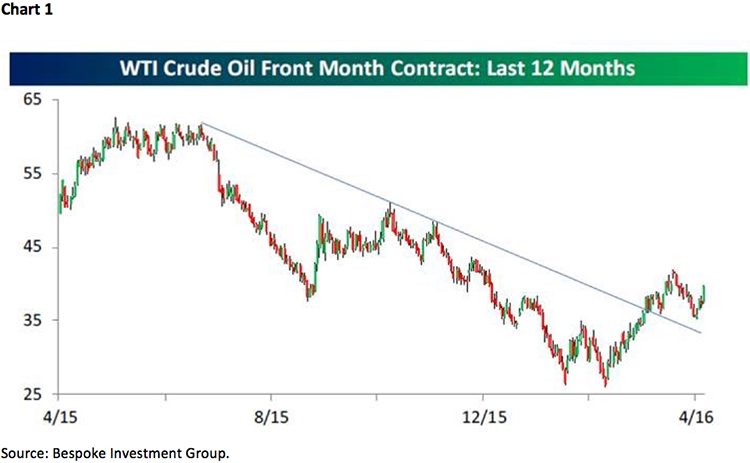

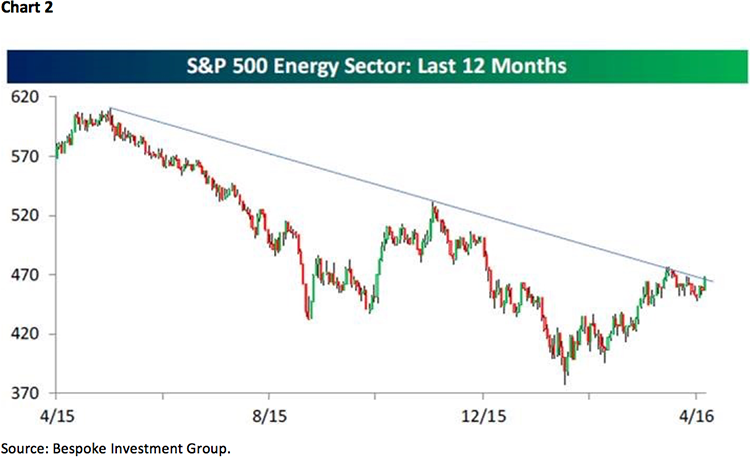

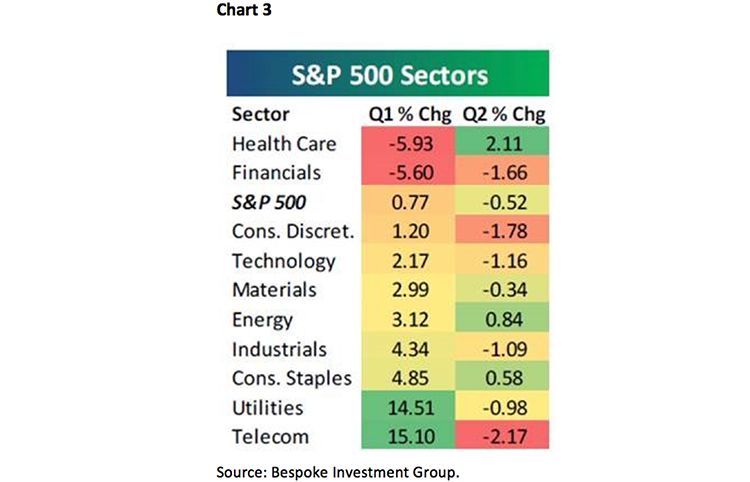

“Never on a Friday” is one of the mantras that has served me well over the years. Long time readers of these letters know its meaning. To wit, when the equity markets are involved in a pullback attempt they rarely bottom on a Friday. Nope, they tend to give participants time over the weekend to brood about their losses, tell their wives they can no longer buy the new Mercedes Benz (which makes for a pretty tense weekend), and consequently return to The Street of Dreams on Monday/Tuesday in “sell mode.” That sequence typically leads to the phrase “Turning Tuesday” implying the market bottoms either late in Monday’s trading session, or early the next day. In last Friday’s Morning Tack I reiterated said mantra and looked fairly foolish as the Dow Dance took the senior index over 150 points higher early in the day. Nevertheless, in this business you have to have certain disciplines to manage the risk and “never on a Friday” is one of my disciplines. Subsequently, as I winged my way back to Saint Petersburg, after a week of seeing accounts, speaking at a conference, and doing various media “hits” in New York City, as I traveled south, so did the equity markets. By Friday’s closing bell the Industrials (and the S&P 500) had lost 1.21% for the week, the Transports slid 1.92%, but the real loser was the S&P SmallCap 600 (-2.28%). As for the sectors, energy and healthcare were the only positive macro sectors for the week with energy better by 2.20% (driven by an 8.13% pop in crude oil prices). To be sure, crude oil has broken out to the upside of the downtrend line that has “capped it” for the past 12 months (Chart 1) and the energy sector is attempting to do the same (Chart 2). Meanwhile, the healthcare sector lifted 0.89% on the week, while the financials dropped a rather large 2.90%. To see what sectors worked in 1Q16, and what is working so far in 2Q16, please see Chart 3.

So this week in earnest begins the 1Q16 earnings report season, with expectations for earnings to decline anywhere from off 7% to off 9% y/y. Those negative estimates have been rising over the past number of weeks. Many pundits suggest that unless earnings, and forward guidance, are better than expectations, the equity markets will travel back down to the Netherworld of 1800 basis the S&P 500 (SPX/2047.60), but we are not one of them. As the good folks at Bespoke Investment Group note (as paraphrased):

Given that we track this kind of information on a regular basis, we looked to see how the S&P 500 performed during earnings seasons (six-week period beginning the Friday before Alcoa report) since the start of 2009. . . . Of the 28 reporting periods, the direction of the market during earnings season was the same as the net guidance spread only ten times (36%). Furthermore, in the last twelve quarters (three years) the guidance spread has been negative eleven times, and the S&P 500 has been down during the corresponding reporting period just once. As we have discussed in prior reports on the subject, when it comes to earnings season, what really matters is expectations heading in. When expectations in the form of analyst revisions are negative leading up to the start of earnings season, equities typically rally during earnings season, while positive sentiment leading up to earnings season sets a high bar to surpass.

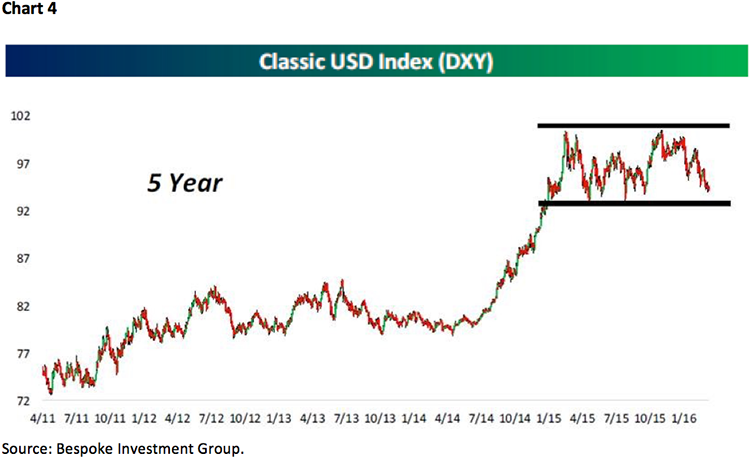

So in between speaking engagements and media events, I had the opportunity to meet with a number of portfolio managers last week. I always enjoy talking with Federated Investors’ Phil Orlando and some of the team in Boston and Pittsburgh. Two of the trends they have been discussing are the recent weakness in the U.S. dollar and the recent strength in crude oil. I told them that I have thought the dollar has been making a “top” for over a year as measured by the Dollar Index (Chart 4). My track record on oil, however, is not so good - having wrongly attempted to make a bottoming “call” on crude oil three times over the past year has not played! I did say that the head of our energy team has a pretty darn good record of doing so, having made the negative “call” on prices and then a few months ago making the bottoming “call.”

Next I met with JP Morgan’s Jeffrey Geller and Scott Davis and gleaned from these PMs that: 1) There is more earnings operating leverage in Europe than the U.S. 2) There is finally stability in emerging markets’ currencies and commodity prices. 3) There are just enough risks out there to balance the good that is emerging. 4) Portfolios should overweight: banks, brokers, insurance, auto, transportation, and semiconductors.

Then there was my friend Mary Lisanti, portfolio manager of the Lebenthal Lisanti Small Cap Growth Fund (ASCGX/$15.98). She told me, “When you talk to small-cap companies all you hear is that business is pretty good and that after this quarter’s earnings report you should have 6 to 7 quarters of easy comparisons.” She further opined the worlds’ central banks have converged in their views that interest rates are going to stay relatively low; and that even at $35 a barrel, the Permian Basin is profitable. At $40 she thinks there will be two or three more basins that will become profitable. Mary’s focus is small capitalization growth companies that do things better, faster, and cheaper, which is why I own her fund. We discussed many of the stocks in her portfolio, but I don’t have the space to mention them.

While I saw more PMs, as stated I don’t have enough space to talk about everything discussed. I will say my meetings with the real estate folks at Cohen & Steers were particularly timely since real estate is becoming the 11th GICS sector (instead of 10 macro S&P sectors there will be 11 beginning in September 2016). According to Cohen & Steers, that new sector has the potential of driving $100 billion into REITs from 40 Act mutual funds just to get them up to a portfolio weighting of neutral. They believe the small and mid-capitalizations funds are more underweighted than the large cap funds. Some of the team I met with help manage the Cohen & Steers Realty Shares Fund (CSRSX/$72.56).

The call for this week: So the insightful McClellan Report writes, “Bearish for short and intermediate trading styles, bullish long term. The DJIA fell back down through a previously broken downtrend line, not a good sign for the bulls.” Guy Ortmann, at Scarsdale’s Securities writes, “In conclusion, our near term outlook remains neutral while the intermediate term has turned ‘neutral’ as valuation issues are beginning to temper that outlook along with recent insider selling activity. Forward 12 month earnings estimates for the SPX from IBES (Institutional Brokers Estimate System) of $122.64 leave a 6.01% forward earnings yield on a 16.8 forward multiple.” And our friend, Mick St. Amour, at the astute The Collier Group writes:

While the S&P 500 has gotten ahead of itself since the mid-February lows, I suspect whatever pullback we get will be more consolidating and working off overbought conditions versus the start of another major move downward. Improving stock market breadth, a more dovish Fed, and the prospect that the worst of the earnings declines could very well be behind us tell me that the bear market scenario that we worried about at the beginning of the year is off the table for now. Investor positioning shows a reluctance to hop on board this rally, which also tells me there is still enough fuel in the tank for the S&P 500 to grind higher in the weeks and months ahead once we work off the overbought conditions. I think for the time being equity market weakness will be confined to the 1950-2000 region for the S&P 500 and this is where I would selectively add back to equities for underinvested accounts.

Plainly, we agree. While the number of stocks in the S&P 500 that remain above their 50-DMAs continues to be near-term overbought at 83.1%, the NYSE McClellan Oscillator has become somewhat oversold. Further, there has been a rather rare “breadth thrust” signal registered suggesting that near-term weakness in stocks should be bought with appropriate stop-loss orders to manage the risk. This morning the preopening S&P 500 futures are better by 9 points on no real overnight news. Chinese March CPI rose 2.3% vs. expectations for 2.5%, giving the PBOC the ability to stimulate; while Japanese Machine Orders beat estimates (-9.2% vs. -12.5%) helping to steady the yen.