Things are looking up in Europe, at least a little. Our global team of investment professionals met last month to discuss the outlook for the world’s major economies, and for Europe we agreed real growth is likely to be 1.75% for the next four quarters, which is slightly above our forecast at our previous investment forum in March this year. Also included in our base case for Europe: We expect the European Central Bank (ECB) to continue its policy of negative interest rates and maintain its quantitative easing (QE) programme at least until September 2016, with an increasing probability QE could be increased or extended. (Read more in PIMCO’s September 2015 Cyclical Outlook, “Has Europe Turned a Corner?”)

We believe domestic demand will be the primary source of the eurozone’s above-trend real growth due to improving private sector loan growth, which is responding to falling private sector interest rates, in turn driven down by low official interest rates and QE.

Based on our outlook, we have identified three key European investment themes that we believe will influence various strategies over the next 18 to 36 months.

1. Opportunities for carry

With the ECB continuing its monetary easing until at least September 2016, and possibly longer, we believe the current environment in Europe will be supportive of higher-quality carry trades while also creating an opportunity to sell more illiquid positions at attractive prices. Although there are a number of economic and investment implications for investors, we have identified three that we have been employing across our portfolios:

- We believe certain securities, such as legacy off-the-run structured credit asset-backed securities (ABS) and select off-the-run new issue securitisations, could offer an attractive pick-up in yield relative to ECB-eligible securities and may tighten as investors extend further out the credit curve, and to a lesser degree duration in response to ongoing QE. Moreover, numerous legacy structured credit ABS positions often have upside optionality not fully priced-in by the market.

- The ECB’s accommodative policies should be supportive for asset prices by reducing the deflationary tail risk. By extension, these actions should stabilise European bank loan portfolios and drive further deleveraging among European banks. While not without risk, we believe select subordinated debt bank instruments, such as lower Tier 2 securities from larger higher-quality banks, are one of the better credit volatility sells in the market today.

- Finally, select assets increasingly offer less attractive value as the ECB’s accommodation persists and a crowding-in effect ensues, with the impact most concerning in assets with an outsized illiquidity premium. Potential examples include select commercial real estate (CRE) in tertiary parts of the UK, Dublin (Ireland) and even Germany due to the marked compression in capitalisation rates. While we believe ECB support will continue until at least September 2016, the ability to sell at attractive levels at that time may quickly dissipate, particularly given the global uncertainty and the inherent illiquidity of the underlying asset.

2. European bank deleveraging still has another two to three years left to go

Despite over €300 billion in asset sales by European banks over the past few years (according to PricewaterhouseCoopers, 30 June 2015), we still believe the European bank deleveraging story has two to three years left to fully unfold. Importantly, the institutions active today versus those three years ago have changed, as have the types of assets sold or capital raised. This, in our view, will continue to evolve.

Moreover, we think the reshuffling of senior management – recent examples include Barclays, Credit Suisse and Deutsche Bank – as well as responses to the shifting regulatory environment, will likely result in shifts of business strategies.

Examples of a few key opportunities stemming from these changes include:

- Bad banks still have further assets to divest, including Spain’s Sociedad de Gestión de Activos Procedentes de la Reestructuración Bancaria (SAREB) and Ireland’s National Asset Management Agency (NAMA), with approximately €44.26 billion and €15.57 billion in total assets, respectively, primarily loans and receivables (net of impairment), remaining on their books as of 31 December 2014.

- Outside of SAREB, we expect Spanish banks will continue to be relatively large sellers of non- and semi-performing residential and small- and medium-sized enterprise (SME) loans over the coming months. We think a continuing Spanish recovery should allow for the bid-offer to narrow, allowing for more transactions to occur.

- Looking at Italy, legislative changes will likely increase the incentive to dispose of non-performing loans (NPLs) by potentially reducing the time it takes to recover on NPLs. These reforms could narrow the bid-offer spread on Italian NPLs and incentivise banks to be more proactive in disposing of risk, which currently totals more than €300 billion (according to PricewaterhouseCoopers, Bank of Italy, 30 September 2014).

- Finally, in Greece, assuming the government’s Memorandum of Understanding with its creditors holds, we would expect steady asset dispositions to occur there over the next few years.

3. An independent European lending market outside of the banking sector may be on the horizon

We believe that the combination of new banking regulations, the need for European banks to continue to deleverage and policymakers’ desire to sever the sovereign bank relationship will increasingly lead to more non-prime or “other” lending being done outside of the banking sector.

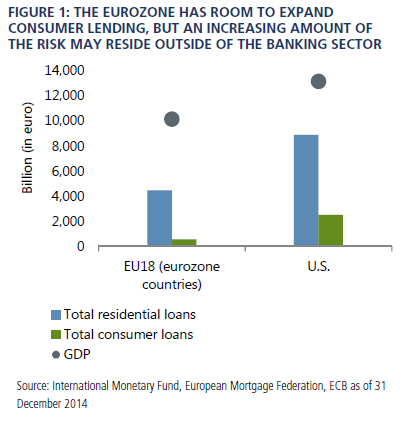

This theme will likely be influenced by the European Union’s Bank Recovery and Resolution Directive (BRRD), which is intended to create more stability in the banking system; but as structured, BRRD may also place investors and management at odds with each other. For example, European regulators put investors in bank securities across the capital structure at greater risk of a bail-in through the implementation of BRRD, while simultaneously asking bank management teams to increase the risk of their lending books (see Figure 1). The tension between these two objectives is particularly acute for banks in smaller, more vulnerable and less politically influential countries, as they are disproportionately likely to be bailed-in during periods of economic and sovereign volatility.

As a consequence, we would expect European banks in general, but particularly those in smaller and more vulnerable countries, to disproportionately focus primarily on higher-quality instruments, i.e., super-prime and prime borrowers, leaving other parts of the lending market void of activity.

The result, we believe, will lead to the creation of numerous independent niche lending opportunities across the UK and continental Europe. Examples include SME lending in Italy and Spain, CRE bridge-lending in Ireland and second-lien lending in the UK.

However, these investments are not without risk. Realistically, many of these platforms will be levered to the underlying economics of their sovereign entities; so understanding the broader macroeconomic dynamics will be critical to the success of investing. Additionally, variations in regulatory and legal regimes across Europe could limit scalability, which is particularly important in jurisdictions where it is not necessarily easy to right-size operations should volumes not cover fixed costs. Finally, the exit of any potential platform could prove challenging, particularly if selling to a banking entity is not a viable option.