Mass layoffs are being announced. The U.S., Central America, South American countries, etc. are all economic disasters. Major currencies are falling and raw materials companies are seeing huge order reductions around the world. Plant production has been reduced to 66% in the first half of 2015; there are fields of idle construction equipment that China is not buying. Look for Korea to dump products into the U.S. Wholesale raw sugar prices dropped from $0.36/pound to $0.11/pound leaving Brazilian sugar cane companies ready to file for Chapter 11. When do we see price reductions in candy bars in the U.S.? Who is protecting the ‘little people’? The Government? Wall Street? The States? How about nobody! The stock market is now a giant casino! When do the brokerage houses talk about it? Corporate profits are dropping, tax flows to Washington will drop, and the national debt will go to $21 trillion soon!

. . . An angry individual investor

Sitting at my perch I receive a lot of emails. Most of them are pleasant, insightful, or inquisitive, but a few times a week I get a vitriolic email like the aforementioned one from an individual investor. Usually when I receive such an item, I take a deep breath and try and figure out, “Why is this person so angry?” Most of the time, if I read the email a few times, it becomes apparent. In my response to that email, I did say that, “I told folks the first week of July the equity markets were going into a period of contraction, and have written extensively about the Dow Theory ‘sell signal’ of August 25th, so Raymond James did tell investors to get defensive.” On further contemplation, I should have added that I didn’t think the decline would be this severe because I did not believe the Industrials and Transports would break below their last October’s lows. And that breakdown, ladies and gentlemen, is what gave us a Dow Theory “sell signal.” Nevertheless, let’s attempt to address some of my emailer’s concerns.

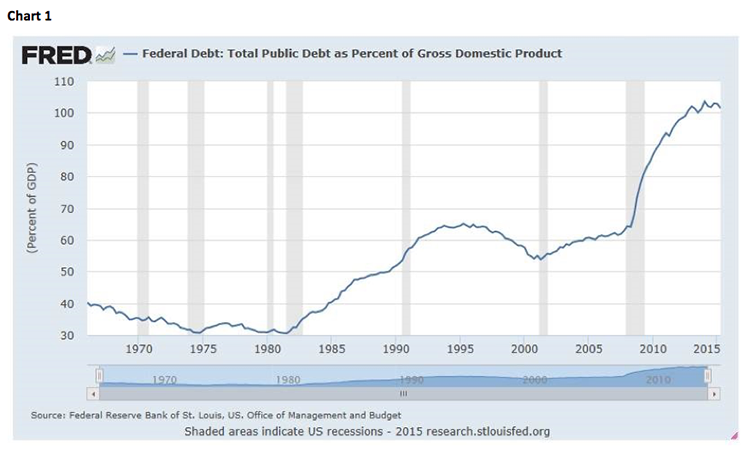

Judging from my emails, many people are concerned with the debt our country has accumulated. In my world, this is usually referred to as Debt-to-GDP; and sure enough, when one studies the Federal Reserve’s Debt-to-GDP chart it is worrisome (see chart 1 on page 3). However, I have argued for some time that is not the proper lens with which to view our debt. Even though I have written investment strategy since December of 1974, in a past life I was a fundamental analyst writing research on individual companies. In that role, when I dissected a company’s balance sheet, I not only had to look at the liabilities side of the ledger, but also the company’s assets. Herein is the problem with the Debt-to-GDP metric. While it may seem nonsensical to try and put a value on our government’s land, intellectual, natural resource assets, etc., they do indeed have tremendous value. This point was recently written about by Dr. David Eifrig. To wit:

The Claim: The U.S. economy is about to enter a depression. Gold will soar past $5,000, the dollar will become worthless, money will become unavailable, and interest rates will skyrocket to 15%.

The Fact: There are a lot of "doom and gloom" financial forecasters out there. They make a mixture of the claims above. Their solutions to these "problems" almost always involve selling all your stocks and bonds and putting your life's savings in gold. Most of these folks have been saying the same thing (wrongly) year after year for decades, or they are really young and inexperienced and claim to be experts. The fact is, America is in great financial shape. When you analyze the financial health of a country, a company, or an individual, you can't simply focus on one side of the balance sheet, as these people do. They only focus on liabilities. Instead, you need to analyze both sides of the balance sheet, and that means factoring in assets. If you want to know the net worth of America, simply take the assets it has and subtract the debt it has and you get a "net worth" of the country. This is the same for households. Looking at debt without looking at the assets is silly and naïve. The U.S. asset side of the balance sheet has increased incredibly, especially in light of the oil and gas finds this past decade. We're a much richer country than we've ever been.

Speaking to my emailer’s “layoffs” worries, in light of last Friday’s surprising employment numbers, is yet another misread. While somewhat disappointing, September’s payroll gain represented the 60th contiguous month of positive readings for the longest record since the government began keeping records. It is a fair point as to whether we are creating high paying, or low paying jobs, but that is a discussion for another time. I will not rehash the employment numbers, because the talking heads have done that ad nauseam. I will, however, share some thoughts from our economist, Scott J. Brown, Ph.D.:

One month does not make a trend, but the slower two-month pace in private-sector job gains likely reflects a stronger pace of seasonal hiring in the late spring and early summer (more jobs for teenagers in May and June, more seasonal layoffs in August and September) – moreover, that two-month pace is not far from what is considered a sustainable pace of job growth (that is, in line with the growth in the working-age population). The start of the school year and end of the summer travel season likely had an impact on the unemployment figures as well (while labor force participation was lower overall, it held steady for the key 25-54 aged cohort). . . . Beyond the headlines, this isn’t a terrible report – but it does raise the importance of the upcoming data reports (ISM non-manufacturing on Monday, but then mostly lite until retail sales on October 15).

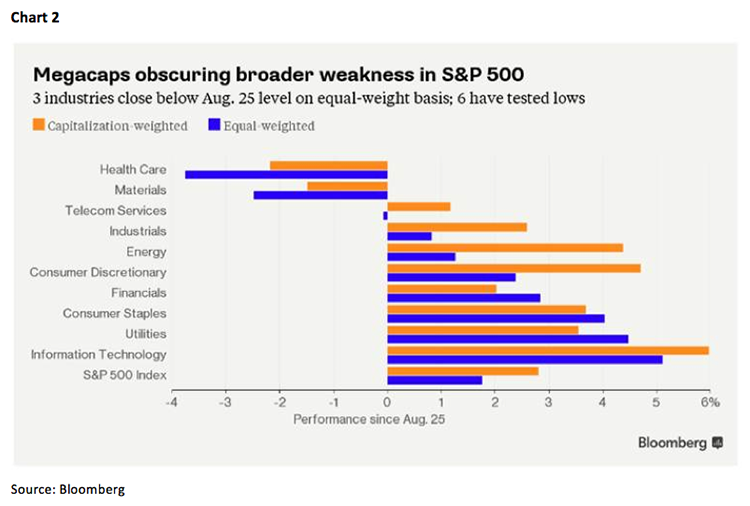

As for, “The stock market is now a giant casino,” comment, I guess high frequency trading (HFT) gives that appearance. But, I remember the mid-1960s when the computer traders gave the same appearance. The cry of the day was, “Computer trading is going to take over the market!” Subsequently, the tech stock boom ended in the late 60s, the “nifty fifty” peaked in the early-70s, and with those “bookends” so ended the computer trading craze. Then there is the narrowness (lack of breadth) of the equity markets that we have written about for months. Maybe that qualifies as a casino, for as Bloomberg writes:

While the Standard & Poor’s 500 Index is 1.9 percent above its worst closing level of 2015, almost 42 percent of the gauge’s members have slipped back below their Aug. 25 price. The heavyweights are doing all the lifting: Apple Inc., Microsoft Corp. and Exxon Mobil Corp., the three largest companies by market cap, account for nearly one-fifth of gains since the market bottomed after a four-day selloff of 10 percent. . . . Megacaps are obscuring weakening breadth in U.S. equities. To some, that’s an ominous sign amid market volatility that has seen the S&P 500 slide as much as 7.4 percent over the past two weeks, coming within five points of a 10-month low of 1,867.61 reached Aug. 25. The benchmark gauge fell 0.6 percent to 1,908.04 at 12:39 p.m. in New York.

However, one could argue that many stocks have already corrected by 20%+, setting the stage for another leg to the upside. A technical analyst would term that an “internal correction” (see chart 2). I would add, if the consensus 2016 EPS estimate for the S&P 500 is anywhere near the mark, at $129.45, that index is trading at ~15x 2016E EPS, which is certainly not expensive or casino like. Given those metrics, and Friday’s “rip your face off” upside reversal, I added to some stock positions. I bought the same names I mentioned on CNBC’s Nightly Business Report last Friday evening. Those names, all of which play to themes of mine and are favorably rated by our fundamental analysts, include: 9.4%-yielding StoneMor Partners (STON/$27.50/Strong Buy); 6.1%-yielding Genesis Energy (GEL/$40.88/Outperform); and 8.7%-yielding Flaherty & Crumrine Preferred Securities Income Fund (FFC/$18.69), which is managed by Don Crumrine, who has managed preferred portfolios for Warren Buffett.

The call for this week: To circle back to our original email, I would note, this is the kind of anger you typically see around market bottoms, not at the start of a new leg to the downside. That view was strengthened with Friday’s HUGE upside reversal. Unfortunately, I was in a meeting and unable to see much of it, so I pinged the uber-connected Dave Lutz at Jones Trading, who responded, “It started as a massive short-covering rally led by biotech and high yield energy names.” And sure enough, when I warped into my trading turret I looked at the session’s action. Around 10:30 a.m. the “upside squeeze” began vaulting the S&P 500 (SPX/ 1951.36) above 1900 and then spurting to 1915 around 11:10 a.m. From there, attempts to sell stocks failed, leading to another “squeeze” into 1:15 p.m. taking the SPX to 1936. After more failed tries to sell stocks, a final hour “squeeze” left the SPX trading at 1951.36, which was the session’s high. That action elicited this email, “What a strange market! Even "Never on a Friday" doesn't work. Maybe, just maybe, this is a start of an upside something?” I responded, “If you look at a chart of the SPX, it bottomed in a retest of the August lows on Tuesday the 29th. Today had nothing to do with ‘Never on a Friday’ and was all about the HUGE intraday upside reversal.” The resulting chart pattern looks conspicuously like a double-bottom (W-shaped). As I said last week, aggressive trading-types can trade the long side using Tuesday’s low as a stop-loss point. As I did, investors can judiciously commit a little capital to special situations, but should probably wait for the middle peak of the W-shaped bottom at 2020 on the SPX to be surmounted before becoming more bullish, because that is what it would take to complete a textbook double-bottom (see chart 3 on page 4). This morning the S&P 500 futures are following the rest of the world’s markets higher on the sense the Fed is never going to raise interest rates. I would note that the last time we had such a large reversal, like we had on Friday, was at the bottom in October of 2011 and we all remember how that turned out.