The UK index-linked gilt market holds the distinction of being the oldest developed market inflation-linked government bond (ILB) market in the world. The first index-linked gilt was issued in 1981, well before the U.S. started its inflation-indexed Treasury programme in 1997 and many years before global ILBs became a mainstream asset class. That is interesting trivia for investors to know, but today, given outright valuations as well as relative valuations to other ILB markets, it might be more fitting to award the UK index-linked gilt market the accolade of being the most overvalued.

Of course, in today’s New Neutral environment, investors cannot, unfortunately, avoid structurally lower yields on bonds in general. However, current extremely low and negative real yields on UK index-linked gilts, particularly for long-dated bonds, do not appear to have any fundamental justifications. Put simply, it is the seemingly insatiable demand from UK pension schemes that has pushed valuations to extreme levels. These schemes feel they have no choice but to accept ever lower yields as they seek to immunise their inflation-linked liabilities. In this great chase, fundamentals are often ignored and valuations become – and quite often stay – extreme. While matching assets with liabilities is important, slavishly immunising just one aspect of the liabilities (sensitivity to changes in the discount rate) forces schemes to invest in an asset with low expected returns – and almost guarantees a growing funding gap.

Putting the index-linked gilt valuations in perspective

As Figure 1 illustrates, the 30-year index-linked gilt real yield has been at or just below zero for a large part of the last three years. In recent months, despite stronger UK growth and a less dovish Bank of England, real yields have dropped to all-time lows. At the current –0.87% real yield, if the 30-year index-linked gilt were to be held to its maturity, it would guarantee investors a whopping 23% loss in real purchasing power in terms of the Retail Price Index (RPI).

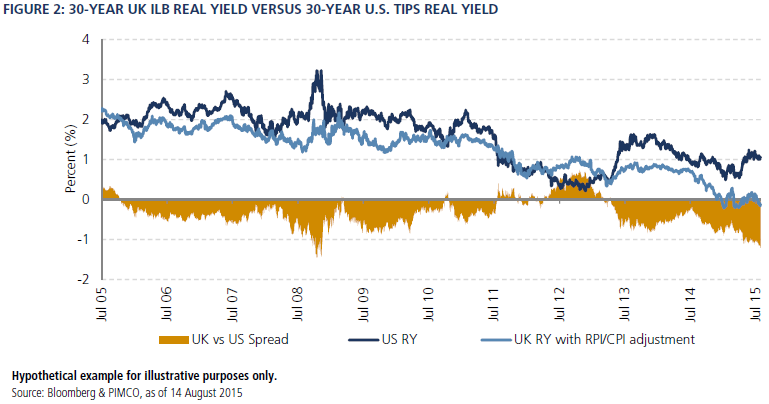

Another way to assess the valuation of UK gilts is to compare them with other inflation-linked bonds of similar quality. Figure 2 compares 30-year UK real yields adjusted for estimated RPI/consumer price index (CPI) basis with 30-year U.S. Treasury Inflation-Protected Securities (TIPS). The RPI to CPI adjustment is needed because U.S. TIPS are linked to the CPI while UK gilts are linked to the RPI, which has different weights and a different calculation methodology. As the analysis illustrates, over the last 10 years UK index-linked gilts have largely traded at a premium to U.S. TIPS (UK linker yields lower than U.S. TIPS yields), but more recently this premium has exceeded the highs seen in 2008, during the global financial crisis. Apart from a brief period in 2012 when UK linkers underperformed U.S. TIPS because of potentially adverse alterations to the RPI index, UK linkers have become increasingly more overvalued. Real yields on long-dated government bonds are a function of real growth expectations for the economy as well as the creditworthiness of the sovereign. Long-term growth expectations for the U.S. and the UK are roughly similar, while the U.S. is arguably a stronger credit. U.S. and UK CPI inflation have been broadly similar over the long term and this is likely to continue. Hence, one would expect long-term U.S. real yields to be somewhat below those of the UK. Yet, as of 14 August 2015, 30-year U.S. TIPS provided a positive real yield of 1.05%, whereas UK linkers yielded an estimated –0.10% after the RPI/CPI adjustment. Over the life of a 30-year bond, ignoring currency hedging costs, this difference in yields equals a roughly 40% difference in estimated total return between the two bonds in local currency terms, and assuming inflation is similar in the two countries.

Investors should ask two key questions: First, what has driven this chase to the bottom? And second, and more importantly, what does this imply for more flexible investors?

The forces driving index-linked gilt yields

The main reason for the ever-lower real yields and persistently high inflation breakevens on long-dated index-linked gilts is the seemingly insatiable demand for inflation-hedging instruments in the UK. According to data from the UK Pension Protection Fund (PPF), as of 31 July 2015 defined benefit pension schemes covered by the PPF in aggregate had £1.5 trillion of liabilities. Most of these liabilities are linked to inflation by regulation, whether it is to the CPI or the RPI. With many schemes now closed, the industry, which traditionally invested in equities to generate high real returns, now faces a shortening investment horizon. In recent years, this has prompted most schemes to start immunising interest rate and inflation risk by buying index-linked gilts and receiving UK inflation via inflation swaps. With only £450 billion of index-linked gilts outstanding and net new annual supply of about £30 billion–£35 billion per year, even considering the flows going through the inflation swap markets, supply and demand are significantly mismatched.

The regulatory link of pension liabilities to inflation and the requirement to value pension liabilities based on market yield curves have led to a circular behavior between the need for de-risking (more demand for linkers) and market yield levels. As pension funds seek to buy more index-linked gilts, they cause real yields to decrease. Lower yields, in turn, lead to growing deficits at the aggregate level as liabilities are discounted using these rates. As deficits widen, pension funds are under more pressure to more closely match the interest rate sensitivity of the liabilities, hence being forced to buy more at the lower yields, which imply lower future returns! For instance, according to the PPF, in July 2015, pension fund liabilities increased by 3.4%, reflecting reductions in conventional and index-linked gilt yields. During the same period, assets rose by 1.5%, with overall pension fund deficits widening by 1.9% – and that is just one month.

The implications for investors

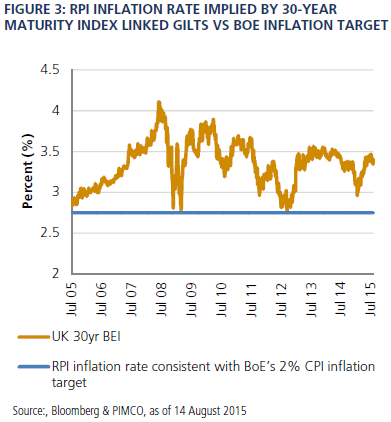

In our view, the choice is simple. Investors who have no regulatory need to own UK index-linked bonds can potentially get better value in other global ILB markets. Valuations are fundamentally much more attractive in the U.S. TIPS market. We believe investors constrained by pension fund regulations to invest only in the UK would be better off spreading their exposures between index-linked gilts and conventional gilts. As Figure 3 shows, the current (RPI) inflation rate implied by index-linked gilts in order to break even with conventional gilts is 3.5%, well above the Bank of England target inflation rate. Unless regulations that offer cheap funding are the government’s goal, the best long-term solution in our view would be to relax regulations that cause adverse investor behavior, i.e., forcing pension funds into assets that are guaranteed to return less than the inflation rate if held to maturity.