The U.K. joined the European Common Market, what is now known as the EU, in 1973. In 1992, the Maastricht Treaty formally created the EU. However, as part of the treaty, the U.K. negotiated that it would be exempt from adopting the euro and joining the Eurozone. Despite the EU’s founding premise that members should seek an ever closer union, both politically and monetarily, the U.K. is questioning the net benefits of its membership altogether.

The British public’s perception of the benefits of the U.K.’s EU membership has always been mixed. Following a recent increase in public opinion asking to separate from the EU, U.K. Prime Minister David Cameron set a referendum on membership for June 23. Cameron supports remaining in the EU, especially after he was able to negotiate a deal with the EU regarding some hotly contested issues for the country. However, several other highly visible members of Cameron’s Conservative Party have stepped out in support of leaving the EU. Political discussions have recently become quite heated and will likely remain so until the June referendum. Additionally, political uncertainty will likely weigh on financial markets, increasing volatility as we move closer to the referendum date.

In this week’s report, we will take a look at the main factors leading to the call for Brexit and their impact on the economy and the markets. As always, we will conclude with market ramifications.

The U.K. within the EU

This is not the first referendum that the U.K. has held regarding its membership in the European community. The country held a referendum in 1975 shortly after it joined what was then called the European Common Market in which the popular vote favored staying in the EU by an overwhelming majority. However, it has remained a controversial topic. The British public is uncomfortable with the extension of EU control over the past 40 years since the initial referendum. Additionally, British influence has been diluted in the organization as the EU has grown, now comprised of 28 countries.

The discussion over the country’s membership encompasses both financial and emotional issues. The U.K. is a net financial contributor to the EU, meaning that the country pays into the common coffers more than it receives back. The public argues that these funds could be better used within the country. On an emotional level, the public values its sovereignty, preferring its own British politicians to shape policies rather than EU officials, who have many more constituents to serve. It is generally the public’s perception that the U.K.’s interests have not been well served by EU policies.

Additionally, a founding principle of the EU is the “free movement of people,” which has brought an increasing flow of immigrants into the U.K. Similar to the arguments made in the U.S. over Mexican immigrants, the number of mostly Eastern European immigrants into the U.K. is seen as taking jobs from the Brits. I lived in London during the time when many Eastern European countries joined the EU (including my own motherland, Estonia), and the public fully expected swarms of laborers to storm the U.K., taking jobs from the locals (one prominent symbol of this fear was that of the Polish plumber). It is true that many economic migrants have moved to the U.K. since 2004, many coming from other poorer EU member countries. However, not everything about immigration has been bad for the British economy. The flow of mostly young immigrants has allowed the U.K. to enjoy an improving demographic profile, unlike many other European countries. The young immigrants also boost aggregate demand and, in many cases, integrate easily due to their European background.

The Referendum

The U.K. will hold a referendum on its EU membership on June 23. The referendum will have one question, “Should the United Kingdom remain a member of the European Union or leave the European Union?” There are five key issues that are important in determining the outcome of the referendum.

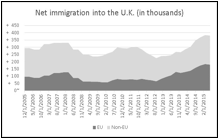

Migration. As previously mentioned, the issue of intra-EU immigration is a rational as well as emotional one. The blue-collar class of Brits perceives the intra-EU flows of immigrants as taking their jobs and reducing wages for everybody. The chart below shows net migration into the U.K. since 2005. During this period, net migration has been consistently positive.

(Source: U.K. Office of National Statistics)

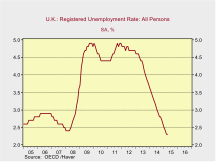

The chart below shows the unemployment rate during the same period. The 2008 crisis and 2011 European crisis caused a large increase in the unemployment rate. In recent years, the unemployment rate has declined and remains near historic lows despite the historically high net inflow of migrants from both EU and non-EU countries.

Trade. The EU is the U.K.’s largest trading partner and, as a member nation, the “free movement of goods” means that there are no tariffs, quotas or quality inspections on intra-EU trades. Many U.K. companies have expressed their continued support for EU membership as a more complicated export process could mean declines in trade. Although the U.S. is the single largest country for the U.K.’s exports, as a trading bloc almost half of the U.K.’s exports go to the EU. There are many factors that determine a country’s trade direction, but it is likely that the U.K.’s trade would decline with the EU, at least in the short run, if it leaves the EU. We note that Switzerland, which is not part of the EU, is the U.K.’s second largest single-country export partner, despite not being part of the Eurozone. It is possible that the U.K. could form similar trade agreements with other countries in Europe if it leaves the EU, but these deals will take time to negotiate and the uncertainty could create volatility in the short term. The U.K. would likely face an uncooperative Germany, who is also one of its largest trading partners.

The U.K.’s largest and fastest growing trade sector is services, with financial services representing a substantial portion. If the U.K. leaves the EU, London’s position as a major financial center could come into question as the EU looks to create its own financial center. At the same time, having a major financial center that is not directly tied to the EU or the euro (and thus, ECB monetary policy) could be beneficial to global investors. We note that similar arguments of London’s declining financial influence were made following the 2008 crisis, but the city has continued to prosper as a financial center.

The EU is also a large provider of foreign direct investment into the U.K. Again, this is most likely a result of the U.K.’s unique position as part of the EU but outside the Eurozone. We could see a temporary decline in these investment flows, especially during the uncertain period leading up to the referendum. However, longer term, this should not be a major issue whether the U.K. remains in the EU or not.

Policy and Regulation. As a member of the EU, the U.K. has to abide by the policies drafted for the benefit of all 28 nations. Even though it is the second largest economy in the bloc, it has to compromise on its own objectives. The question here is whether the benefits of belonging to the union outweigh the compromises that the country has to make.

The U.K. used to be an empire on which “the sun never set.” Thus, the popular narrative still supports sovereignty and struggles with the idea of being under another entity’s influence. This opinion is not likely to change anytime soon. The population was willing to turn a blind eye while times were good. However, since the Eurozone crisis and in light of increasing Middle Eastern immigration, many EU countries have started to more seriously weigh the benefits of membership against the costs.

Following the announcement of the referendum, PM Cameron was able to negotiate a deal addressing two main areas of concern for the British people.

First, the U.K. was granted an exemption from seeking an “ever closer union” with the EU, a long-term goal for all EU members. This exemption is important for the U.K. as the country was expected to eventually join the Eurozone, a direction that the British people highly disliked.

Second, PM Cameron negotiated an agreement that gives the U.K. more sovereignty over whether to extend social benefits to immigrants. The country now has the option to not extend social benefits to immigrants for a four-year period. We note that this is an option that the U.K. could use in a case of “severe economic hardship” caused by immigration.

Given these two agreements, PM Cameron is confident that EU membership is still beneficial to the U.K. It remains to be seen if it will be enough to convince the popular opinion.

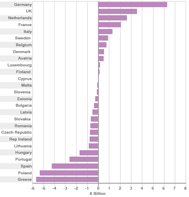

EU Budget and Benefits. As discussed above, the U.K. is a net financial contributor to the EU. The following chart shows the net contribution from each EU country in billions of euros. Germany is the largest net positive contributor. The U.K. is the second largest net positive contributor, with a net outflow of over €3.0 bn. The British population would like to see these funds used internally, rather than bailing out countries (e.g., Greece, Portugal, Spain) or supporting economic growth in poorer countries (e.g., Poland, Lithuania, Czech Republic).

(Source: BBC)

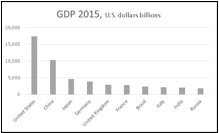

Influence. Lastly, but perhaps most importantly, the U.K. needs to determine if it wants to be a large fish in a small pond or a somewhat smaller fish in a large pond. The following chart shows the absolute size of the ten largest economies in the world (2015 data from the IMF). Currently, the U.K. is the second largest economy in the EU, but the fifth largest economy in the world as measured by GDP. Its current GDP includes Scotland, but if the U.K. votes to leave the EU then Scotland would hold its own referendum on leaving the U.K. The leader of the Scottish National Party recently said that although she supports an independent Scotland, a split caused by Brexit would be counter-productive to all parties involved.

(Source: IMF)

U.K. Internal Politics

Political debate has turned quite heated regarding the referendum. Although the ruling Conservative Party leader, PM Cameron, supports EU membership, some party members have openly supported the option to leave. Most notably, London Mayor Boris Johnson opposes the membership on the grounds that the country pays too much for too few benefits to the people. Johnson is quite popular, and his support could deal a blow to the campaign to stay. More than anything, Johnson’s political ambition could be behind his opposition as it has been speculated that he would be the next party leader (and thus possibly the next PM) after Cameron finishes his term.

Ramifications

This political uncertainty could have several outcomes, ripples of which we are likely to witness until a clearer path ahead is identified. Thus far, polls are indicating a close vote. If either side gains a substantial majority in the polls, we could see volatility subside, but until then the British risk markets and the currency will likely remain volatile and trend generally lower.

According to a Bloomberg survey, Brexit ranks as the most serious worry for European economists, well ahead of monetary policy and a Chinese slowdown. According to another Bloomberg survey, if the U.K. leaves, the probability of the country falling into a recession triples to 40%. Although the underlying economics will not be affected until the U.K. actually decides to leave, we are likely to see falling investment as manufacturing and investor confidence declines. Additionally, the Standard & Poor’s rating agency put the U.K. on a negative outlook watch, which is likely to tighten credit conditions.

At the same time, the Bank of England (BOE) has a range of tools which it is ready to use. It could keep monetary policy easy until volatility has abated. The BOE’s Eurozone counterpart, the ECB, could also employ additional stimulus when it meets in March.

The pound has weakened to its lowest level since 2009. According to a Bloomberg survey, a majority of economists see the pound falling to $1.35 or below within a week of the referendum vote; these are levels last seen in 1985. We remain cautious about the currency, especially as we approach the referendum date. The following chart shows the pound’s trading range since 2000. The pound has fallen 19.2% since reaching its most recent high in 2014. We could see further weakness in the currency, with the consensus of economists calling for a level of $1.35.

(Source: Bloomberg)

During the Scotland independence debate, conditions intensified shortly before the referendum. Similarly, volatility is likely to increase as risks cloud the minds of investors despite recent improvements in the U.K.’s economy. The currency markets, in particular, are likely to remain volatile, with short-term unpredictable moves possible.

The referendum will be a close one, and the outcome will be affected by more than the purely economic and financial arguments. It is also an emotional dilemma for the British people as Cameron needs to find a balance between those who see EU membership as a long-term economic and political advantage and those who believe that Britain is weighed down by the same factors.

Kaisa Stucke

February 29, 2016

This report was prepared by Kaisa Stucke of Confluence Investment Management LLC and reflects the current opinion of the author. It is based upon sources and data believed to be accurate and reliable. Opinions and forward looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

|

© Confluence Investment Management LLC

© Confluence Investment Management