SUMMARY

- The economic expansion should continue to support a low default environment for the credit markets outside of higher risk credits in energy and commodity-related sectors.

- A higher interest rate environment over the next year should cause a decline in new corporate bond issuance while demand for credit-related assets from investors will likely increase due to higher yields.

- Current valuations are “pricing in” a pickup in defaults, and investors should consider taking advantage of attractive valuations to add select credit risk.

While the U.S. economy continues to grow at a decent, though not stellar, rate of roughly 2.5% real GDP, softer global manufacturing activity, concerns over emerging markets growth and China’s recent move to devalue its currency have led to a pickup in market volatility and a tightening in financial conditions. Although the global outlook may be slightly more uncertain, U.S. economic fundamentals remain healthy, and growth above potential is causing the U.S. labor market to tighten, as evidenced by a greater-than 2% decline in the unemployment rate over the past two years to 5.1%. Over the past year the U.S. economy added 2.8 million private-sector jobs and over one million job openings, a 21% increase in openings.

With labor market slack declining, investors are sensing that the Federal Reserve will eventually raise short-term interest rates. Not surprisingly, companies have been issuing corporate debt aggressively to get ahead of an anticipated Fed “liftoff,” forcing debt markets to digest what is on pace to be a record $1.15 trillion in new investment grade corporate bonds this year, an increase of 15% from last year. While heavy new issuance has caused credit spreads to widen, equities have also come under pressure due to a slowdown in corporate profit growth as well as the heightened market volatility and uncertainty surrounding global growth and Fed liftoff.

Despite these concerns, the outlook for developed credit markets, and in particular the U.S. credit market, remains constructive. Here arethree reasons supporting the case for credit now.

1. The economic expansion will likely keep defaults low.

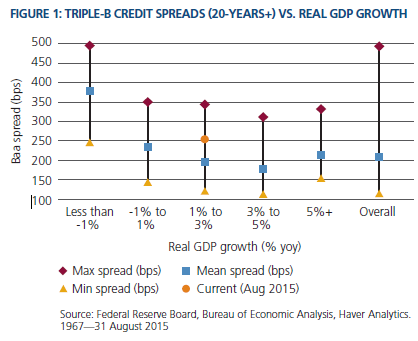

Credit markets tend to do well in economic expansions and poorly in recessions. In the U.S., a real rate of 2.25%–2.75% economic growth is “not too hot, not too cold,” and credit spreads are near the “sweet spot” as well, given the market is in an economic expansion. Importantly, credit spreads today look attractive relative to historical levels, in light of today’s economic growth rate (Figure 1).

Furthermore, the outlook for economic growth in developed markets remains supported by stable-to-improving fundamentals, a well-capitalized global banking sector and low imbalances in the private sector. While the Fed is expected to raise short-term rates at some point, it will likely remove policy accommodation at a gradual pace. Importantly, global central bank policy across most developed markets, including Europe and Japan, should remain highly accommodative, and policy is likely to ease in emerging markets in Asia, notably China. With healthy private-sector fundamentals and supportive global central banks, the economic expansion should continue to support a low default environment for the credit markets outside of a likely rise in the default rate in some higher risk credits in energy and commodity-related sectors.

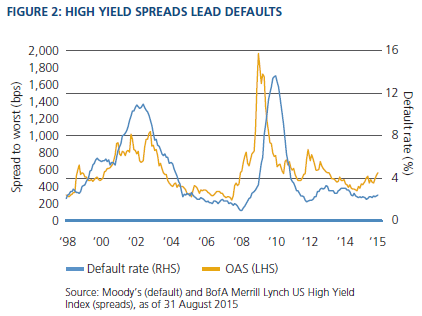

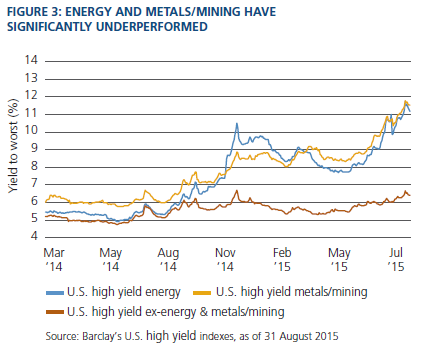

The higher spreads in the high yield market today are implying an increase in the default rate, primarily caused by commodity-related sectors (Figure 2). We believe the overall high yield market outlook away from this sector remains healthy given our constructive view on developed market economic growth. Importantly, yield levels in high yield ex-energy and metals have risen, and we believe they are attractive, particularly in the U.S. market where fundamentals remain supportive (Figure 3).

2. Higher interest rates should tighten credit spreads.

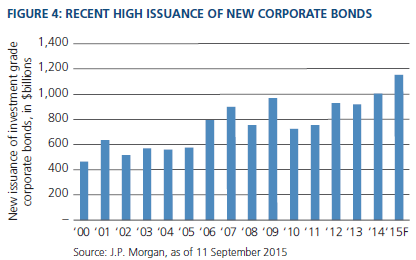

Low rate environments tend to lead to an increase in new corporate bond issuance as companies look to lock in cheap funding, and over the past several years, companies have in fact issued a significant amount of new corporate bonds to refinance and term out their balance sheets (Figure 4). At the same time, a low absolute level of interest rates typically attracts less demand as many investors have minimum yield and return targets.

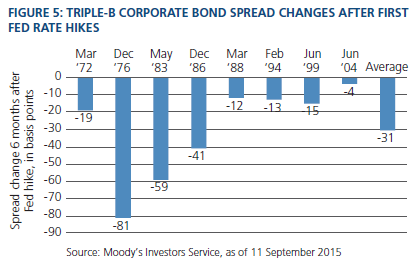

Over the next year, however, higher interest rates are likely due to improving private-sector fundamentals, modestly higher inflation and a gradual tightening of monetary policy by the Federal Reserve. In a higher interest rate environment, new corporate bond issuance should decline while demand for credit-related assets from investors will likely increase due to higher yields. Historically, credit markets tend to outperform after Fed rate hikes, with tighter credit spreads as soon as six months after the first rate hike (Figure 5).

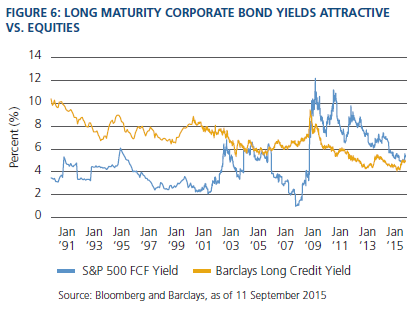

In addition, higher yields for corporate bonds in the context of a range-bound equity market should result in an asset allocation shift out of equities and into corporate bonds, particularly if profit growth slows next year, given that overall yields for corporate bonds are attractive today relative to the free cash flow yield on equities (Figure 6).

We also find bank loans attractive in an environment of rising interest rates. As a floating-rate instrument, bank loans tend to perform well because the all-in coupon rises as rates increase. Further, demand for floating-rate loans historically rises during rate hike cycles, as investors shift from more interest-rate sensitive strategies and equities to strategies that benefit from a rise in rates.

3. Credit spreads are attractive at today’s valuations.

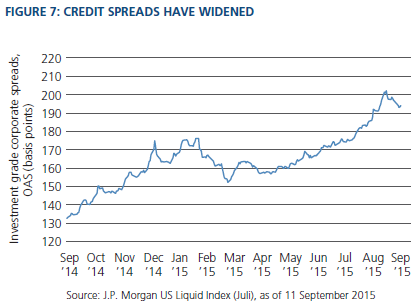

For investors, the main benefit of the significant amount of new corporate bond supply is that credit spreads have widened materially this year (Figure 7).

Large new corporate issuance has served a valuable purpose for companies in helping to keep future defaults low as balance sheets have been improved through the “terming out” of debt maturities into longer-maturity debt. With low near-term debt maturities and supportive economic growth, there are limited near-term catalysts outside of commodity-related areas for defaults to pickup. Given that current valuations are “pricing in” a pickup in defaults (Figure 2), we feel the case for credit is compelling and investors should consider taking advantage of today’s attractive valuations to add select credit risk.

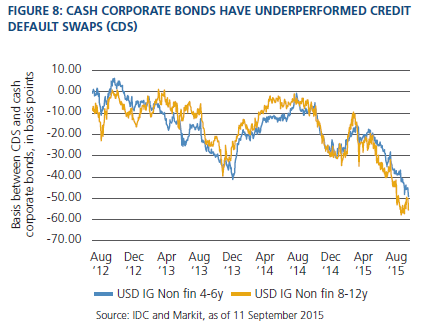

An investor has two options to gain exposure to credit markets: 1) buying corporate cash bonds or 2) adding synthetic exposure via credit default swaps (CDS). CDS spreads essentially price the credit/default risk of a credit and are usually unaffected by the technical dynamics of the corporate bond market. However, corporate bond spreads are usually affected by demand/supply technicals, in addition to the credit/default risk. This year, heavy new issue supply has put pressure on cash corporate bond spreads and caused them to widen relative to CDS spreads (Figure 8). For these reasons, we are favoring cash corporate bonds and new issues to selectively gain exposure now to the credit markets.

At current valuations, we view the credit market as attractive, given our outlook for supportive economic growth and low defaults. We find numerous opportunities today in U.S. housing and housing-related industries, consumer, telecom and healthcare sectors, and in banks and financials. Any credit spread widening or market volatility that occurs around anticipated Fed rate hikes should provide attractive entry points for investors in the credit markets.

Mark Kiesel

Chief Investment Officer, Global Credit

DISCLOSURES

Past performance is not a guarantee or a reliable indicator of future results. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Corporate debt securities are subject to the risk of the issuer’s inability to meet principal and interest payments on the obligation and may also be subject to price volatility due to factors such as interest rate sensitivity, market perception of the creditworthiness of the issuer and general market liquidity. Bank loans are often less liquid than other types of debt instruments and general market and financial conditions may affect the prepayment of bank loans, as such the prepayments cannot be predicted with accuracy. There is no assurance that the liquidation of any collateral from a secured bank loan would satisfy the borrower’s obligation, or that such collateral could be liquidated. Credit default swap (CDS) is an over-the-counter (OTC) agreement between two parties to transfer the credit exposure of fixed income securities. Derivatives may involve certain costs and risks, such as liquidity, interest rate, market, credit, management and the risk that a position could not be closed when most advantageous. Investing in derivatives could lose more than the amount invested.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Investors should consult their investment professional prior to making an investment decision.The option adjusted spread (OAS) measures the spread over a variety of possible interest rate paths. A security's OAS is the average return an investor will earn over Treasury returns, taking all possible future interest rate scenarios into account.

The BofA Merrill Lynch U.S. High Yield Index is an unmanaged index consisting of bonds that are issued in U.S. Domestic markets with at least one year remaining until maturity. All bonds must have a credit rating below investment grade but not in default. Barclays U.S. Long Credit Index is the credit component of the Barclays US Government/Credit Index, a widely recognized index that features a blend of US Treasury, government-sponsored (US Agency and supranational), and corporate securities limited to a maturity of more than ten years. The S&P 500 Index is an unmanaged market index generally considered representative of the stock market as a whole. The index focuses on the Large-Cap segment of the U.S. equities market. The JPMorgan U.S. Liquid Index (JULI) is an unmanaged index composed of USD-denominated corporate bonds issued by developed market corporations. Markit’s North American Investment Grade CDX Index, or the CDX.NA.IG Index (the “IG Index”), is a tradable index composed of one hundred twenty five (125) of the most liquid North American entities with investment grade credit ratings that trade in the CDS market. The IG Indices can be further divided into sub-indices (“Sub-Indices”) to represent specific portions of the credit markets (for example, by sectors, ratings or credit spreads). It is not possible to invest directly in an unmanaged index.

This material contains the opinions of the author but not necessarily those of PIMCO and such opinions are subject to change without notice. This material has been distributed for informational purposes only. Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO and YOUR GLOBAL INVESTMENT AUTHORITY are trademarks or registered trademarks of Allianz Asset Management of America L.P. and Pacific Investment Management Company LLC, respectively, in the United States and throughout the world.

©2015, PIMCO.

© PIMCO