In the following interview, Portfolio Managers Adam Bowe, Isaac Meng and Tadashi Kakuchi discuss conclusions from PIMCO’s quarterly Cyclical Forum, in which the company’s investment professionals debated the outlook for global economies and markets. They share our views on economies and investment implications across the Asia-Pacific region over the next 12 months.

Q: PIMCO has described the global economy as having a multi-speed growth trajectory. How does the outlook for Asia fit within that framework?

Bowe: Asia definitely falls in the slow lane of PIMCO’s multi-speed world. While absolute levels of growth in countries like China remain comparatively high, the region as a whole is going through a fragile transition, with many countries experiencing slowing rates of growth and/or growth that remains below potential. While China continues to grapple with its own domestic transition away from export- and investment-led growth, the rest of the region is struggling to adjust economic growth models to a new environment. China has become a headwind rather than a tailwind, with its continued progress toward financial liberalization causing bouts of volatility across equity and currency markets.

This fragile transition is likely to result in further easing of monetary conditions across the region as policymakers attempt to support cyclical growth, either via lower interest rates, weaker currencies or a combination of both. Even in Japan, where we expect growth to improve over the next year as consumption recovers from the valued-added tax hike in 2014, persistently low inflation and the impact of China’s weaker growth trajectory and currency devaluation are increasing the likelihood of an expansion of Abenomics over the cyclical horizon.

Q: Could you elaborate on PIMCO’s view on China over the cyclical horizon? What are the implications of the plunge in equity markets and the yuan’s devaluation?

Meng: The Chinese economy is going through a multi-year New Normal adjustment. Growth will inevitably moderate as policymakers rebalance the economy away from investment and toward consumption, over-leveraged borrowers repair their balance sheets and frothy asset prices adjust.

Indeed, the adjustments got very bumpy in the third quarter. The credit-fueled equity bubble crashed and China’s A-share market has fallen by about 40% from its peak on 12 June. This sent severe shocks via the wealth, expectations and balance sheet channels. PIMCO estimates that the equity market crash will drag down GDP growth by up to 100 basis points (bps) over the next 12 months.

On 11 August, the People’s Bank of China (PBOC) relaxed the yuan’s quasi-peg to the dollar, a move that was followed by devaluation of around 4% in one week. Although this helped to correct the yuan’s moderate overvaluation and was marginally positive for exports, the surprising policy change raised the specter of policy exhaustion and the risk of competitive devaluation. This amplified negative shocks and spilled over to other emerging markets (EM), commodities and the global economic outlook. Capital outflows intensified, and the PBOC was forced to intervene heavily to stabilize the currency.

Clearly, there are daunting challenges in managing a gradual slowdown and structural adjustment in a highly leveraged economy with frothy asset prices. The PBOC, for instance, will face challenges in transmitting its monetary policy under a rigid foreign-exchange regime, while the need for fiscal consolidation in local governments (where debts are some 40% of GDP) also will limit fiscal stimulus. The risks of further real economic and market shocks are high.

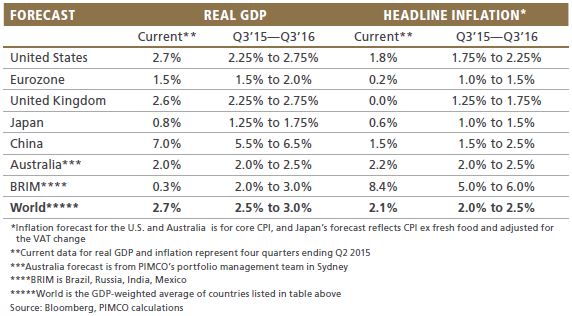

Under these circumstances, our baseline outlook anticipates GDP growth in China between 5.5% and 6.5% over the next four quarters. This is 25 bps weaker than our March forecast and remains well below consensus. We expect private capital expenditures and property prices to weaken further, risking a negative spillover to employment and consumer spending; these will be only partly offset by a marginal improvement in net exports and stimulus from constrained public investment. We see headline inflation between 1.5% and 2.5%. Given this, we expect to see a significant monetary policy response from the PBOC, including 75 bps in deposit rate cuts, a 200 bps cut in the required reserve ratio and devaluation of the yuan to 6.80 to the dollar.

Q: How do recent developments in China affect the outlook for Australia?

Bowe: Developments in China and broader emerging market Asia affect Australia through three key channels. First, via potentially weaker commodity prices that negatively affect Australia’s terms of trade and national income growth. Second, via export volumes, where Australia is the most exposed developed market economy to emerging Asia (including China). And third, via financial conditions that to date have been both positive (from a weaker Australian dollar) and negative (from weaker equity markets). The net impact via these three channels has undoubtedly been negative for Australia, and this is factored into our below-consensus outlook for growth and inflation.

Importantly, however, Australia continues to face its own domestic challenges as growth rebalances away from the resource sector. This rebalance is clearly happening, albeit slowly, and is the key reason we are not more pessimistic on the outlook. One can see the rebalance occurring geographically, with the mining states contracting while the larger non-mining states are growing at the quickest pace in several years. One can see the labor market rebalancing, with mining job losses being offset by gains in other sectors such as tourism. Indeed, aggregate employment growth through August this year had increased to 2%, its fastest pace for this period since 2011. Finally, one can see the rebalance occurring in the composition of private investment and in the growth of external demand, where the value of services exports is now larger than the value of iron ore exports for the first time since 2011.

Thus, our outlook for Australia calls for a continuation of the sluggish rebalance away from mining-led growth, in an environment where a reluctant Reserve Bank of Australia (RBA) will more likely than not be required to provide additional policy support over the cyclical horizon. Our below-consensus outlook for China, which incorporates the recent equity market correction and currency-regime shift, continues to skew the balance of macroeconomic risks firmly to the downside.

Q: What about Japan? How will the Japanese economy be affected by slower EM Asian growth and what policy response is expected?

Kakuchi: Similar to the Australian economy, the Japanese economy will experience multiple headwinds from slower EM Asian growth, and we see an increasing chance of additional easing by the Bank of Japan (BOJ) over our cyclical horizon.

More than half of Japanese exports go to EM Asia so a decline in sales of final goods to this region will naturally hit export growth. Moreover, a decline in Japan’s competitiveness also poses downside risk. Historically, devaluation of the yuan has resulted in greater depreciation of EM Asian currencies than the Japanese yen. In particular, strengthening of the yen against the Korean won will add headwinds to Japanese exports given their similarity with Korean goods. Therefore, the demand shock from the region and a decline in its competitiveness will negatively affect Japan’s economy.

Inflation will also be lower than otherwise. Japan imports about half its goods from EM Asia and weaker currencies in the region will create deflationary pressures on the Japanese economy. It is true that nearly 70% of imported goods are denominated in the U.S. dollar, but companies are likely to lower their export prices due to huge inventory overhangs, as evidenced in China’s steel sector.

What are the expected policy responses? On fiscal policy, we expect that a more accommodative stance will be adopted to cushion external negative impacts. In addition, with upper house elections being scheduled for next July, the administration of Prime Minister Shinzo Abe has a strong incentive to implement a more accommodative fiscal stance. On monetary policy, the BOJ is running a very aggressive QE policy; the central bank is buying nearly twice the annual net issuance of Japanese government bonds. Our base case scenario foresees the BOJ maintaining its current very easy monetary policy, although we see an increasing chance of even further easing given that the external backdrop poses more downside risk to Japanese GDP and inflation.

Q: What are the investment implications of PIMCO’s cyclical outlook for Asia?

Bowe: Our investment positioning in Asia reflects our expectation for easier, policy-induced monetary conditions across the region. In terms of duration, we are positioned for a flatter yield curve in Japan as the risk of a further expansion of the BOJ’s balance sheet has risen. We expect an increase in the scope of its quantitative and qualitative easing program that would require its bond buying to be focused on the longer end of the curve, and hence cause a flattening in the term structure of Japanese rates.

Despite our cautious outlook on Australia, we are fairly neutral on duration given that the market already prices in further policy accommodation from the RBA and we prefer to express downside macro risks via short positions in the Australian dollar. We also expect a further devaluation in the yuan. This will add additional downward pressure to currencies across EM Asia in countries that are already suffering from weak global demand and anemic export growth. We are positioning for this outcome via a basket of short positions in currencies such as the South Korean won, the Malaysian ringgit, the Thai baht, the Singapore dollar and the New Taiwan dollar.