk factors and be tactical across and within asset classes in order to generate attractive risk-adjusted returns. In addition, with asset valuations more mature and monetary policies becoming divergent, we believe investors need to “altitude adjust” their return expectations lower and volatility assumptions higher.

We also anticipate other changes to the investing paradigm as we look forward. We expect less consistency in the negative correlation between stocks and bonds relative to the past decade. We believe currency movements will play a much larger role in determining portfolio outcomes. Finally, we suggest investors not ignore the reduction in market liquidity and its potential consequences.

In this publication, we will explore these themes in greater detail and share our views on all major global asset classes.

Macroeconomic backdrop

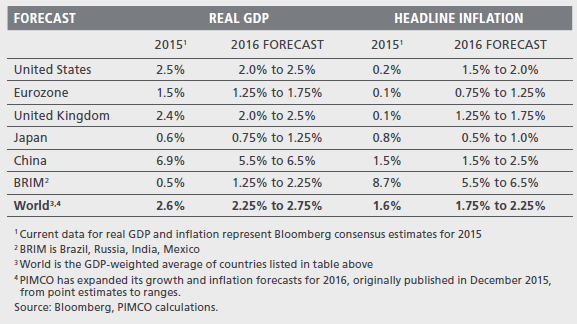

Our outlook for the global economy is for sideways growth with an uptick in inflation. Specifically, we expect the global economy to expand at a rate of approximately 2.25%–2.75% in 2016, continuing the modest trend from 2015. We expect the U.S. economy to expand between 2.0% and 2.5%, in line with its stable post-crisis recovery while growth is also steady in Europe and picks up slightly in Japan. In the emerging world, Brazil, Russia, India and Mexico (BRIM) should experience growth higher than 2015 as Brazil and Russia, while still contracting, improve from the deep slowdown of 2015. Meanwhile, China is likely to continue its bumpy journey toward a slower but more balanced economy.

There is greater uncertainty regarding inflation. Low oil and commodity prices are leading to increased concerns about deflation. However, we see a number of factors that could cause global inflation to pick up somewhat in 2016. Primary amongst these, we expect energy-related commodities to end 2016 significantly above both spot and forward prices (we discuss our reasons in the real assets section). In the U.S., slower appreciation in the dollar relative to recent history should remove some of the drag from last year. Further, as the economy operates closer to full employment, we should see a closing of the output gap and faster wage growth, leading to an uptick in inflation. If our base case view on oil prices ending 2016 around $50 per barrel is realized, we expect global inflation in 2016 to be in the 1.75%–2.25% range, up slightly from the 1.6% experienced last year.

Cyclical asset allocation framework

So why did so many investors benefit from strong market returns in the years following the financial crisis of 2008? To be sure, it helped that developed and emerging markets had a starting point of cheap valuations. Yet, in our opinion, a large portion of those returns can be explained by the drop in long-term real rates, which boosted the present value of all future cash flows, benefiting most asset classes. The U.S. dollar plays a unique role as the world’s reserve currency. So this cheaper U.S. dollar funding benefited most regions of the world.

However, as we had anticipated (please see prior Asset Allocation Outlooks, “Beyond Beta” and “Asset Allocation Without Tailwinds”, 2015 returns were more mixed as the Fed finally raised interest rates. In addition, weak commodity prices, poor corporate earnings and deterioration across the major emerging market (EM) economies of China, Brazil and Russia weighed on investor sentiment. Add on the market volatility at the start of this year, and many investors are asking: Are we nearing the threshold of the next global recession? At PIMCO, we don’t think so.

While there are risks to our outlook, as outlined in the prior section, we think the global economy will expand at a pace close to that of 2015, and fears of deflation should fade.

While this scenario could bring stability to some asset classes, we see three paradigm shifts underway that may necessitate a change in investing frameworks:

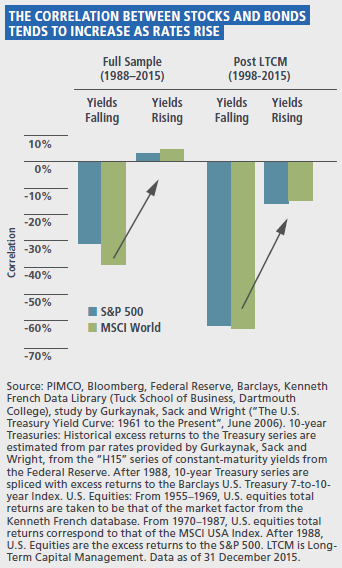

Less stable stock/bond correlation – We expect interest rates in G-3 economies to drift higher from their 2015 lows. If history is any guide, these periods are often associated with an increase in correlation between stocks and bonds.

Looking ahead, we think the recent regime of consistently negative correlations between stock and bond returns may become a bit more unstable. Acknowledging this regime shift is going to be critical for numerous investment strategies whose construction is predicated on the sustainability of this negative correlation.

Theoretically, as long as the “risk-free” discount rate and the dividend growth rate are independent, equities should have a positive correlation to bonds (ignoring the equity risk premium). This has indeed been the case for much of the past century, except for the negative correlation regime that began in the late 1990s. As inflation expectations finally became anchored in the 1990s, changes in discount rates became increasingly correlated with changes in growth, leading to the negative correlations between bonds and stocks that many investors now take for granted. If 2016 is likely to be a year of unchanged growth yet rising inflation expectations and rising yields (and a time where the Fed is sanguine about growth, but reacting to changes in inflation and inflation expectations) this would be an environment where the correlation between bond returns and stock returns could be less negative than expected, surprising investors and resulting in higher-than-expected volatility in portfolios that rely heavily on the stock-bond diversification hypothesis. Regardless, we believe bonds will continue to play an important role in investor portfolios of diversification, income generation and loss mitigation.

Importance of the “FX Factor” – Currency may have become more than simply a factor to hedge (or ignore) – it can potentially become a driving force of our economic and financial systems, and relatedly, central bank reaction functions.

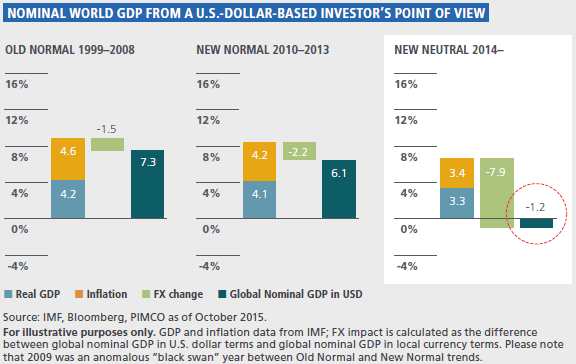

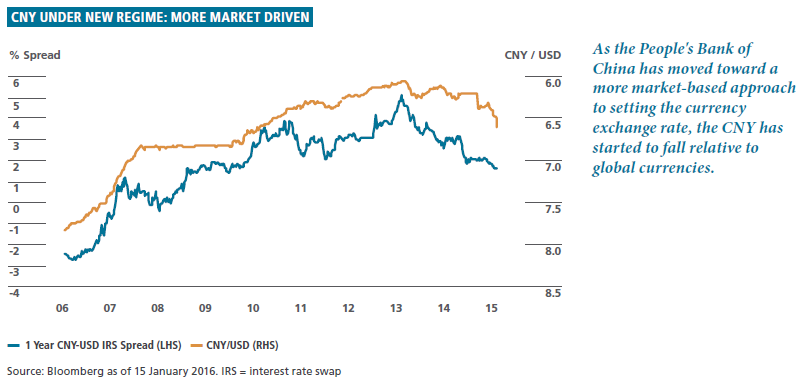

PIMCO’s New Neutral outlook says the global economy will experience modest growth and inflation accompanied by low interest rates. In the past, when real GDP and inflation were both higher, nominal economic cycles were relatively unaffected by currency swings as the volatility of FX was small compared with the growth rates of real GDP and inflation. However, as the graph below shows, when FX changes are high relative to growth and inflation, the investment landscape is far more sensitive to the FX factor and sudden nominal recessions can occur in the middle of what we might otherwise consider expansions. While we have not been in and do not think a recession is coming in 2016, adjusted for FX, global growth may feelmore tepid than it really is in 2016.

The result is a more volatile environment, not only on the macroeconomic scale, but also at the corporate scale. The FX factor affects corporations’ earnings as well as leverage and therefore feeds into financial conditions and wealth effects, in other words, back into the macro economy and from there into monetary policy. In a world of low nominal GDP, investors should consider integrating FX considerations not only in asset allocation decisions, but also in individual security selection as well.

Reduced market liquidity – There are two factors at work here. The first is increased regulations on banks toward the goal of making the financial system safer. This reduces capital allocated to proprietary risk taking (which is the intention of the new regulations) as well as to the market-making and financing functions. The reduction in market-making capacity causes investor flows to have much larger impacts as prices must reach a point where new investors are willing to take the opposite side of the price momentum (as opposed to a market maker who may warehouse the risk for a short time until another investor is found).

The second factor is the growth of systematic trading strategies that are programmed to respond to changes in volatilities in major asset classes, often exacerbating large market moves as market declines lead to higher volatility which then leads to programmatic selling. The same happens in rallying markets as volatility declines, leading to programmatic buying. These changes in market liquidity are often viewed solely as a problem, but overshoots in prices created by reduced liquidity can be opportunities to generate excess returns if investors are patient and positioned to provide liquidity when the market needs it.

Asset allocation themes for multi-asset portfolios

Overall risk: We are modestly overweight on overall risk positioning. While many assets had priced in the net present value boost of lower long-term rates, they have cheapened recently in response to uncertain monetary policy and commodity prices. Given our base case of continued modest growth with diminishing deflation fears over time, this means returns can still be earned via targeted risk taking.

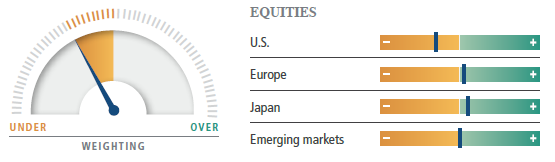

Equities: We are doubtful of the potential for equities to continue to deliver outsized returns. We believe a focus on relative value can add to return potential and our expectation of continued U.S. dollar strength coupled with continued quantitative easing from the European Central Bank (ECB) and the Bank of Japan (BOJ) leads us to slightly favor European and Japanese equities over U.S. equities. We also expect value-oriented stocks to begin to gain favor again in 2016.

Rates: We are defensive on interest rate exposure, while appreciating the risk-hedging properties of high quality bonds. Our base case is for a Fed that hikes gradually, but still hikes more than once in 2016 (which is all the market is pricing) and we see a return of some term premium to the bond market. We find UK rates particularly rich and Mexican rates attractive.

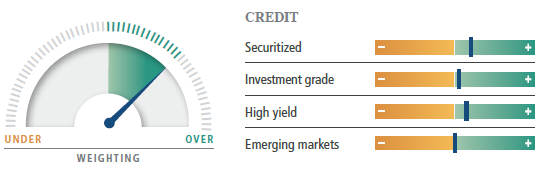

Credit: We favor credit, as a combination of increased supply and “infection” from the energy sector has led to valuations that are attractive for this stage of the business cycle. In a world of slow but positive growth and challenging equity returns we think a focus on high quality income will be key in generating attractive returns.

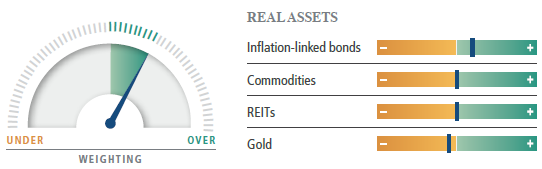

Real assets: We are selectively overweight real assets. Within commodities, we favor the energy complex over metals as supply and demand are both rebalancing in the former as a response to lower prices. Given the current level of inflation expectations, inflation-linked bonds could outperform nominal bonds even if our baseline view that oil prices will appreciate does not materialize.

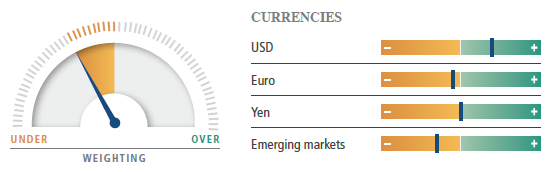

Currencies: We believe being overweight the U.S. dollar (USD) versus a basket of Asian currencies should deliver positive returns in addition to providing a valuable hedge against a greater-than-expected slowdown or currency devaluation in China. We favor targeted positions in developed market currencies, recognizing that in a world of lower nominal growth, currencies can serve as a tactical, liquid proxy for country exposure.

Global equities

We do not expect further deep declines following the market drop at the beginning of the year, as equity risk premia, while not cheap, do not seem particularly stretched in a world of low long-term rates. However, returns going forward are likely to be challenged in a world of slowly rising interest rates, headwinds to earnings and a slower pace of debt-financed share buybacks.

Therefore we are cautious on global equities and expect high return dispersion across countries and sectors. We believe that given current valuations, asset allocators are better compensated for taking equity risk higher up in the capital structure through the credit markets.

Companies will find it difficult to deliver earnings growth this year as modest economic expansion and low (albeit slowly rising) inflation is not the most favorable backdrop for strong earnings increases. Also, for corporations that derive a large share of their earnings overseas, higher currency volatility can be a big source of earnings growth or contraction. Further, valuation multiples have expanded meaningfully in many developed market regions over the past few years, responding to lower long-term rates. Looking ahead, we expect valuation multiples are likely to be stable overall, while perhaps experiencing a mild contraction in developed market equities.

Lastly, the paucity in earnings growth combined with the boost speculative stocks received from the drop in discount rates has resulted in a significant underperformance of value stocks. For years, investors chased fast-growing companies or embraced those that used financial engineering to deliver shareholder returns. While there should be a premium for real quality earnings growth, we believe the resumption of the Fed hiking should result in a reduced attractiveness for speculative growth stocks and resume the outperformance of value stocks with solid fundamentals.

Cautious U.S. equities

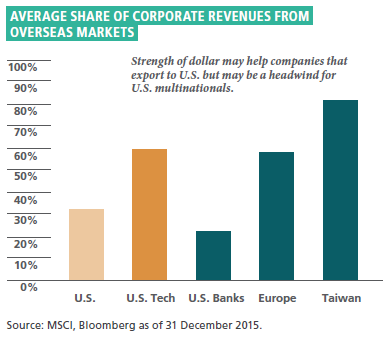

PIMCO’s expectations of continued U.S. dollar strength and modest upward bias in U.S. Treasury yields, coupled with our view that valuations are full, lead us to underweight U.S. equities. Within U.S. equities, we favor U.S. banks, which tend to have limited exposure to foreign exchange fluctuations and are more closely related to the health of the domestic economy. Moreover, in contrast to other sectors, U.S. banks are trading at a meaningful discount to the broader market and have significantly underperformed the broad market, while their earnings are coming in ahead of expectations.

Overweight European equities

European equities enjoy a favorable macro backdrop of a dovish ECB, which is expected to continue quantitative easing (QE). As European equities are highly sensitive to currency movements, earnings have a fair chance to continue to exhibit healthy advances as the euro weakens further. However, Europe’s equity markets could suffer disproportionally from weakness in the emerging markets, and financials could pay the price of deeper negative interest rates. As a result, we are modestly overweight European equities and shying away from financials. We remain mindful of the recent slowdown in earnings growth.

Overweight Japanese equities

We suggest an overweight to Japanese equities. Corporate earnings in Japan have proved to be resilient despite the relative stability of the Japanese yen in 2015 and the economic slowdown in Asia. Japan’s strong performance in the last five years has been supported by robust earnings growth as shown in the figure, “Global equity return decomposition 2010–2015 (annualized).” Further, we expect the Japanese market to be supported by continued structural reforms, better corporate governance and most probably further BOJ support in 2016 although we remain mindful of the risk from weaker Asian currencies.

Select opportunities in EM equities

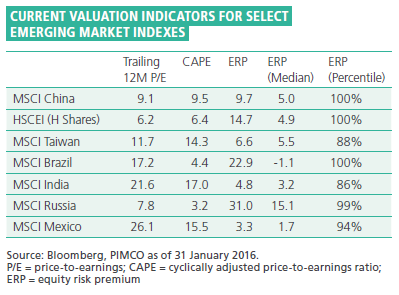

On the surface, the greatest value today appears in emerging market equities where valuation multiples are among the lowest in the world and near levels last seen during the global financial crisis. While we believe EM equities have the greatest return potential for long-term investors, corporate earnings in this region have disappointed year after year and expectations are still running fairly high. Given the strong ties of several EM economies to commodity prices, our outlook for commodities (excluding energy) is not optimistic enough for us to favor EM equities at this point. That said, we see specific pockets of value and will be ready to reassess the entire sector if positive catalysts do materialize given the value proposition that many markets offer.

Global rates

We are positioned with a small underweight in global rates, balancing our fundamental view of diminishing deflation fears and a return of some term premium to the bond market as the year progresses with the recession-hedging and diversification benefits of high quality bonds – benefits that remain important even in the context of the less stable stock/bond correlations discussed earlier.

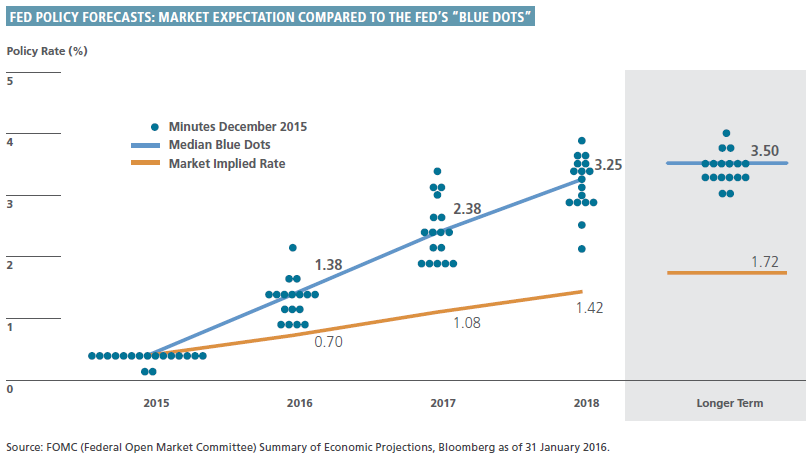

The Fed has embraced PIMCO’s New Neutral hypothesis and shared with the markets its belief that the neutral real rate is lower than its historical average. Moreover the Fed has to be cautious as its actions impact not just the U.S., but the global economy. Even so, we believe that not only is the market pricing too shallow a path of Fed hikes in the near term, but also that term premium and inflation expectations are too low. Currently markets are pricing only one hike in 2016, compared with the Fed’s own projection of three or four hikes.

Not only do we expect the U.S. economy to grow at an above-trend 2%+ rate, but also for headline inflation (as measured by the CPI) to move up from current levels. In this scenario we think the Fed is likely to hike more than the market is currently pricing. In addition, the term premium in the bond market (as modeled by five-year yields, five years forward) is too low and at levels from where it tends to rise. While part of the low term premium is justified by our New Neutral hypothesis, part of it is due to the market pricing a probability of deflation (the implied probability from the inflation options market is an approximately 10% probability that inflation is zero for the next five years). We think this deflation protection will get priced out of markets as we advance through 2016 and longer-term rates should rise. Both of these facts bias us toward an underweight in global rates.

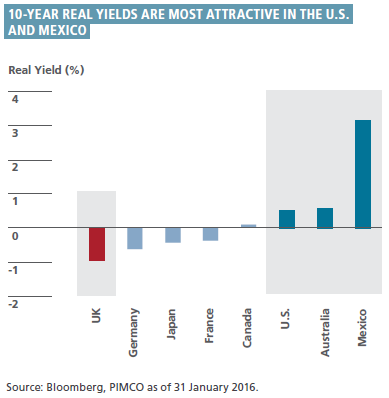

As with other assets, relative value is critical. If we are to be underweight, we would like to find the richest high quality global rate to be underweight. For example, compare long-term real rates in the U.S. versus the UK: In a world of low rates, the UK is at an extreme, even at a time when its economy and labor markets are strong and inflation is expected to move higher.

UK rates are lower than fundamentals would imply due to strong demand from liability-hedging pension funds as well as fears of contagion from mainland Europe coupled with poor market-making liquidity that tends to exaggerate flows.

In Europe we think the most attractive rates trade currently is to continue to hold an overweight to the large periphery sovereigns, Italy and Spain, versus German Bunds. Although spreads have compressed to approximately 100 basis points (bps) for 10-year bonds, we think these are likely to be supported by the continued ECB QE.

Finally, we are overweight Mexican rates. Mexico offers one of the highest real yields with steepest yield curves despite having tamed inflation with vigilant monetary policy. With below target inflation and below potential growth, we feel the 4.2% spread of 10-year Mexican swap rates above U.S. swap rates is likely to compress in 2016.

Global credit

We find that credit sectors currently offer the most attractive opportunities across risk assets. While credit spreads have risen over the past 18 months, we believe much of the widening is a result of contagion from the energy sector combined with large issuance volume and increased volatility and liquidity risk premia – rather than an increase in expected defaults. Increased yields now available to investors across both investment grade and high yield offer what we believe to be significant value.

We concede that there has been some deterioration in leverage ratios and increased uncertainty about the commodity outlook. As such, investors rightly should demand a higher risk premium to compensate for the increase in credit risk. However, interest coverage ratios are still at extremely manageable levels and we don’t expect a spike in defaults (outside the commodity sector) even in a scenario of modestly rising rates.

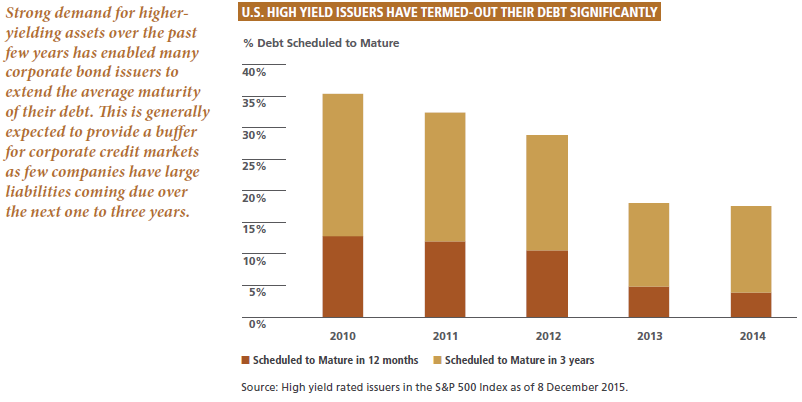

Spreads lately have widened to levels close to what one would expect ahead of a recession, which is not our base case over the next year. In contrast, PIMCO expects about 2.5% global growth and modestly rising inflation, which is a scenario in which spreads have typically been tighter than current levels. In particular, issuers have managed to term out debt, resulting in lower maturities and rollover risk over the next couple of years, adding to the positive return expectations from this sector.

On a near-term basis, expected defaults are not the only factor affecting credit spreads. One must also account for the beta to the equity market and the negative convexity of the asset class’s return profile (credit spreads tend to widen more in down markets than they tighten in up markets). Taking all of this into account, in our multi-asset-class strategies, we fund our overweight to credit from both equities and core fixed income. We find BB-rated (excluding energy) corporate credit the most attractive. In particular, we like the following credit sectors the most:

• Non-agency MBS in the U.S. that offer attractive risk-adjusted returns in the context of a modestly positive outlook on the U.S. housing market.

• European bank capital where we observe fundamentals are generally positive given ECB support and an improving economic backdrop.

• Senior bank debt in the U.S. is a sector that should benefit from ongoing regulatory focus on de-risking and de-levering balance sheets, but has counterintuitively widened as total loss-absorbing capacity (TLAC) requirements lead to increased issuance from the banks.

We also find numerous opportunities in consumer, telecom and healthcare sectors with solid or improving fundamentals. We continue to be highly selective in the energy sector, waiting for more attractive entry points. In particular, most high yield issuers need a more vigorous oil price or natural gas recovery than we expect to remain solvent, and are likely to default if prices stay around here for a prolonged period or fall further. We think there are opportunities to participate in a recovery in energy prices, but they are better expressed directly in commodity markets or inflation-linked bonds.

In U.S. taxable portfolios, investors may also consider an allocation to municipal debt strategies, particularly if they find themselves in higher tax brackets. While continued growth in the U.S. is generally a positive for municipal bonds, in today’s investment environment, rigorous credit selection is very important not only in corporate sectors as mentioned previously, but also within the muni sector.

Global real assets

We feel there are pockets of opportunity within the real asset sector despite the overall pessimism surrounding commodities and inflation.

We think the energy sector is currently the furthest advanced of the major commodities in rebalancing and hence has the brightest prospects. Low oil prices have supported demand growth at the fastest rate in a decade and supply, particularly in producing basins with greater short-term elasticity, has begun to turn lower. In 2016, we expect demand growth for oil to be 1.2 million barrels per day (bpd), in line with longer-term trends. Meanwhile, even the additional supply from Iran as sanctions are lifted will not match our forecast growth in global demand as Saudi Arabia continues to produce near its maximum capacity, Libyan production will likely remain curtailed and U.S. output is likely to fall. If our forecast is correct, the market will adjust from the current situation of excess inventories to a more balanced state or even a deficit as we move into the later part of 2016. All in all, our base case is for oil prices at $50 per barrel a year from today as renewed drilling in North America will be required by 2017 to meet demand growth. We recognize, however, that oil prices have been highly volatile and our price forecast could take longer to realize.

The story is different for the industrial metals complex, as growing Chinese production capacity for some metals combined with slowing demand to materially pressure prices lower. There is no minimizing or escaping the importance of emerging market growth, and China in particular, on the metal price outlook. Adjustments on the supply side are extremely slow due to long lead time and high capital intensity.

We retain our bearish outlook on gold from last year. Gold has declined more than 10% over the last year, and there may be more to go. Many market participants zealously allocate to gold as a liquid hedge against U.S. dollar debasement or runaway inflation, but this year is one where rising real interest rates and a strong dollar may dull gold’s luster. Moreover, governments in countries such as India that have a strong demand for physical gold are taking measures to divert savings in gold to savings in more productive assets.

We have long found real estate investment trusts (REITs) an attractively valued asset, but are currently neutral on the asset class at current valuations.

Finally, we believe one of the most attractive risk-adjusted return opportunities this year will be inflation-linked bonds like TIPS as a substitute for nominal Treasuries. Given identical credit and maturity profiles, substituting nominal bonds with TIPS may add some volatility (due to lower liquidity in TIPS) while we believe the spread between the two, which is a measure of market implied inflation expectations, should widen in favor of TIPS. Even if oil prices only reach the $40s, we forecast headline inflation in the U.S. in the range of 1.5%–2.0% for 2016 versus the current TIPS market implied rate below 1% for the next year. There could be additional upside if oil prices realize our more bullish forecast.

Global currencies

2014 and 2015 were years of large relative moves in G-10 currencies with the euro depreciating 21% versus the dollar and the yen sliding 12.5% versus the dollar over the two-year period. In fact, as discussed earlier, these moves dwarfed nominal GDP growth.

We do not expect the same magnitude of shifts to repeat themselves in 2016, particularly as the Fed is unlikely to tolerate a significant strengthening of the USD going forward, as that would threaten not only the health of U.S. corporate earnings and the recovery but have large impacts on the emerging markets and commodities which could then spill over into the U.S. However, while large moves are unlikely, we still expect the USD to remain strong, and calling the moves will be critical to equity and overall investing. Equity markets will not fare well without stability or support from FX markets because of the disproportionate impact on earnings and financial conditions in a New Neutral world.

The move in the Chinese yuan (CNY) toward a floating regime is a new development that has introduced a fair amount of volatility in foreign exchange. Not only is China a large component of the global economy, CNY moves have a large impact on the behavior of many other Asian currencies commanding all together 25% (31% if we include Japan) of the world nominal GDP, bigger than the U.S. at about 22% or the eurozone at 17%. Therefore the behavior of the CNY in 2016 will be a significant factor to watch, as it will influence global nominal growth, global inflation, commodity prices and corporate earnings – in other words, global financial conditions, and therefore to some extent the Fed’s and other central banks’ monetary policies.

We expect the CNH (the offshore pricing of the yuan) to depreciate more than currently implied by market pricing but to remain contained to the mid to high single digits. A depreciation of a greater magnitude could have a marked impact on our theme of stable growth and rising inflation, so we particularly like to be long USD funded by CNH and a basket of related Asian EM currencies. Not only do we expect to gain from this position, but it provides a good hedge to our baseline case of steady global growth and rising global inflation. This position is a key element to our overall portfolio construction at a time when duration might not be as powerful a hedge.

Tactical asset allocation, risk management and portfolio construction

In our view it is clear that we are in a transition from a market with cheap valuations, stable correlations and low volatility – all supported by dropping discount rates, predictable central banks and ample liquidity – to a market with fuller valuations, higher volatility and central banks that are less predictable (with the Fed starting to hike and the PBOC starting to make its presence felt). This is an environment where strategies that were successful over the past several years may not be as attractive going forward. Rather, the volatility and dislocations should create compelling investment opportunities. Indeed, active management’s potential for added returns has thankfully not shrunk as the chart showing the differences among the best performing and worst performing asset classes for any given year illustrates.

Sophisticated risk management technology is necessary but not sufficient to avoid unexpected drawdowns. Risk management should evolve to account for new paradigms like the unstable stock-bond correlations or increased importance of FX volatility even to currency-hedged asset class returns, as discussed earlier. We believe it is important to construct a portfolio of alpha trades that are diversified not just across asset classes but also across risk factors.

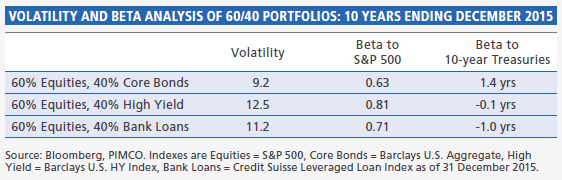

As the chart “Volatility and beta analysis of 60/40 portfolios: 10 years ending December 2015” shows, corporate bonds have sensitivity not just to duration risk, but also to equity risk. A simple example of this is the popular notion that the way to avoid losses during a Fed hiking cycle is to sell a core bond allocation into one with floating rate exposure, such as bank loans. However, at the extreme, moving from a portfolio of 60% equities and 40% core bonds to one with 60% equities and 40% bank loans would increase the volatility from 9.2% to 11.2% and the equity beta from 0.63 to 0.71 (assuming historic correlations), while giving up the recession hedging properties that a core bond allocation provides.

Closing remarks

We have centered our 2016 outlook on the basic assumption that global growth proceeds along PIMCO’s central case of around 2.5% accompanied by a modest uptick in inflation, and that the yuan’s depreciation will be contained to the mid to high single digits versus the USD, while oil prices move higher from current levels.

The most obvious risk to the downside is the one the market is currently fixated on – that the low inflation of 2015 slides into outright deflation in 2016. This could be due to a further unexpected drop in commodity prices, a larger-than-expected depreciation of the CNY or a greater slowdown in Chinese growth. Furthermore, given most global central banks are operating near the zero bound, they may not have a lot more room for stimulus if any of the above shocks materialize. As the first month in 2016 has shown, markets will be difficult to navigate. However, we feel there is still the potential to outperform markets if investors are patient and open to changing paradigms.

Disclosures

The “risk-free” rate can be considered the return on an investment that, in theory, carries no risk. Therefore, it is implied that any additional risk should be rewarded with additional return. All investments contain risk and may lose value.

Past performance is not a guarantee or a reliable indicator of future results. Performance results for certain charts and graphs may be limited by date ranges specified on those charts and graphs; different time periods may produce different results. Charts are provided for illustrative purposes and are not indicative of the past or future performance of any PIMCO product.

Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Equities may decline in value due to both real and perceived general market, economic and industry conditions. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Currency ratesmay fluctuate significantly over short periods of time and may reduce the returns of a portfolio. Sovereign securities are generally backed by the issuing government. Obligations of U.S. government agencies and authorities are supported by varying degrees, but are generally not backed by the full faith of the U.S. government. Portfolios that invest in such securities are not guaranteed and will fluctuate in value. Inflation-linked bonds (ILBs) issued by a government are fixed income securities whose principal value is periodically adjusted according to the rate of inflation; ILBs decline in value when real interest rates rise. Treasury Inflation-Protected Securities (TIPS) are ILBs issued by the U.S. government. Commodities contain heightened risk, including market, political, regulatory and natural conditions, and may not be suitable for all investors. Mortgage- and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and while generally supported by a government, government-agency or private guarantor, there is no assurance that the guarantor will meet its obligations. Bank loans are often less liquid than other types of debt instruments and general market and financial conditions may affect the prepayment of bank loans, as such the prepayments cannot be predicted with accuracy. High yield, lower-rated securities involve greater risk than higher-rated securities; portfolios that invest in them may be subject to greater levels of credit and liquidity risk than portfolios that do not. There is no assurance that the liquidation of any collateral from a secured bank loan would satisfy the borrower’s obligation, or that such collateral could be liquidated. There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market. Investors should consult their investment professional prior to making an investment decision.

Return estimates are for illustrative purposes only and are not a prediction or a projection of return. Actual returns may be higher or lower than those shown and may vary substantially over shorter time periods. It is not possible to invest directly in an unmanaged index.

This material contains the current opinions of the manager and such opinions are subject to change without notice. This material is distributed for informational purposes only. Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this publication may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America L.P. in the United States and throughout the world. THE NEW NEUTRAL is a trademark of Pacific Investment Management Company LLC in the United States and throughout the world.

© PIMCO