2016 Outlook: A Slow and Gradual Fed is Nothing for Municipal Investors to Fear

SUMMARY

- We expect the municipal market to provide opportunities for investors who choose credits carefully and are positioned to take advantage of bouts of volatility.

- Municipals offer several benefits such as the potential for better-than-equity after-tax returns with significantly less volatility, attractive tax-efficient income and low correlation to other asset classes.

- High-tax-bracket U.S. retail investors should consider whether municipals should be a significant allocation for their portfolios.

Municipals were among the top performing asset classes in 2014 and 2015 amid global volatility, with the bulk of returns coming in the form of tax-efficient income. PIMCO expects 2016 to look similar due to the outlook for U.S. economic growth, assumed monetary policy and improving overall credit health.

Our baseline view for the global economy is formed at or during quarterly meetings, or forums, that include all of our global investment professionals and our senior advisors including former Federal Reserve Chairman Ben Bernanke, Nobel Laureate Michael Spence and former presidential aide Gene Sperling. After our December forum, PIMCO this year forecasts U.S. real GDP growth of 2% to 2.5% and moderate inflation of 1.5% to 2%, which are supportive of an allocation to municipals. Importantly, the overall U.S. economy is slowly improving. Meanwhile, continued lower inflation expectations should somewhat anchor yields at the long end of the curve.

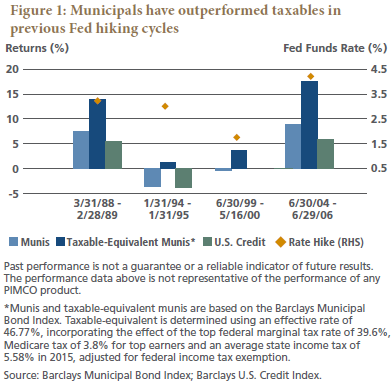

Monetary Policy and the Impact of Rising Rates

As the Fed embarks on its hiking cycle, we expect municipals should outperform taxables on a taxable-equivalent basis as they have in prior tightening cycles (see Figure 1). The reason is that the value of tax-efficient income to investors increases at higher absolute yields. Also, most municipals are issued with a call option, which provides for a price cushion as rates rise. Additionally, in the New Neutral world, with rates predicted to remain lower for longer and rise only gradually, investors should expect to receive more of their total return from income. Municipals should deliver on that expectation with an attractive tax-efficient income component.

PIMCO’s Outlook for Puerto Rico and Municipal Credit

We think that Puerto Rico will dominate municipal-related headlines again in 2016 and the decision to invest – or not invest – in Puerto Rico will continue to be a major driver of high yield municipal returns. Puerto Rico, which represents almost 25% of the Barclays High Yield Municipal Bond Index, was down 12.01% in 2015. PIMCO believes the commonwealth’s liquidity position remains extremely tenuous; the majority of its recent debt service payments relied on the claw-back of tax revenues from other public agencies. As complex negotiations with creditors proceed, the island’s political leaders also will continue to lobby U.S. Congress for federal aid and/or access to Chapter 9 bankruptcy law. However, Washington remains divided on the form of assistance and whether the island should have access to bankruptcy protection. The probability is increasing that a federal fiscal control board will be part of any eventual legislation. This is problematic for investors as the rules have yet to be written and may conflict with perceived bondholder covenants already in place. Adding to uncertainty and policy risk, a Supreme Court ruling on the restructuring of the island’s public corporations is expected this year and there will be a gubernatorial election in the fall. Lastly, Puerto Rico has yet to release audited financials for the fiscal year that ended 30 June 2014. Because of the lack of clarity and transparency regarding the island, PIMCO municipal-focused portfolios maintain zero exposure to Puerto Rico and its associated public agencies. While we foresee another action-packed year for the commonwealth, we do not predict Puerto Rico’s problems will spill over to the rest of the municipal market.

Beyond Puerto Rico, municipal credit health is generally improving, supported by the continued U.S. economic expansion. Tax revenues have rebounded to pre-recession levels, and state and local governments recently made their greatest contribution to U.S. GDP growth since 2009 (see Figure 2). The frequency of municipal defaults and bankruptcies remains low and is falling from the recessionary peak. Additionally, household formation has improved, and lending conditions remain favorable. We see opportunity in certain housing-linked credits such as regional land deals.

Nevertheless, the recovery remains uneven, affecting regions and governments differently. Rating agency upgrades have outpaced downgrades but we have witnessed an increase in the number of “super” downgrades, defined as multi-notch negative rating agency actions. This phenomenon illustrates greater dispersion in municipal credit quality and the importance of forward-looking independent credit research. As we near the peak of the credit cycle, research will become a larger driver of municipal performance as credit dispersion becomes more observable. Many weaker municipal credits struggle with rigid long-term fiscal commitments, including costs from servicing unfunded public pension liabilities. The challenge has been compounded by chronic underfunding by local governments, and these liabilities may continue to grow with an aging U.S. population. New rules from the Governmental Accounting Standards Board (GASB 67/68) have recently improved municipal disclosure and accountability, but may reveal to investors an off-balance-sheet financial commitment not previously identified. Identifying and avoiding these challenged credits early in the credit cycle will reward investors later on. Our portfolios favor essential revenue bonds over general obligation bonds as revenue bonds typically have smaller pension commitments, enjoy special revenue status in municipal bankruptcy and tend to exhibit vertical demand curves.

We also recognize that the municipal market is not immune to developments in the global financial markets. For example, the supply shock in oil markets has resulted in lower fuel costs benefiting not only consumers but some oil-sensitive municipal issuers such as toll roads and sales tax bonds. On the other hand, several energy producing states now face budget gaps driven by the fall in oil. Similarly, some energy- and commodity-linked corporate issuers in the municipal market have come under pressure from falling oil prices and stepped-up volatility in commodity and financial markets. Many of these tax-efficient bond valuations still look stretched relative to parity taxable corporate debt and should be avoided until prices adjust further. For active managers of municipal portfolios like PIMCO, volatility and extreme changes in valuations often present opportunities.

At this juncture, we don’t view the risk/reward profiles of many lower-rated and less liquid high yield segments as particularly attractive given the relative tightness of high yield credit spreads. Our extensive bottom-up research of municipal credits has turned up some exceptions. For example, we continue to see value in Master Settlement Agreement (MSA) tobacco bonds, which returned 15.75% in 2015 as measured by the Barclays High Yield Tobacco Index, and remain a good source of tax-efficient income and portfolio liquidity. MSA tobacco bonds may continue to benefit from lower gasoline prices which has led to more miles driven and a slowing of the decline in cigarette shipments, which will have a compounded benefit on internal rates of return going forward. In addition to their attractive valuations at current levels, MSA tobacco bonds are also some of the most actively traded and liquid bonds in the municipal market.

PIMCO’s Outlook for Municipal Market Liquidity

Similar to 2015, we see overall new issue supply high again in 2016 as refunding activity continues in the low rate environment and the federal government recently passed a large spending bill removing uncertainty around funding. Supply may even surpass 2015’s $398.4 billion as pent-up infrastructure needs and a lower emphasis on austerity could lead to increased issuance. As we saw last year, the market should well absorb the supply. We forecast positive demand for the asset class to continue as municipals have exhibited strong and steady performance amid global volatility and investors continue to seek income in a low yield environment. However, it is imperative to navigate thinning liquidity, as measured by a decline in broker/dealer holdings from over $50 billion pre-crisis to less than $20 billion now and secondary trading volumes that are the lowest in a decade. This thinning liquidity is expected to continue in the years to come and will likely create attractive opportunities for active managers like PIMCO.

Conclusion

The combination of continued U.S. growth, muted global inflationary pressures and gradual Fed tightening bodes well for the municipal asset class in 2016. We expect the municipal market to provide opportunities for investors who choose credits carefully and are positioned to take advantage of bouts of volatility. PIMCO’s integrated top-down and bottom-up investment process informs our portfolio positioning and security selection. Municipals offer several benefits such as the potential for better-than-equity after-tax returns with significantly less volatility (see Figure 3), attractive tax-efficient income and low correlation to other asset classes. As a result, high-tax-bracket U.S. retail investors should consider whether municipals should be a significant allocation for their portfolios.

DISCLOSURES

Non-municipal focused portfolios managed by PIMCO may hold Puerto Rico municipal bonds that have been economically and legally defeased by US Treasuries.

All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. High yield, lower-rated securities involve greater risk than higher-rated securities; portfolios that invest in them may be subject to greater levels of credit and liquidity risk than portfolios that do not. Income from municipal bonds in the United States may be subject to state and local taxes and at times the alternative minimum tax. Management risk is the risk that the investment techniques and risk analyses applied by PIMCO will not produce the desired results, and that certain policies or developments may affect the investment techniques available to PIMCO in connection with managing the strategy. There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market. Investors should consult their investment professional prior to making an investment decision. It is not possible to invest directly in an unmanaged index.

This material contains the opinions of the author but not necessarily those of PIMCO and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. This is not an offer to any person in any jurisdiction where unlawful or unauthorized. | Pacific Investment Management Company LLC, 650 Newport Center Drive, Newport Beach, CA 92660 is regulated by the United States Securities and Exchange Commission. |PIMCO Investments LLC, U.S. distributor, 1633 Broadway, New York, NY, 10019 is a company of PIMCO. | No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America L.P. in the United States and throughout the world. THE NEW NEUTRAL is a trademark of Pacific Investment Management Company LLC in the United States and throughout the world.

©2016, PIMCO.

CMR2016-0128-161565

© PIMCO