More Money Has Been Lost Reaching for Yield than at the Point of a Gun

“More money has been lost reaching for yield than at the point of a gun.”

. . . Ray DeVoe’s unprovable but highly probable theory #2.5

Raymond DeVoe went on to write:

Because of an accident in college I took a year off and worked on the floor of the New York Stock Exchange, initially as a Page and subsequently as an Apprentice Specialist’s Clerk. Returning to college I was offered the opportunity to become a dual major in Economics and Mathematics. I completed the requirements and graduated a year late – but those three disciplines have worked at cross-purposes ever since. The precision of mathematics conflicts with the shifting vagaries of economics, and both are quite removed from the emotionally charged world of finance and trading – where real money is won or lost in a true meritocracy. To reconcile these I have put together all sorts of “Laws” and “Theories” including some, like the title above, which are unprovable but highly probable in my opinion. For the College Humor Magazine I submitted a collection of many “Laws” and other items, including my “College Course Descriptions,” 1) If it’s green, wiggles or slithers, it’s biology; 2) If it stinks, it’s probably chemistry, although don’t rule out economics; 3) If it doesn’t work, it’s most likely physics – but keep the economics option open; 4) If it’s incomprehensible, it’s probably mathematics, but that’s part of economics also; 5) If it sticks, doesn’t work, is incomprehensible and doesn’t make sense – it’s either economics or philosophy.” When I made these up I thought they were original, but I have seen many modifications of many of them. My “Law of Ruination” which goes “There are four ways to be ruined in this world – by sex, gambling, drinking and economics. To be ruined by sex is the most fun, gambling is the most exciting, drinking is the most debilitating – and ruination by economics is the most certain.

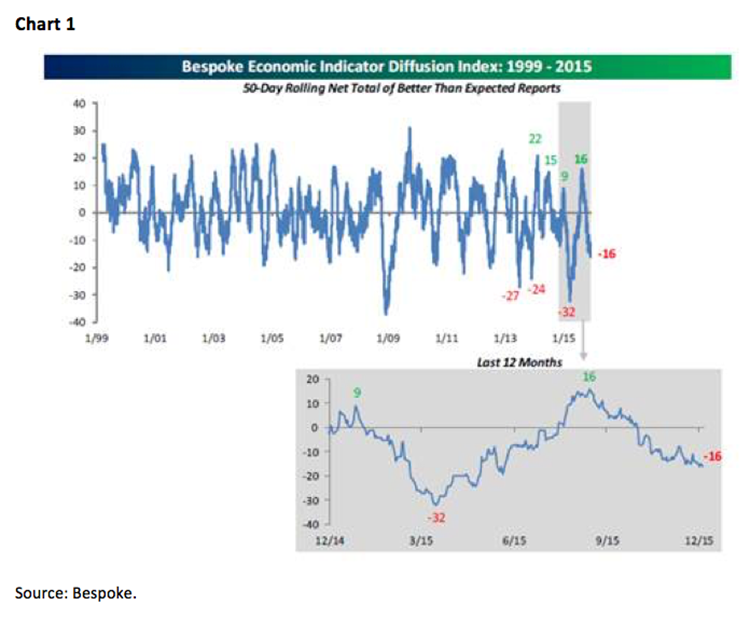

And last week, DeVoe’s “unprovable but highly probable” theory about ruination by economics played in spades: 1) the U.S. ISM services index fell (55.9 vs. 59.1), 2) the U.S. ISM manufacturing index traveled below 50, 3) the trade deficit rose, 4) U.S. exports slid, 5) consumer confidence fell, 6) pending home sales were weaker than expected, 7) home refinance declined, 8) vehicle sales were below estimates . . . well, you get the idea (see chart 1 on page 3). Yet the biggest economic goof came from across the pond when ECB president Mario Draghi delivered an expanded economic policy that just wasn’t up to snuff. The result left world equity markets reeling on Thursday, the euro soaring while the U.S. dollar dove, and bonds getting a shellacking. Yet, Thursday’s wild ride was pretty much in keeping with last week’s schizophrenic market action.

A schizophrenic week, indeed, with a ~10 point loss for the S&P 500 (SPX/2091.69) on Monday followed by a 22 point pop on Tuesday and then 23 point decline on Wednesday and 30 point loss on Thursday, capped by Friday’s 42 point rally. Such action caused the erudite Doug Kass (Seabreeze Partners) to term the stock market “An unplayable market.” Friday’s fling erased the mid-week slump, leaving the SPX better by 0.08%. It also enabled the SPX to recapture, and travel above, its 200-day moving average (DMA). Of course, the solid employment report was one of the drivers of Friday’s win, but the icing on the cake was likely because, after seeing what happened on Thursday, a contrite Mario Draghi began talking about the potential for “more aggressive actions by the ECB if needed.” The resulting stock action caused StockCharts.com’s John Murphy to write:

Stock indexes gain 2% . . . stocks are having a huge day on Friday. Stock indexes are showing gains of 2%. Chart 2 shows the S&P 500 gaining 40 points nearing the close. Its ability to bounce back above its 200-day line is also impressive. That gives its recent [chart] pattern the look of a "pennant" or "symmetrical triangle", which usually leads to higher prices.

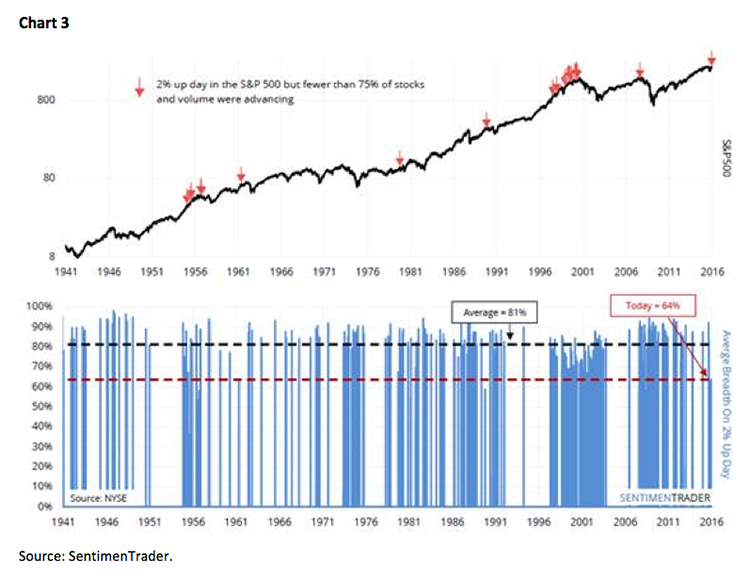

Clearly, Friday’s gain was impressive on the surface. However, drilling down into the entrails of the rally renders a more subdued conclusion. As my friend Jason Goepfert (SentimenTrader) writes:

Once again, we're dealing with a lack of participation. The S&P 500 gained more than 2% on Friday, but fewer than two-thirds of stocks and volume on the NYSE were in advancing issues. This was the 9th-worst breadth day since 1940 on a day the S&P gained 2% or more. The past two years have been more of these kinds of divergences than any time period outside of the late 1990s (chart 3).

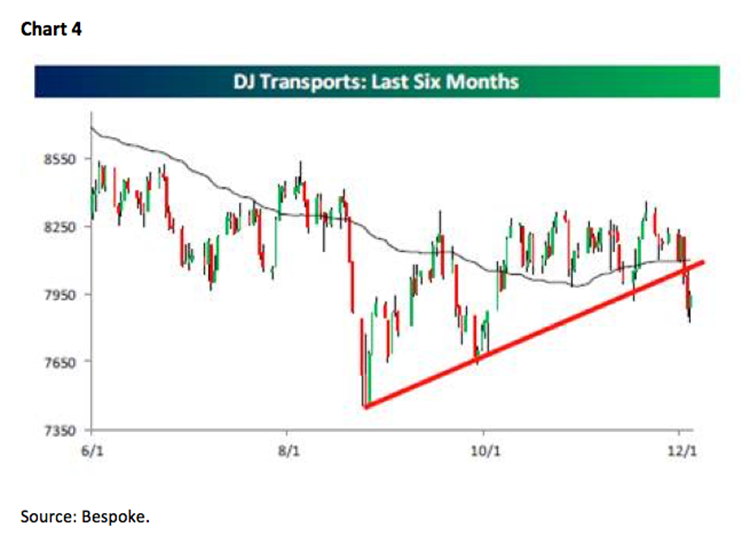

I would add that Friday’s new highs over new lows also diverged with 44 new highs and 98 new lows. Speaking to the breadth divergence, parsing the S&P 500 shows that, since the May 21, 2015 stock market high, 208 stocks of that index’s components are up and 292 are down. Also on the divergence front is the D-J Transportation Average’s (TRAN/7954.83), which should be soaring with the drop in the price of crude oil but is, in fact, breaking down (chart 4). The Transports came under pressure last week, causing them to break below their rising trendline that has been intact since the August lows. Clearly, the Transports are not confirming the strength in the Industrials. Maybe that will change this week as we enter the timeframe where the typical Santa Claus rally begins. While nobody really knows what causes the Santa rally, the guesses include: the ebullient seasonality, yearend bonuses, money managers attempting to minimize tax liabilities, a limited audience as Wall Street deserts the scene for the holiday, anticipation of the “January Effect,” etc. Whatever the reason, since 1928, the SPX has risen in the month of December roughly three-fourths of the time. Moreover, I have learned the hard way, while it can happen, it is TOUGH to put stocks away to the downside in December.

In response to the plethora of requests I have received for tax loss bounce ideas (meaning stocks that are sold to establish a tax loss that should “lift” when that selling abates), the two most hated groups that make sense to me are the midstream Master Limited Partnerships (MLPs) and the precious metals stocks. Of note is that gold made what a technical analyst would term a bullish outside reversal in the charts last week when it traded to a multi-year low and then closed above the previous week’s high. In the gold complex, there is only one large cap name that is positively rated by our fundamental analysts and meets the tax loss bounce criteria, and that name is Goldcorp (GG/$12.73/Outperform by RJL). In the midstream MLPs, however, there are a number of names that meet the criteria and carry a positive rating from our fundamental analysts. They are: Enterprise Products (EPD/$22.93/Strong Buy), Enterprise Transfer Partners (ETP/$33.79/Outperform), Genesis Energy (GEL/$34.53/Outperform), Kinder Morgan (KMI/$16.82/Outperform), and Plains All American (PAA/$21.16/Outperform). As a sidebar, there is a very negative story in today’sBarron’s titled, “Kinder Morgan: Don’t Say We Didn’t Warn You,” which is what you tend to see at “bottoms.” In said article, EPD is also mentioned.

The call for this week: In the last line of Friday’s “Morning Tack”, I wrote, “The result was that a lot of technical damage was done to the SPX yesterday, but it will take a much bigger decline to dent the overall bullish case.” I guess we will find out this week if that is the case, or if Friday’s fling was just a one day wonder. Stay tuned . . .

P.S. – I am in NYC all week doing media and seeing accounts; back next week.