Men can be trained to be inventors by the simple process of telling them that it is not a disgrace to fail. In research work there is no such thing as failure in the accepted sense of the word. It is as important to know how not to do a thing sometimes as it is to know how to do it. And out of these ‘intelligent failures’ often come astounding by-produces which open other avenues of learning. These are the rewards of the open mind.

Charles “Boss” Kettering was an American automotive engineer, businessman, inventor, and the holder of 186 patents who was the head of research at General Motors. My father met Kettering during the late 1940s and often reminded me of the aforementioned quote. I recalled the quote when I received a pretty nasty email from someone I don’t even know about my call for a “rip your face off rally.” The phrase he kept using was “you failed!” The reference was regarding the Thursday/Friday two-step (12/17 and 12/18/15) that lopped some 620 points off of the D-J Industrials. Prior to that, however, the set up looked perfect for “the rip.” The 309-point Dow Downer of Friday, December 11th was a 90% Downside Day, meaning 90% of the total Upside to Downside volume came in on the downside. The following Monday/Tuesday action proved to be two 80% Upside sessions and that sequence tends to mark a bottom. The next day (Wednesday 12/16) also was an 80% Upside Day, lifting the senior index by ~224 points, but the late week action erased the early week win. As stated, I think it was the $1.2 trillion dollar options/futures expiration that caused the 620-point slide, but whatever it was it certainly broke the rhythm of “the rip.” Undeterred, the Industrials were better by 123 points last Monday, 165 points on Tuesday, and 185 points Wednesday before Thursday’s holiday-shortened session lost 50 points. Last week’s action put the market capitalization weighted S&P 500 (SPX/2060.99) back into positive territory for the year at up 0.10%, but the equal weighted S&P 500 is still down 3.17% year-to-date. That is more representative of 2015’s market consternations with 47% of the components in Lowry’s Operating Company Only universe of stocks down 20% or more from their respective 52-week highs. Indeed, a difficult year!

Despite Thursday’s setback the S&P 500 has rallied noticeably from its 1990 – 2000 support level before stalling at its 50-day moving average (DMA) and 200-DMA of 2064.48 and 2061.48, respectively. All of the indices we monitor were better for the week with the best being the Value Line Arithmetic (+3.72%), which makes sense as participants position themselves for the fabled January Effect. According to The Street.com:

At the end of the year, investors start worrying about taxes. To that end, they may sell some stocks that they've seen a loss on -- not because they don't like them anymore, but because they can take those losses out of their annual bill from Uncle Sam. This selling will knock stocks down a bit toward the end of the year -- particularly small-caps, since they're not as liquid. In January, investors will be in there buying back their lost darlings, giving stocks a boost.

Speaking to the sectors, all of the S&P macro sectors were higher last week with the worst being Consumer Discretionary (+1.35%) and the best Energy (+4.60%). To the Energy, and tax loss selling, points, there are a number of names in the Raymond James research universe of stocks that qualify as tax loss bounce candidates and have favorable ratings from our fundamental analysts. The names that have a decent dividend yield and screen positively on our algorithms, include: Apache (APA/$45.80/Outperform); Hess (HES/$50.57/Outperform); Occidental Petroleum (OXY/$69.20/Strong Buy); and Chevron (CVX/$92.05/Outperform). Of course in the Master Limited Partnership (MLP) space there are a plethora of names that qualify. Of note is that the Alerian MLP Index (AMZ/289.77) has rallied 21.45% from its December 7, 2015 intraday low (242.57) into last Thursday’s intraday high (294.62). While some pundits like select names in the upstream MLPs, Andrew and I prefer the midstream names since they have less sensitivity to the price of crude oil. Many of the energy stocks appear to be bottoming and so is the price of crude oil. I spoke with our Director of Energy Research recently, namely Marshall Adkins. Recall that Marshall made the negative “call” on crude oil prices, but last week he told me that his model is looking more bullish than it has in four years. After my three failed attempts to pick the bottom for crude, I will defer to Marshall’s model. Almost on cue, oil rallied 9.79% last week, but natural gas fell 9.41%, likely due to the warm temperatures.

The year 2015 is about to enter the history books as one of the more difficult years in recent memory. Some indices are up (NASDAQ 100 +9.12% YTD) and some are down (D-J Transports -16.60%). Revenue growth has been lackluster, as have earnings, and the Fed is raising interest rates. However, history shows equities have tended to do pretty well in the months following a Fed rate hike. Yet many investors are worried about current stock market valuations in a higher interest rate environment. JP Morgan addresses this concern by writing:

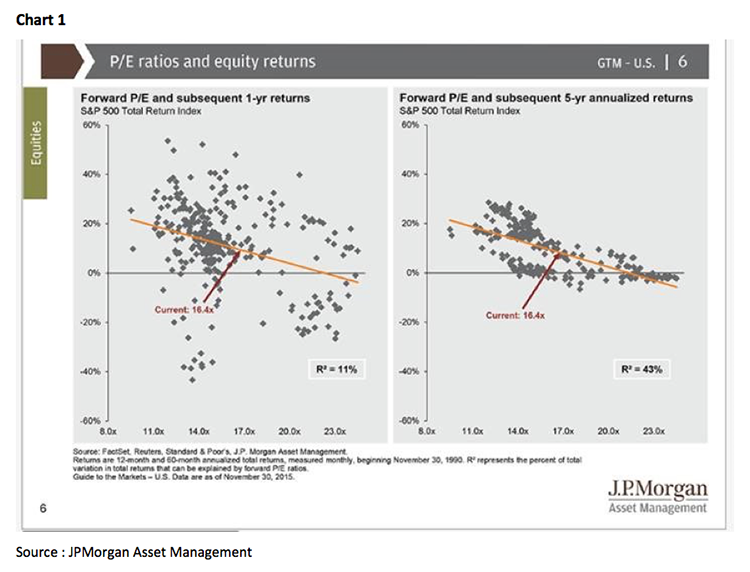

Over one year, valuation is a fairly unreliable predictor of future returns. In fact, since September 1990 valuation has only explained 9% of the S&P 500 return over the following 12-months – one might be better off reading tea leaves. Looking at the relationship between valuation and 5-year annual returns since 1990, the current level of forward P/E ratios suggest we are entering an environment of lower but more stable returns (see chart on page 3).

Meanwhile, over at Goldman Sachs, Chief Economist Jan Hatzius and his team, after analyzing the data, say that the U.S. economic recovery has about four years before it ends (https://binaryoptionevolution.com/2015/11/11/goldman-u-seconomic-recovery-4-years-ends/).

In conclusion, our 2016 outlook is supportive of equities driven by improving global growth, slowly rising interest rates, a stronger U.S. dollar, and low inflation. I expect equities to outperform bonds, commodities, and alternative investments. Managing the “risks,” and rebalancing portfolios accordingly, should be the key for successful investing in the new year.

The call for this week: We have not yet given up on the “rip your face off rally” theme. But if the market “tells” us we are wrong, we will quickly admit it, in keeping with one of my dad’s mantras, “If you are going to be wrong, be wrong quickly for a de minimus loss of capital.” Manifestly, it is no disgrace to guess wrong, the mistake is to stay wrong! Or as Leon Levy said, “An investor has to have the ability to adjust to being wrong. In other words, you can’t be too stubborn. You must have a certain degree of flexibility as to what’s going on.” And this morning “what’s going on” is that the preopening S&P 500 futures are lower (-7) on concerns over a 2% drop in crude oil prices and worries about China’s slowing economy. Alas, it must be a Monday.