If the science of statistics can benefit me in anything, I will use it. If it poses a threat, then I will not. I want to take the best of what the past can give me without its dangers. Accordingly, I will use statistics and inductive methods to make aggressive bets, but I will not use them to manage my risk and exposure. Surprisingly, all the surviving traders I know seem to have done the same. They trade on ideas based on some observation (that includes past history) but, like the Popperian scientists, they make sure that the costs of being wrong are limited. Unlike Carlos and John, they know before getting involved in the trading strategy which events would prove their conjecture wrong and allow for it. They would then terminate their trade. This is called a stop loss, a predetermined exit point, a protection from the black swan. I find it rarely practiced.

. . . Nassim Taleb, Fooled by Randomness

Fooled by Randomness: The Hidden Role of Chance in Life and in the Markets is a book by written by Nassim Taleb that discusses the fallibility of human knowledge. Taleb’s main premise is that modern humans are mostly unaware of the existence of “randomness,” believing that random outcomes are non-random. Randomness is the lack of a pattern, or predictability, in events; a random sequence of events that has no order and does not follow an intelligible pattern. For example, according to Wikipedia:

When throwing two dice the outcome of any particular roll is unpredictable, but a sum of 7 will occur twice as often as 4. In this view, randomness is a measure of uncertainty of an outcome, rather than haphazardness, and applies to the concept of chance, probability, and emotional entropy. . . . In finance, the random walk hypothesis considers that asset prices in an organized market evolve at random, in the sense that the expected value of their change is zero, but the actual value may turn out to be positive or negative. More generally, asset prices are influenced by a variety of unpredictable events in the general economic environment.

One of Taleb’s main premises is, “Unlike Carlos and John, they know before getting involved in the trading strategy which events would prove their conjecture wrong and allow for it. They would then terminate their trade. This is called a stop loss, a predetermined exit point, a protection from the black swan. I find it rarely practiced.” Rarely practiced indeed, as can be seen in most portfolios this year, which is why I have averred, ever since arriving at Raymond James more than 17 years ago, “Don’t let ANYTHING go more than 15% - 20% against you without either selling, or hedging that asset to the downside!” As legendary hedge fund manager Paul Tudor Jones states, “I’m always thinking about losing money as opposed to making money. Don’t focus on making money; focus on protecting what you have.”

I reflected on Nassim Taleb while reading the excellent work from a true Dow Theorist, namely Tim Wood, and the insightful market letter at www.cyclesman.com. To wit:

It is going to be interesting to see how the talking heads try to minimize and spin the events of this past week. I can assure you that it will not be recognized by the mainstream for what it really is. For one, they don’t know and if they did they would not tell you. Did they warn you of the equity top in 2000 or in 2007? What about the housing top in 2005, or the top in oil in 2008 or 2013? No! They did not. It doesn’t work that way. Rather, the sheep are always told that everything is going to be okay. I warn you now that we are headed into an extremely deceptive time for those that do not understand the environment in which we are operating.

Like Tim, we too warned of the Dow Theory “sell signals” of September 23, 1999 and November 21, 2007, but regrettably few listened. We also warned in early July of this year that the equity markets were going into a period of contraction, although admittedly we did not think (at the time) it would be this severe. Nevertheless, we were prepared for what has happened. However, what has Wall Street done? As Tim notes they have trotted out the same “talking heads” that never saw the carnage coming to now tell us what the future holds. So I ask this question, “If they never saw the aforementioned downturns coming, why should anyone listen to them now?! While like most of Wall Street I too am trying to stay positive, if the D-J Industrial Average (INDU/16102.38) closes below its August 24, 2015 closing low of 15871.08, combined with a close by the D-J Transportation Average (TRAN/7793.83) below its closing low of August 25, 2015 of 7466.97, I will have to take a more defensive stance.

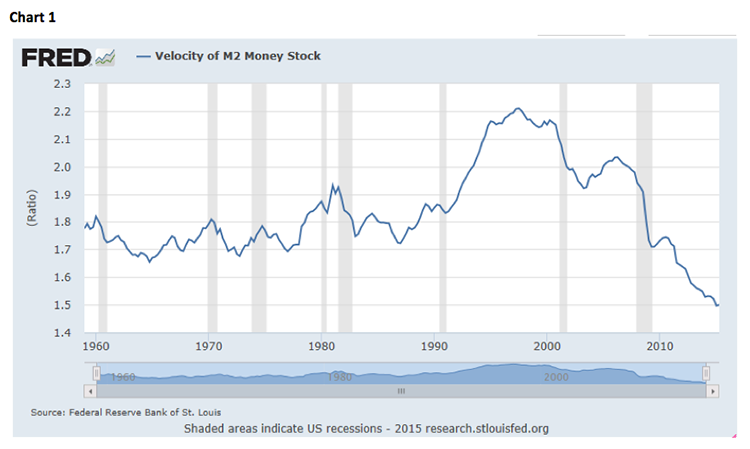

The reasons I am trying to remain constructive include: 1) valuations are still supportive with next year’s S&P 500 earnings estimate of $130.83 producing a forward P/E multiple of 14.5x and an earnings yield of 6.8%; 2) too much of a slowdown in the world’s economic growth is being priced in; 3) there is still huge liquidity; 4) many of the S&P 500’s stocks have already corrected more than 20%; 5) the economy is improving; 6) summer sell-offs tend to reverse; and 7) there has only been one false Dow Theory signal in the past 18 years and that was the “sell signal” occurring in the “flash crash” (5/6/10), which was reversed a few weeks later. I am hoping August 24th’s 1000-point Dow Dump will likewise prove to be another false signal. On the negative side: 1) about three weeks ago, before the bottom fell out, the Standard & Poor’s earnings estimate for 2015 fell below last year’s actual earnings; 2) what’s happening to credit spreads is worrisome; 3) the labor force participation rate is in the tank (chart 1 on the next page); 4) the velocity of money is non-existent (chart 2); and 5) there has been a Dow Theory “sell signal.” Whatever the outcome, the next few weeks are going to tell us a lot about the future direction for stocks.

The call for this week: While NOBODY can consistently “time” the market, if one “listens” to the message of the market they can tell whether you should be playing hard, or not so hard. In the fall of 1999 the equity market was “speaking” with a negative voice. In June 2003 the market’s voice was decidedly more positive. In November 2007 the tone was again somber, but it was ebullient in June of 2009. We listened and tilted accounts accordingly at those “trend changes,” but most pundits did not. So again I ask, “Why should anyone listen to those stock market gurus who never saw the 2000, 2008 and the recent downturns coming?” This week we look for a sharp rebound, very similar to what the SPX did on August 26th (+72.90) and August 27th (+47.15), but then for the indices to stall out in the 2030 – 2050 zone followed by renewed weakness.