. . . Look for hysteria to see if you shouldn’t go the opposite way, but don’t go the opposite way until you have fully examined it. Also, remember that the world is always changing. Be aware of change. Buy change. You should be willing to buy or sell anything. So many people say, ‘I could never buy that kind of stock.’ ‘I could never buy utilities.’ ‘I could never play commodities.’ You should be flexible and alert to investing in anything.

. . . Sometimes the chart for a market will show an incredible spike either up or down. You will see hysteria in the charts. When I see hysteria, I usually like to take a look to see if I shouldn’t be going the other way. . . . Just about every time you go against panic, you will be right if you can stick it out. . . . How do you pick the time to go against hysteria? I wait until the market starts moving in gaps.

. . . Never, ever, follow conventional wisdom in the market. You have to learn to go counter to the markets. You have to learn how to think for yourself; to be able to see that the emperor has no clothes. Most people can’t do it. Most people want to follow a trend; ‘The trend is your friend.’ Maybe that is valid for a few minutes in Chicago, but for the most part, following what everyone else is doing is rarely a way to get rich. You may make money that way for a while, but keeping it is very hard.

. . . Good investing is really just common sense. But it is astonishing how few people have common sense; how many people can look at the exact same scenario, the exact same facts, and not see what is going to happen. Ninety percent of them will focus on the same thing, but the good investor – or trader to use your term – will see something else. The ability to get away from conventional wisdom is not very common.

. . . Excerpt of an interview with Jimmy Rogers, Market Wizardsby Jack D. Schwager

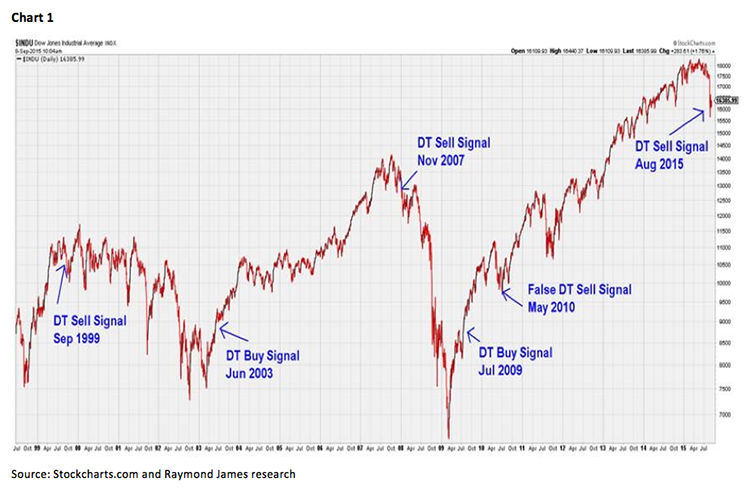

Going against the panic plunge of August 24th was pretty easy, especially if you heeded the market’s warning message in early July that Mr. Market was going into a period of contraction. The ensuing post August 24th “throwback rally” was also pretty easy to anticipate. From there, however, things have become much more difficult. In past missives we have suggested that forming a bottom is more of a “process,” rather than “event.” Andrew Adams and I have addressed that process by noting, “Following the Fed’s ‘no hike’ decision, my email box lit up with the ubiquitous question, ‘Have we seen another ‘V’ bottom like the one we had last October 15th? As often stated, while markets can do ANYTHING, I have seen a lot more ‘W’ (double bottom) shaped bottoms than I have ‘V’-shaped bottoms.” Also mentioned in last week’s Morning Tack were some indicators that argued for caution in the short-term. By far, however, the indicator that is causing me the most angst is the Dow Theory “sell signal” that was registered on August 25, 2015, when the Industrials and Transports closed below last October’s lows. As previously stated, there has been only one false Dow Theory signal in the last 18 years, at least by my method of interpreting Dow Theory. That was In May of 2010 during the “flash crash,” which was the last time the D-J Industrials were off 1000 points on an intraday basis. That “sell signal” proved to be false and was quickly corrected.

Fast forward, on August 24, 2015 the Industrials were similarly down 1000 points on an intraday basis, so I am hoping this “sell signal” will prove faulty as well. But, it gives me cause for pause because if you look at the attendant chart (chart 1 on page 3) you will see how accurate Dow Theory has been. I have included only the major signals because since the 2009 bottom there have been just too many “buy signals” to highlight them on the chart. So, for the stated reasons, I am temporarily ignoring the August 25th signal unless the Industrials and D-J Transports close below that session’s closing price. For the record, those closing prices were 15666.44 and 7466.97, respectively. If those levels are breached, it suggests a “change in trend” that must at that point be honored. As Richard Russell, arguably the best Dow Theorist of my lifetime, wrote years ago:

Most people have a hard time envisioning change, and they are almost incapable of envisioning major change. Most people are guided by their experience of the immediate past. If the past was good, they believe the future will be good. If the past was rotten, they believe the future will continue to be rotten. Yet anyone who has studied the history of the stock market knows this is not true.

By studying the second chart one can easily see that last October’s lows were decisively violated in August, which strongly suggests a “change of trend.” If one wants to try and spin that occurrence positively, one could observe that the S&P 500 (SPX/1958.03) has NOT violated its respective October 2014 low. But, it’s too bad the S&P 500 has absolutely no part in Dow Theory, and neither do the D-J Utilities.

Speaking to last week’s action, well it really wasn’t much of a surprise. As Michael Revilla, an astute Miami-based Raymond James advisor, emailed me last Wednesday:

Hey Jeff, is this “Buy the Rumor, Sell the News” that we are currently witnessing? I was implying this concept to this rally leading up to the Fed announcement. I remember when the House and Senate were voting on the bank bailout in 2008. The market rallied hard into the announcement and subsequently rolled over; if I am not mistaken, the Dow closed down roughly 1000 points that day. The quote that was used to describe that series of events was, “Buy the Rumor, and Sell the News”.

Bingo, Michael nailed it because that is precisely what happened Thursday afternoon. To wit, following the Fed “no hike” announcement pop, which took the SPX from ~2000 to 2021 and close to our upside target, “they” sold stocks, leaving the SPX off 25.5 points from Thursday’s intraday high and down ~5 points on the session. The selling continued on Friday, consistent with my mantra, “Never on a Friday!” Such trading action was telegraphed in last Wednesday’s Morning Tack with the quip, “With this Friday’s quadruple expiration, yesterday (last Tuesday) felt like a giant ‘short squeeze.’ The question now is can it continue through the Fed announcement and Friday’s ‘witching?’ If it does, we may be able to tag the 2040 – 2050 zone on the SPX, but I would not bet that happens” . . . QED!

So what now? Well, we have had the anticipated “capitulation low” of August 24th and the subsequent two- to seven-session “throwback rally.” Yet, all of the ensuing rallies did not quite make it to the prescribed 2040+ overhead resistance zone. Even last Thursday’s “no hike” rally fell short at 2021. That 2021 “print high” left the McClellan Oscillator about as overbought as it ever gets, combined with the credit spread breakdowns mentioned in that day’s Morning Tack. Typically, following a quadruple “witch twitch” (last Friday’s option expiration), what you tend to get is further weakness the next week. Initial support would be around 16000 on the Industrials, and 1909 on the SPX. However, a violation of the August 25th closing lows would be a decided negative.

The call for this week: If you want to put a positive spin on things, the six other times the stock market declined by 10% in four days, like it did in August, every time the market rose within a year. If you want to put a negative spin on things, there was a Dow Theory “sell signal’ last month. We are trying to stay constructive, but the negative evidence is mounting; and if the August 25th lows are breached, well you know how we feel. Last week’s “now you see it, now you don’t,” post rate hike announcement stock market action was predictable, for as we wrote, “The first ‘move’ following such an announcement typically is a wrong-way move. And, boy did that play in spades with last Thursday’s last hour downside reversal. The question this week is, “Will ‘they’ build on Friday’s Fade?” This morning, at least so far, that is not the case with the preopening futures flat as I sip a latté at Grand Central Station . . .