There are two primary reasons Millennials aren’t saving like they should. The first is the lack of money to save, the second is the lack of trust in Wall Street. A recent post from JP Morgan, via Andy Kiersz, got me to thinking on this issue.

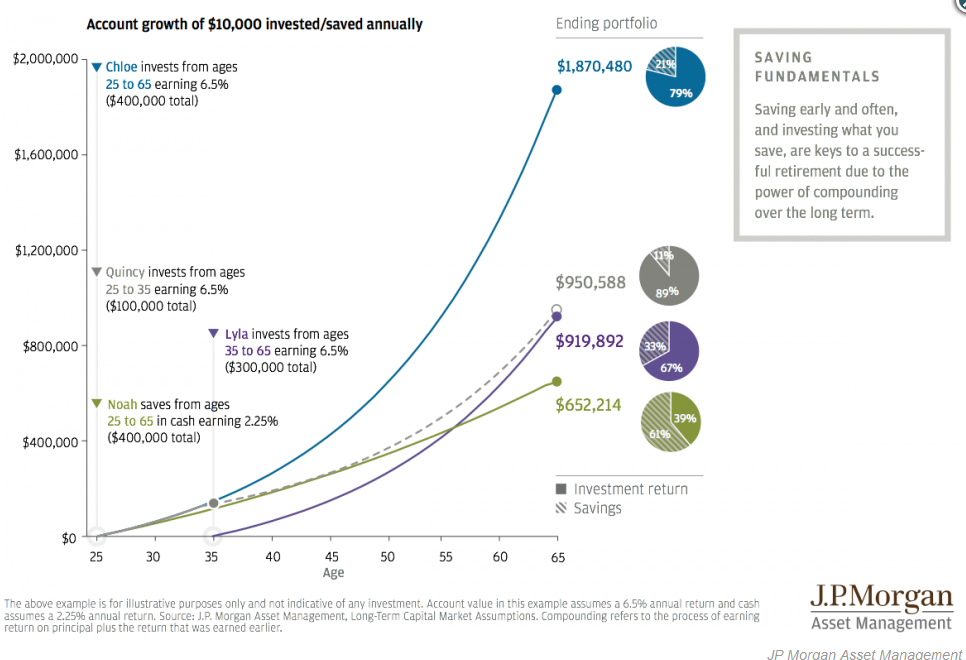

“JPMorgan shows outcomes for four hypothetical investors who invest $10,000 a year at a 6.5% annual rate of return over different periods of their lives:

- Chloe invests for her entire working life, from 25 to 65.

- Lyla starts 10 years later, investing from 35 to 65.

- Quincy puts money away for only 10 years at the start of his career, from ages 25 to 35.

- Noah saves from 25 to 65 like Chloe, but instead of being moderately aggressive with his investments he simply holds cash at a 2.25% annual return.”

There are two main problems with this entire bit of analysis.

Saving Is Problem

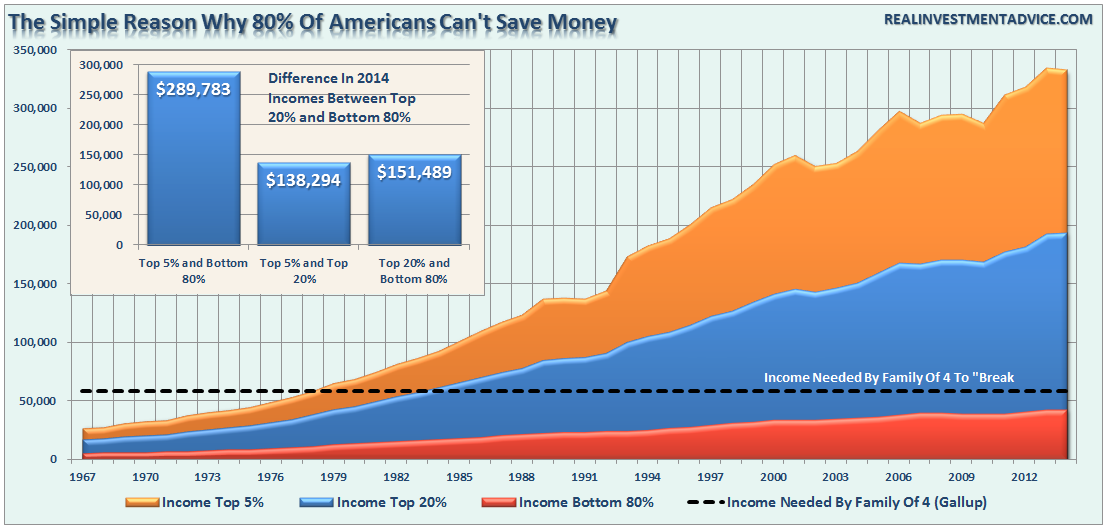

First, while saving $10,000 a year sounds great, the real problem is that median incomes in the U.S. for 80% of wage earners is $42,564 (via the Census Bureau, 2014 most recent data).

The problem, of course, is JP Morgan assumes that these young individuals are able to save an astounding 25% of their annual incomes. This is not a realistic assumption given that many of the Millennial age group are struggling with student loan and credit card debts, car notes, apartment rent, etc.

But it really isn’t just the Millennial age group that are struggling to save money but the entirety of the population in the bottom 80% of income earners. According to a Bankrate.com survey, 63% of American’s do not have enough savings to pay for a $500 car repair or a $1000 emergency room bill. However, as noted, it even covers a large number of higher income individuals as well.

“While savings predictably increase with income and education, even 46% of the highest-income households ($75,000+ per year) and 52% of college graduates lack enough savings to cover a $500 car repair or $1,000emergency room visit.”

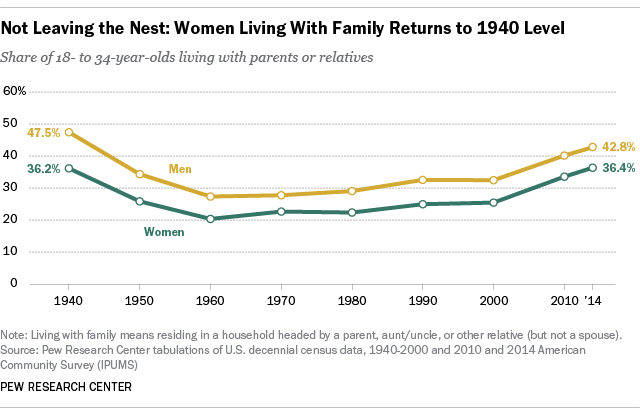

How are Chloe, Lyla, Noah and Quincy to save $10,000 a year when Chole works as a nursing assistant, Lyla waits tables, Noah is a bartender and Quincy works retail? (These are the jobs that have made up a bulk of the employment increases since 2009. They are also in the lower wage paying scales which makes the problem of savings for difficult.) This is also why Millennials are setting new records for living with their parents.

“Young people started moving out mid-century as they became more economically independent, and by 1960 only 24% of young adults total—men and women—were living with mom and dad. But that number has been rising ever since, and in 2014, the number of young women living with their parents eclipsed 1940s—albeit by less than a percentage point. And last year 43% of young men were living at home, which is the highest rate since 1940.”

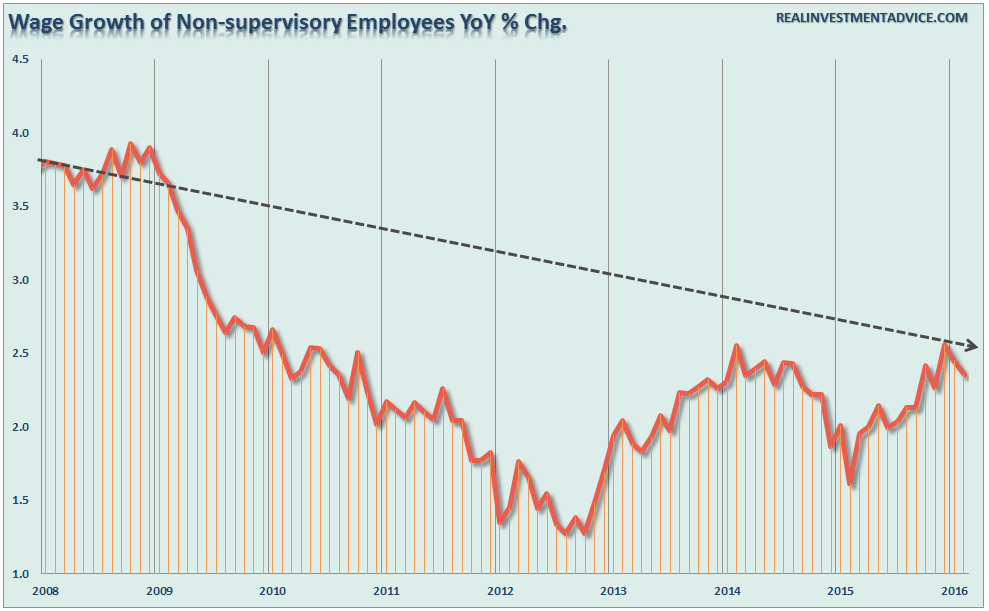

“But Lance, wages have been rising recently. That helps, right?”

While we have, at long last, seen an uptick in wages recently, the growth rate of wages remains well behind levels seen prior to the financial crisis. Wage growth remains woefully behind levels of rising healthcare, food and other related living costs that eat up a substantial portion of incomes reducing the ability to save.

Stocks Do Not Deliver Compound Rates Of Return

The second major problem with JPM’s analysis is the assumption that stocks deliver compounded returns over the long-term. This is one of the biggest fallacies perpetrated by Wall Street on individuals in the effort to entice them to sink their money in “fee-based” investment strategies and forget about them.

Compound returns ONLY occur in investments that have a return of principal function and an interest rate such as CD’s or Bonds (not bond funds.) This is not the case with stocks as I have explained previously:

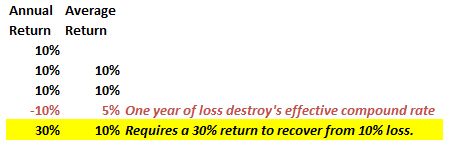

“First, while over the long-term (1900-Present) the average rate of return may have been 10% (total return), the markets did not deliver 10% every single year. As I discussed just recently, a loss in any given year destroys the ‘compounding effect:’

Let’s assume an investor wants to compound their investments by 10% a year over a 5-year period.”

“The ‘power of compounding’ ONLY WORKS when you do not lose money.As shown, after three straight years of 10% returns, a drawdown of just 10% cuts the average annual compound growth rate by 50%.

Furthermore, it then requires a 30% return to regain the average rate of return required. In reality, chasing returns is much less important to your long-term investment success than most believe.”

Secondly, while JPM’s assessment shows a nice smooth acceleration of wealth for the four individuals, there is a huge difference that occurs when accounting for the variability of returns during a long-term investment period. To wit:

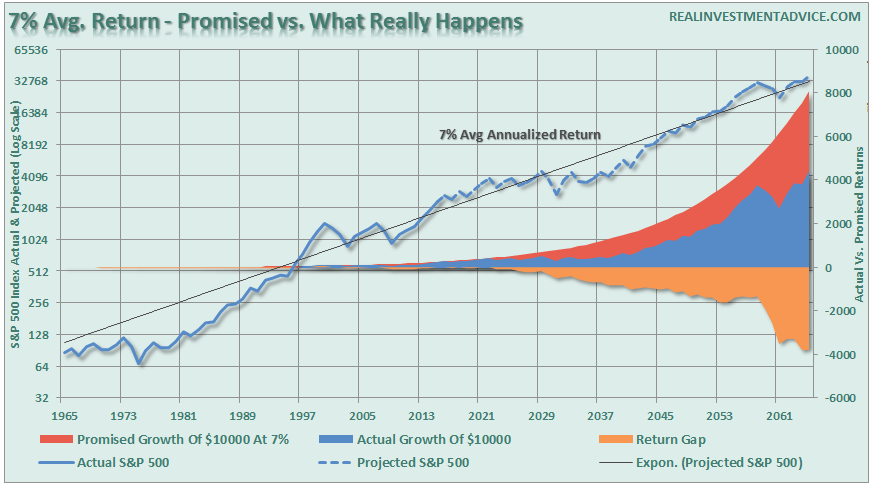

“Here is another way to view the difference between what was ‘promised,’ versus what ‘actually’ happened. The chart below takes the average rate of return, and price volatility, of the markets from the 1960’s to present and extrapolates those returns into the future.”

“When imputing volatility into returns, the differential between what investors were promised (and this is a huge flaw in financial planning) and what actually happened to their money is substantial over the long-term.”

Lastly, and probably the most critical point, is valuation level of the market when these individuals began the saving and investing program.

The problem for Chloe and her friends is that valuation levels are currently at some of the highest levels recorded in market history. The chart below shows REAL rolling returns for stock-based investments over 20-year time frames at various valuation levels throughout history.

Of course, none of this even includes the negative impacts to individuals and their savings due to the emotional and psychological impact of market volatility over time. As I discussed previously in “Dalbar: Why Investors Suck:”

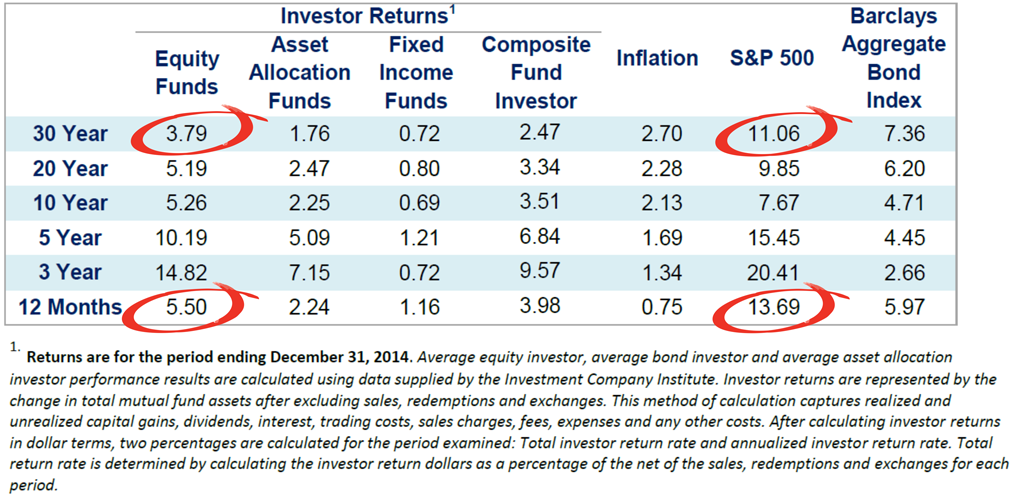

“In 2014, the average equity mutual fund investor underperformed the S&P 500 by a wide margin of 8.19%. The broader market return was more than double the average equity mutual fund investor’s return. (13.69% vs. 5.50%).”

Why is this? Well, according to Dalbar, there are three primary reasons:

- 25% Lack of capital to invest (Chloe can’t save $10,000 a year)

- 25% Capital needed for something else. (Noah is paying off student loan debt.)

- 50% Were directly related to psychological and emotional factors.

Of course, after years of watching their parents slaughtered by two massive bear markets, which Wall Street never warned of and were directly responsible for, is it any wonder that “trust” is a major issue?

See the problem here for Wall Street?

What Millennial’s, and everyone else, is starting to figure out is that Wall Street is not there to help you, but only to help themselves. “Long-term” and “buy-and-hold” investment strategies are good for Wall Street’s bottom lines as the annuitized revenue stream accrues each year. Unfortunately, for individuals, the results between what is promised and what actually occurs continues to be two entirely different things and generally not for the better.

Don’t misunderstand me. Should individuals invest in the financial markets? Absolutely. However, it should be done with a solid investment discipline that takes into account the importance of managing volatility and psychological investment risks. There are many great advisors that do exactly that, unfortunately, they generally aren’t found on the front pages of investment publications or in the financial media.

Of course, the problem to solve first is getting Millennial’s out of their parents basements and back into the work force. Having a job makes it easier to start investing to begin with.

Lance Roberts

Lance Roberts is a Chief Portfolio Strategist/Economist for Clarity Financial. He is also the host of “The Lance Roberts Show” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report".