Reminding us of the current market is an anecdote about the Sport of Kings that took place in London. An American race horse owner, while parading his entry in the paddock just before the event, fed the horse what appeared to be a white tablet. Noticed and challenged by an English track official, Lord Marlboro, the American was informed that his horse would have to be disqualified. Protesting vehemently that he only gave the horse a sugar cube, the owner popped one into his mouth and offered Lord Marlboro a cube as proof. The English official tasted and swallowed the cube. He agreed with the owner that it was a harmless sugar cube and waived the disqualification. Just before the race horse was to enter the gate, the American signaled his jockey, instructing him to keep his horse clear of trouble near the start and try for the lead early since his horse was sure to win. “In fact,” he told the jockey, “Only two have a chance to beat our horse.” “What two?” asked the jockey. Replied the American owner . . . “Me and Lord Marlboro!”

... Author unknown

Holy cow, somebody must have slipped American Pharaoh a “sugar cube” last Saturday as horse and jockey (Victor Espinoza) made the turn into the withering stretch at Belmont Park and pulled away from the rest of the pack. American Pharaoh won by 5½ lengths and thus became the first Triple Crown winner since 1978, and only the 12th horse to do so. Indeed, he is the first horse since 1978 to sweep the Kentucky Derby, Preakness, and Belmont Stakes, which is likely one of the sporting world's rarest accomplishments. Hopefully, somebody will feed a “sugar cube” to the stock market this week because it certainly needs it. To be sure, the S&P 500 (SPX/2092.83) has fallen into the 2090 – 2100 support zone so often discussed in these reports. Failing to hold these levels would suggest a test of the 2040 – 2050 level and if that doesn’t hold, a potential decline into the 2000 – 2020 zone. The approximate cause for the recent stock weakness has been the noticeable rise in interest rates, which has seen the yield on the 10-year T’note jump from 1.65% last January to 2.438% last week. While many reasons have been offered for the rate ratchet, one of the better explanations I heard was from a European-based portfolio manager (PM). He said that recently ECB president Mario Draghi told European banks to “get liquid” and increase euro currency reserves. The PM went on to suggest that meant the European banks, which had been loading up with U.S. Treasuries because of competitive yields and the rising dollar, now had to sell treasuries and convert the resulting dollars into euros. I don’t know if he is correct, but it certainly fits nicely with what has been happening in the markets given the weaker greenback and slide in bond prices.

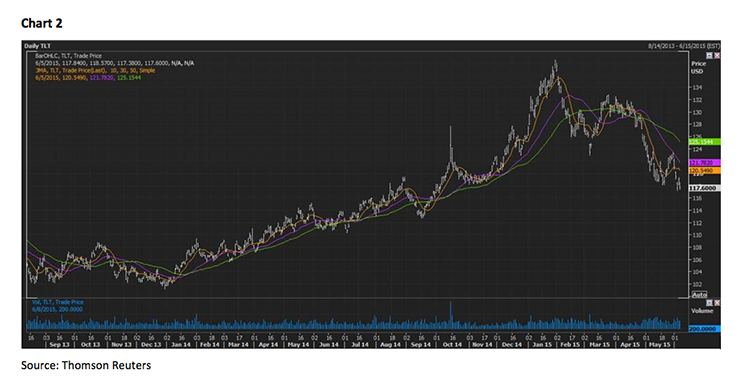

Speaking to the dollar and bonds, I have commented since mid-April that it looked to me as if the buck has “put in” a double-top in the charts (see chart 1 on page 3). By studying that Dollar Index chart you can observe the first peak coming in mid-March around 100 followed by a decline into the mid-90s. Then there is a “throwback rally” taking the index back to slightly under 100 . . . aka, a double top. Since then the index declined to ~93, re-rallied to 98, and then started down again. As for the bond market, as measured by the iShares 20+ year T’bond (TLT/117.60), hereto the TLT peaked in January at 138.50 followed by a decline to ~123 where another “throwback rally” commenced. That rally carried the TLT back to roughly 133 (see chart 2), not exactly the double-top the dollar displayed, but close enough for government work. As I said, I don’t know if he (the PM) is correct, but it certainly fits nicely with what has been happening in the markets given the weaker greenback and slide in bond prices.

The decline in the dollar, and concurrent rise in interest rates, obviously is impactful for stocks. With rising stock prices, and a rising dollar, the double-kick for foreign portfolio managers was irresistible. Of course now the worm has turned, which could also explain the weakness in equity prices. Then there is also what happens when you crank a higher interest rate into a dividend discount model, or most other stock valuation models. It is, however, somewhat of a head scratcher that with interest rates rising, while the economic statistics are weakening, why rates are heading higher. Maybe, just maybe, the bond market knows something the equity markets will figure out in the future. That being the economy, after a squishy 2Q15, is going to strengthen in the back half of the year. In last Friday’s Investment Strategy Committee (ISC) meeting our economist (Scott J. Brown, Ph.D.) stated that a number of economic readings are strengthening. That also foots with what ex-Secretary of the Treasury Tim Geithner said in our appearance on CNBC a few weeks ago. As I recall his comment, he said, “The underlying economy is stronger than the headline figures suggest.” Plainly that is what I believe. If so, as I stated in that same ISC meeting:

I still think earnings for the S&P 500 are going to grow by 4% - 5% on average for the year of 2015. I also believe companies are going to buy back somewhere between 2% – 2.5% of their shares. When added together that implies stocks could rally between 6% and 7.5%. Add in the ~2% dividend yield on the S&P and you look for an expected total return for the S&P this year of 8% to 9.5%. I know that sounds like pretty lofty returns given the meager returns year-to-date, and given all the consternations in the world but as repeatedly stated, “ The equity markets do not care about the absolutes of good and bad, but only if things are getting better or worse.”

As for the much feared 10% correction, my friends at the invaluable Bespoke organization had this to say over the weekend:

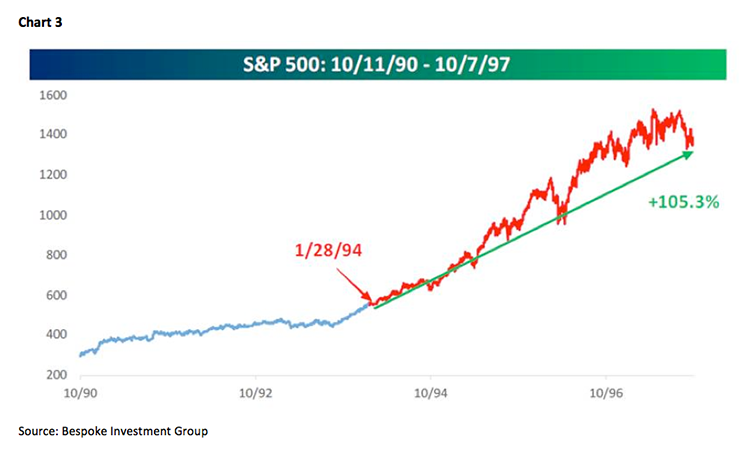

Naturally, the fact that the S&P 500 has gone so long without a 10% correction makes many investors uneasy that the market may be “overdue” for one. When the correction comes, though, is anyone’s guess. As bears painfully learned in the mid-1990s, just because we are due for a correction doesn’t necessarily mean it will come. Think back to the mid-1990s. On 1/28/94, the S&P 500 set what at the time was the longest streak of days without a correction of at least 10%. Many investors at the time probably thought stocks were due for a pullback then too, but had you sold all of your stocks or shorted the market just because the market was ’due’ for a pullback, you would have missed out on a 105% + gain in the S&P 500 over three years and nine months before we saw a correction (see chart 3).

The call for this week: The other worry on Wall Street’s mind is Greece. To this point, KochBank’s Christian Angermayer writes:

I think there is a 30% chance of Tsipras signing a deal and getting approval of the communist wing (by threatening them with new elections), a 30% chance he holds a referendum to force the communist wing to approve and a 30% chance he supports an interim technocrat government and then new elections. And a 10% risk he messes all up and fails.

It is worth mentioning, given my opening quote, that according to Bespoke, “Since 1928, there have been ten Triple Crown winners. Following those ten victories, the average change of the S&P 500 for the rest of the year was a decline of 9.01% with positive returns only once.” Whether that plays here is debatable, but I doubt it. This morning the preopening futures are flat on no real overnight news.