I always look forward to reading Frederick “Shad” Rowe’s monthly investment letter to his partners. Shad founded Greenbrier Partners, Ltd. In 1985 and has captained the investment fund ever since. He is known as one of the best “stock pickers” on Wall Street, a moniker that is well deserved. In his recent letter Shad writes:

On May 2nd for the twelfth year in a row, I attended the Berkshire Hathaway annual meeting in Omaha, Nebraska where Warren Buffett answers questions for five hours accompanied by Charlie Munger, who pipes in from time to time. For this month’s letter and in the Berkshire tradition, I thought we might answer a few of the questions I get asked from time to time and perhaps even a few that I ask myself (Note: If you are a slow reader, this exercise will require five minutes, not five hours.):

Question: You don’t seem to be talking about your stocks as screaming bargains. The market has been up six years in a row, you’ve had a great run, why don’t you just sell your stocks and buy them back when they get cheaper?

Answer: When you sell your stocks at a profit and pay taxes, that tax money is gone forever. If you continue to own really great stocks, you can theoretically own them forever. You can ride out down markets and not pay out a dime. This question also implies that you will make three correct decisions in a row, which in terms of probabilities is a severe challenge. What counts for most of us is our after-tax compounded return. While it is true that stocks are not historically cheap relative to book value or price to earnings multiples – traditional valuation metrics – they are cheap relative to what your cash will earn which is zero. In fact, Greenbrier recently moved some cash away from JP Morgan because we were going to get charged 1% on the balance. If the idea that cash is a liability gains more traction, then clearly stocks are an even better buy.

Now, I particularly like the comment, “While it is true that stocks are not historically cheap relative to book value or price to earnings multiples – traditional valuation metrics – they are cheap relative to what your cash will earn which is zero.” I like that statement because it is true! To be sure, stocks are not as “cheap” as they were in 2009, but they are not all expensive on a “relative basis” when compared to bonds. In fact, the only two valuation metrics that show stocks as extremely overvalued are the Cyclically Adjusted Price Earnings ratio (CAPE) and the price to book value. Many times in the past I have discussed why I don’t use the CAPE, one of which is because it would have kept you out of stocks for the past six years. Book value, however, is another discussion.

Speaking to book value, my friends at Day Hagen Asset Management put forth the notion that, “The price/book has trended higher over time as the economy has shifted from manufacturing and tangible assets to consumption and intangible assets.” To this point I would add that I believe book value for the S&P 500 is understated. Part of the issue is embedded in the depreciation schedule used by corporate America. In many cases capital equipment is depreciated at a much faster rate than the true life of the equipment. If, for example, a company depreciates a piece of equipment over a seven-year period, when the useful life of that equipment is say 20 years, it implies that company’s book value is vastly understated. Quite frankly, I don’t know how to adjust for this, but it does imply using book value as a valuation tool may be suspect.

I discussed many such points in Barron’s this week and particularly valuations, where I reiterated the P/E ratio for the S&P 500 should be somewhere between 18x and 20.5x. Specifically, the Rule of 20 states that the stock market is at fair value when the sum of the price earnings ratio, plus the rate of inflation, equals 20. Since the current inflation rate is around 2%, this suggests the S&P 500’s (SPX/2107.39) P/E ratio should be 18x (18 + 2 = 20). Another manner of targeting a potential P/E ratio comes from Benjamin Graham and it foots to ~20.5x. Currently, the SPX is trading at about 18.7x its trailing 12-month earnings and at 18.16x this year’s bottom-up operating estimate from S&P of $116.01. However, S&P’s estimated earnings for 2016 is $133.11, rendering a forward P/E ratio of 15.8x, which is not all that far above its historic median P/E ratio of 15.4x since 1929. Accordingly, while stocks may be at fair value on a nominal basis, they are not expensive on a relative basis when compared to yields. Most of my many emails over the weekend agreed with my comments in Barron’s; however, to be fair and balanced, I will chronicle the one pushback I received from a portfolio manager I have never heard from before. He wrote:

1) The "movie you've seen before" (1982-2000) began with sky-high interest rates and low levels of household debt and now we're at the exact opposite of that. Yes, the ratio of household debt to income is down a bit from 2005 but it's still around 105% vs 80% in 1980 and we now have massively more government debt (both on and off the balance sheet) too. So you may be referencing the wrong movie!

2) Interest rates that you cite to support stock multiples are UNDENIABLY a bubble, as real short-term US rates have been set by the Fed at NEGATIVE 150-180 bp for around seven years now. Any time you PAY people to take money (rather than charging for it) it's by DEFINITION a bubble. So your justification for stock valuations is predicated on a bubble. I suppose that it's okay to play that kind of musical chairs if you like, but you should at least acknowledge that the creator of a bubble (in this case the Fed) can't always control the pace at which the air goes out of it.

Okay that’s fair, and I agree that fixed income is bubblicious, but I expect it to stay that way for a lot longer than obviously my emailer does. And as stated inBarron’s, “Our model says she (Ms. Yellen) is going to raise the fed-funds rate starting in November, even though there is not a FOMC meeting that month, and that she is going to raise it by 25 basis points. Then we expect her to step back for two, three or four months and see how it impacts financial markets, as well as the economy.” Indeed, a gradualist ...

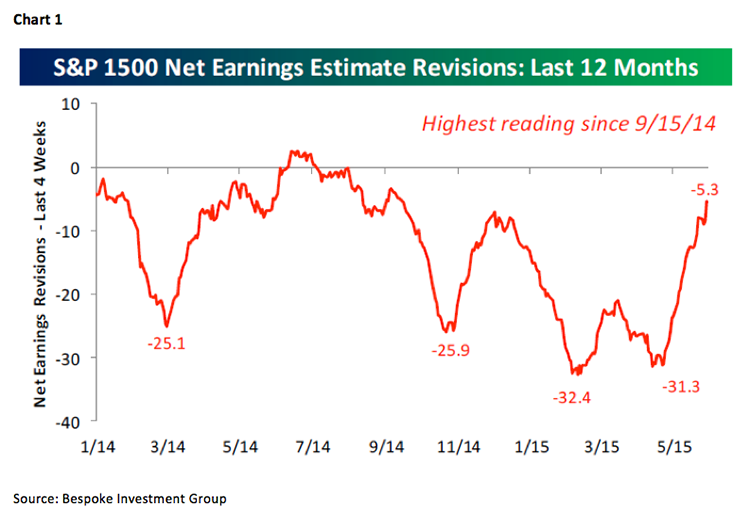

The call for this week: Last week the “secular bull market” theme came into question for the umpteenth time since our “bottom call” of March 2009. The latest boogie man has been the D-J Transportation Average (TRAN/8299.75), whose upside non-confirmation we have discussed ad nauseam since its occurrence last December when the Trannies failed to confirm the new all-time highs in the Dow. Unfortunately, many of the indices I follow failed to extend their upside breakout to new all-time highs recently. Nowhere was this more glaring than with the D-J Industrials (INDU/18010.68), whose upside non-confirmation by the Transports widened even more last week. Indeed, the Trannies extended their breakdown below the 8520 – 8580 support zone and in the process the 50-day moving average (DMA) fell below the 200-DMA (the death cross). Still, the Industrials have not fallen below their respective support level. The same can be said for the SPX as it continues to reside above the 2090 – 2100 level. Lost in the technical trauma has been the improvement in earnings’ revisions (see chart on page 3). This morning the preopening futures are marginally higher on no over the weekend news. I continue to think the SPX is organizing itself for a move higher as long as the 2090 – 2100 level is not breached.