Italy’s Banking Crisis

On January 1, 2016, the EU implemented a new bank restructuring directive. The new and stricter rules are aimed at forcing private stock, bond and deposit holders to accept losses before public funds would be used in a bank restructuring. Although all EU countries are affected by these new rules, Italy remains of particular concern due to the number of distressed loans in the country. The Italian banking index is down almost 20% in 2016 due to concerns over nonperforming loans in the country’s banking system and the limited protection that private investors will receive under the new directive.

This week, we will look at the overall health of Italy’s banking system as well as the nonperforming loan problem in the country. We will explore the various issues affecting Italy and the EU with regard to finding a solution for Italy’s troubled banking system.

Nonperforming Loans

Nonperforming loans (NPLs) are loans that debtors are not paying off as agreed upon, but which have not yet been written off by the banks. All countries’ banking systems have some level of NPLs.

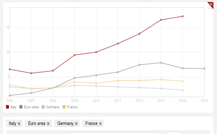

The chart below shows NPLs as a percentage of total gross loans for various countries. In 2014, Italy’s (red line) ratio stood at 17.3%. The Eurozone average (dark gray line) was 6.8% in the same year and Germany’s ratio was 2.3% (light gray line). By comparison, the U.S. ratio was 1.9% in 2014 (not shown on the chart). Some sources peg the 2015 level for Italy at 18.0%.

(Source: World Bank)

Another measure of NPLs is the ratio of NPLs to GDP. Italy does not have the highest ratio of NPLs to GDP in the Eurozone. In fact, Cyprus, Greece and Ireland all have worse ratios than Italy. However, Italy represents an outsized risk due to its large size. It is the third largest economy in the Eurozone, after Germany and France, and the eighth largest economy worldwide. Thus, while smaller European countries may have worse NPL ratios, the relative size of “bailout” funds for those countries pales in comparison to what would be needed in Italy. This makes a banking crisis in Italy much more serious than a crisis in any other smaller European country.

The BRRD

The EU Bank Recovery and Resolution Directive (“BRRD”), which became effective at the beginning of this year, requires that shareholders, bond holders and even large depositors bear the costs of a bank restructuring before government funds will be used to bail out the failing institution. This mechanism is informally called a “bail-in,” with stakeholders providing the funding as opposed to a “bail-out” which uses public funding.

In the case of a business failure, it is not uncommon to require shareholders to lose money. Even certain classes of bond holders usually lose some, if not all, of their investment. The approach, which was first used during the Cyprus bank failures in 2012-2013, will require losses from all subordinated debt holders as well as accounts with balances over €100,000. Smaller deposits would still be excluded from the bail-ins.

Background on Italy’s Markets

The Italian bond market enjoyed a period of falling yields in anticipation of the euro’s introduction. Financial markets interpreted the euro to mean that all Eurozone countries’ credit qualities would converge and ultimately would be guaranteed by the single monetary union. The chart below shows Italian 10-year Treasury yields. After falling in the late-1990s into the creation of the Eurozone on January 1, 2000, yields remained stable and low until the Eurozone crisis in 2009 when it became clear that not all credits were created equal within the Eurozone. However, the subsequent easy monetary policy by the European Central Bank (ECB) as well as the effects of the central bank’s asset-purchase program lowered yields to historically low levels.

The chart below shows the Italian stock index over the same time period. Stocks have experienced greater volatility as the underlying economic growth has remained constrained.

Following the Eurozone crisis, Italian banks avoided an EU-backed bail-out. However, as a result, the country’s banks hold a disproportionate level of NPLs, especially when compared to banks in countries that were able to remove NPLs from their balance sheets through a bail-out (e.g., Spain, Ireland).

The Italian Small-Scale Bank Rescue

In November 2015, the Italian government restructured four small banks. Implemented ahead of the new Eurozone “bail-in” directive, the restructuring pushed losses onto not only stock and bond holders but also absorbed deposit accounts that were larger than €100,000 before using government funds. The bank rescue was relatively small at €250 mn, but it gathered public attention after a pensioner committed suicide as a result of losing his life’s savings in the restructuring. It appears that he owned the bank’s bonds, believing them to be low-risk assets. A complicating twist to the Italian bank situation is that the banks often sold their subordinated bonds to retail investors as a substitute for deposits, and depositors mistook them for safe investments. As a result, many Italian retail investors are overexposed to the banking system bonds.

Consequently, the Italian government has initiated a case-by-case resolution to help “irregular bond purchasers” who bought the bonds without understanding the risks involved. This policy is likely to fail due to the difficulty in applying for it in practice, the increasing popular opinion demanding a “blanket” guarantee to retail clients and the EU opposition to guarantees.

Bad Bank

Italy has not been able to create a “bad bank” where it could accumulate the nonperforming loans. Spain and Ireland were able to help their banking systems by creating bad banks during the 2011-2012 bail-out crises. However, Italy has encountered recent opposition from the EU as the creditor nations are now more reluctant to bail out other countries’ banks. During the 2011-2012 Eurozone crisis, the monetary union was more open to providing support for countries that officially sought a bail-out, while current regulations oppose the use of “state aid” to bail out private banks. The use of EU funds to bail out banks has been virtually eliminated under the new BRRD rules.

Additionally, under the new rules, each large depositor is liable for knowing the underlying health of the bank. In reality, it will be hard for retail investors to know this so it would mean that depositors should diversify their risks by opening several smaller accounts in various banks or move their money across the borders to other European countries. For example, neighboring Spanish banks were restructured via Eurozone bail-outs in 2012, thus reducing bad debts and currently leaving them in a healthier financial position than Italian banks.

In this banking environment, the possibility of bank runs will be increased as depositors grow increasingly nervous about the safety of their savings. Similar to the U.S. bank runs of 1907, rumors can feed panic, which can lead to bank runs that ruin even healthy banks. In addition, if a bank is forced to liquidate a loan under stress, the price discount it would have to accept would in turn weaken the bank’s financial health, leading to more deposit withdrawals and creating a never-ending vicious cycle.

A deposit insurance system usually soothes some retail investors’ worries over bank runs. Although no EU-wide deposit insurance is in place, an Italian deposit insurance system does exist (Interbank Deposit Protection Fund), which should protect deposits of up to €100,000. According to estimates, the average size of a bank account in Italy is €13,200 (source: MutuiOnline), so it appears that many bank accounts would be protected by the insurance.

However, the size of actual funds available for deposit insurance is uncertain as the latest data is from 2013. The larger banks will also require significantly larger funds. For example, Monte dei Paschi, Italy’s third largest bank, holds roughly €45 bn of NPL. By comparison, the private losses in the restructuring of the four small banks in November were about €790 mn.

Positive Developments

There are a couple of positive developments in Italian banking. First, in November, the rating service Fitch raised its outlook for Italian banks to stable from negative. Although ratings agencies are not always right, this should at least allow Italian banks to borrow at more attractive rates. Second, loan creation growth has continued. Increasing loans potentially means more diversification away from the nonperforming loans. Of course, this trend would only be helpful if the new loans are of higher quality, resulting in less nonperforming loans, and the new loans are not simply used to refinance the nonperforming loans. Third, a wave of consolidation in the Italian banking sector may mean that some of the weaker and smaller banks would be absorbed by safer counterparties. However, we note that in the long run this may bring its own problems and bigger does not necessarily mean safer in the current Italian banking landscape. Last, but not least, the Italian economy is forecast to grow at a slow but steady rate this year. The chart below shows the country’s year-over-year GDP growth.

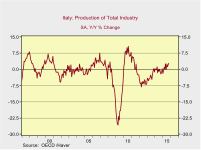

Perhaps more importantly, Italy is finally seeing a positive rate of industrial production growth, although production has not surpassed its pre-2008 high. Some of this industrial growth could be due to the low petroleum product prices, so we may see a slight pullback of industrial growth when crude prices rebound.

The Way Forward

The Italian banks’ current situation is made more difficult by the political wrangling both within the country and the EU. Although the Italian government supports a wide-scale banking system restructuring, EU opinion has swung to opposition.

The Eurozone’s monetary policy is currently largely driven by Germany, which is trying to avoid using its taxpayers’ money to bail out other countries’ bank bond and deposit holders. During the Cyprus banking crisis, the Eurozone took a tougher stance for the first time, forcing private bond and deposit holders to suffer losses. Germany has to balance two conflicting goals. On the one hand, it does not want to use its own funding to guarantee other Eurozone countries’ depositors. German public opinion especially opposes covering other countries’ bad debts while the German people have accepted austerity. On the other hand, it does not want leaving the Eurozone to become an attractive alternative. Thus, it has to give Italy just enough to keep it from leaving the monetary union.

We do not anticipate a solution to emerge soon. The two sides will likely come to a workable solution, but only after an extended period of brinkmanship. The most likely outcome would be that the EU and Italy agree to a solution that falls within the “direct state aid” category, despite northern European opposition. It is clear that Italy needs some sort of a solution to help clear the bad loans out of the banking system and prevent bank runs. With almost one-fifth of the country’s loans deemed nonperforming, the loan problem needs to be addressed and will not simply “work itself out.” Italy is arguing for access to EU funding to clear the bad debts, while the EU is trying to push haircuts on private investors and depositors.

In the longer term, a possible EU solution could involve a loan to Italy to boost its deposit insurance funds. However, we do not expect a solution to be reached until the banking situation has deteriorated further.

Ramifications

The uncertainty in the Italian banking sector is likely to increase volatility for the banking sectors of weaker Eurozone countries. We could also see increased cross-border capital flows as depositors will likely move money to a country with a more favorable banking system. If countries implement capital restrictions as a result of the capital outflows, bigger Eurozone-wide problems could develop.

Although other countries’ banking sectors could be affected in the short term, contagion risk to other countries is still low.

Kaisa Stucke

January 25, 2016

This report was prepared by Kaisa Stucke of Confluence Investment Management LLC and reflects the current opinion of the author. It is based upon sources and data believed to be accurate and reliable. Opinions and forward looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

Confluence Investment Management LLC

|

© Confluence Investment Management LLC

© Confluence Investment Management