A couple of weeks ago I wrote a strategy report titled “Friends.” In that report I scribed, “Regrettably, too many of my friends’, and stock market icons’, stories have been lost forever. One of the best writers I ever knew on the Street of Dreams was my friend Barton Biggs (Morgan Stanley). . . . Other deceased notables include: Alan “Ace” Greenberg (Bear Stearns), Henry Singleton (Teledyne), Muriel Siebert, Marty Zweig . . . well, you get the idea.” Today, it is with great sadness that I report another icon passed away last week when Dow Theorist Richard Russell left us. Richard began writing the Dow Theory Letter in 1958 and continuously wrote it until recently. To my knowledge it was the longest running investment letter written by the same person on record. Yet, the letter wasn’t just about investing, because Richard shared his life’s journey and personal experiences with subscribers. There were always tidbits of psychology, emotional experiences, and thoughts imbedded in his manifestos. Richard made you think! I began reading him when I entered this business in 1971. When I began writing strategy letters at EF Hutton in December 1974 (see attached on page 5) I wrote Richard and told him he was responsible for my prose.

Richard recommended gold stocks in the 1960s before the great inflation surge, called the “top” of the post-WWII secular bull market in 1966, and announced the end of the 1973 – 1974 bear market in December of 1974. In early 1975 he recommended “steel stocks,” noting that in every bull market the steel stocks have made massive gains and hereto he was right as the steel stock soared in 1975 – 1976. The last time I personally saw him was at a cocktail party during my friend John Mauldin’s conference in La Jolla in 2009. I was bullish and so was Richard, but I think we were the only ones at said conference that were bullish.

In one of his final missives Richard wrote:

A lot of lies can be told about a stock, but dividends don’t lie. In order to increase dividends, a stock must create a history of producing cash. Analysts can lie, earnings can lie, CEOs can lie, but dividends don’t lie. A company must increase its actual earnings in order to raise dividends. The only thing better than dividends is the float produced by an insurance company. The float, plus compounding, made Buffett a wealthy man.

Another mentor of mine (my father) agreed with Richard’s dividend advice, but added some other insights. He told me that the first thing to read in an annual report is the auditor’s statement. If it is a qualified statement, that’s a red flag. The second thing to read is the “footnotes.” Doing that kept me out of Enron because I could not understand all the transactions that were taking place between Enron’s various partnerships. Third, look at “retained earnings”; if there is a continuous buildup of retained earnings it is a good thing. Of course such a buildup implies dividend increases; and some of the best performing stocks over the last 50 years have been those companies that have increased the dividend by 10% per year forever.

Speaking to the current stock market, and Dow Theory, Richard Russell agreed with Jack and Bart Schannep of TheDowTheory.com organization when they wrote:

The requirements for a (re) buy have been met effective 10/9 for the Original Dow Theory… You'll see the bounce was “from 3 weeks to as many months” and the pullback met the 3% threshold as outlined by Robert Rhea in his 1932 classic book The Dow Theory. Incidentally, the other prominent Dow Theorists (Dow Theory Letters - Russell, and Dow Theory Forecasts - Moroney) are in rare agreement on this signal. Hope you will find this helpful.

I responded to the Schanneps by writing:

I have studied Robert Rhea and the Schanneps correctly highlight this subtle point from his seminal book The Dow Theory. But as I recall, this point was not proffered by the creator of Dow Theory (Charles H. Dow 1851 – 1902) in his original Wall Street Journal editorials, or by Dow Theorists William Hamilton and George Schaefer. Of course I could be wrong, but I do not have the time to go back and reread all of them. All I can say is by my interpretation of Dow Theory the “sell signal” of August 25, 2015 has not been reversed, yet I really hope the Schanneps are correct because I continue to ignore that “sell signal” for often stated reasons.

So far the Schanneps have been right as the Dow has rallied from its August 25, 2015 closing low of 15666.44 to within ~3% of its all-time high. The third quarter romp has gone a long way toward answering the question about “passive” versus “active” portfolio management. Indeed, as reported by Russell Investment (not Richard Russell), “Active investment managers trounced the index in Q3 2015. 75% of large-cap managers beat the S&P/TSX Composite Index for the period. All investment styles outperformed the index with dividend-focused managers at the top.” There’s that “dividend” emphasis again.

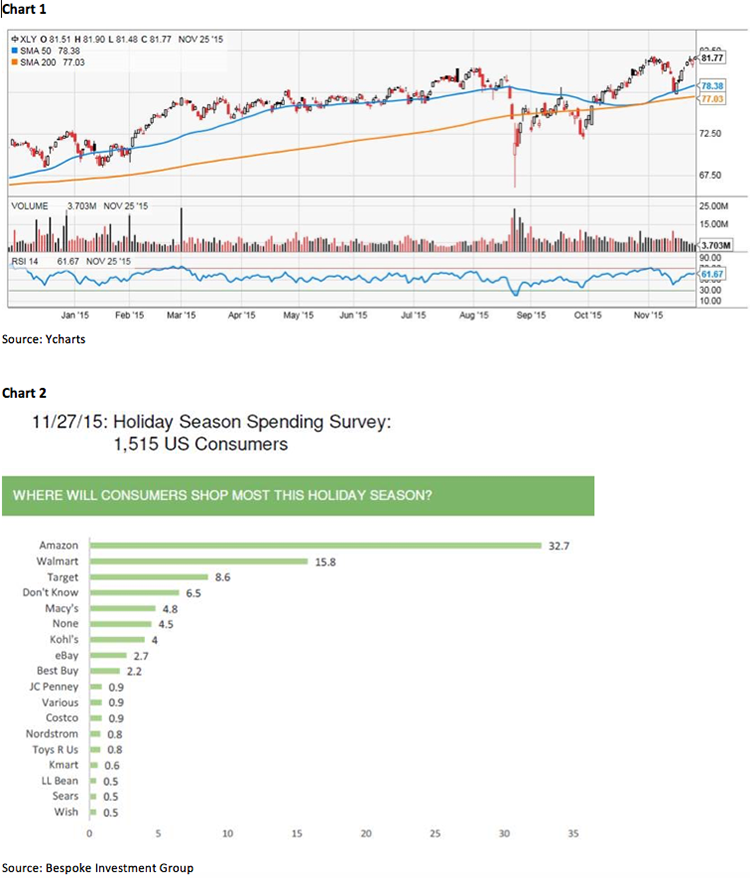

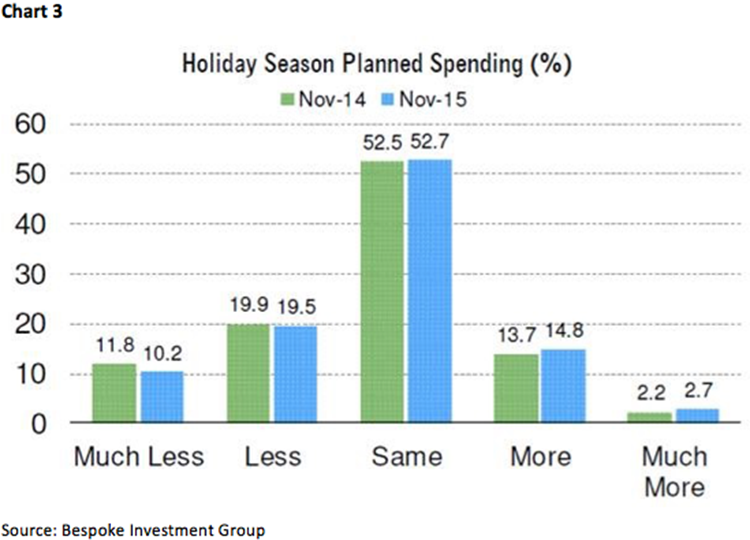

So tomorrow we enter the ebullient month of December, which The Stock Trader’s Almanac reveals is the strongest month of the year for stocks. Consistent with that, the D-J Industrials (INDU/17798.49), the S&P 500 (SPX/2090.11), and the NASDAQ 100 (NDX/4680.47) all reside above their respective 200-day moving averages (DMAs) of 17587.91, 2065.26, and 4449.64, respectively; and in the NDX’s case, its 50-DMA has bullishly crossed above its 200-DMA (The Golden Cross). Despite this bullish confluence, many pundits remain negative, while others are trumpeting it is going to be a lousy Christmas selling season. Tell that to the SPDR Consumer Discretionary ETF (XLY/81.47), which is trying to trade to new all-time highs (see chart 1 on page 3). Hereto, the XLY is above its 200-DMA and the 50-DMA has crossed above the 200-DMA. Asked about where consumers are going to shop, and how much money they are going to spend, Bespoke conducted a consumer survey showing that Amazon and Wal-Mart were by far the stores of choice (see chart 2). Also of interest is that there has been renewed strength is the small-caps as investors anticipate the January Effect where small-caps tend to rally from their tax-loss selling lows. We regard this as another positive sign.

The call for this week: When Turkey shot down the Russian fighter I instantly thought of the movie “Blackhawk Down,” expecting the stock market to crater. But after an initial 100+ point “morning melt” a funny thing happened, the Dow closed higher for the session. That caused one Wall Street wag to exclaim, “When stocks don’t react to bad news that’s good news!” Yet for the week the action once again proved frustrating, very much like this entire year. So I will leave you with another Richard Russell quip. To wit:

Nothing created by the mind of man has ever equaled the stock market in terms of its sheer ability to frustrate people. Why is this? The answer is that the stock market frustrates because millions of traders and investors across the face of the U.S. and the world are trying to make money out of the market. Now when millions of people are trying to make money out of the market, you know right off the bat that it can’t be done. A majority of people are not fated to make money doing anything, much less beat the stock market. ‘It’s not fair’ you complain, ‘why can’t all those nice, well-meaning people make money with their trading and investing?’ There’s one simple fact that makes it difficult. And that fact is that throughout history there have always been a small number of financial winners and an army of financial losers. So when we state that the stock market is frustrating, we must qualify the statement by asking, ‘frustrating for whom?’ And the answer again is that the stock market is frustrating to the great majority of participant-losers but highly rewarding to the small minority of informed, hard-working, intelligent winners.

To which I would add, this is why you need a good financial advisor! Richard, you will be missed . . .