Has The US Dollar Topped Out, Or Headed Much Higher?

|

The US dollar’s value has been on a tear since last summer, with the greenback’s value surging more than 20% against a basket of major foreign currencies. Reasons for the dollar’s sudden strong advance vary widely, but include the following among others:

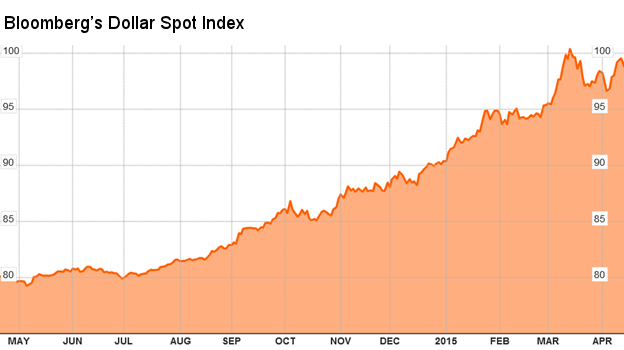

For these reasons and others, international capital has been flowing into the US at a near-record rate since last summer. This has definitely boosted the value of the US dollar since last July and may continue to do so. But questions remain. The first question is whether the strong rise in the US dollar will continue? There are some compelling arguments that it will, as I will discuss below. Yet in March of this year, the US dollar turned lower. So the next question is, whether the recent downturn in the US dollar is a real change of trend? I’ll offer an opinion as we go along. Following that discussion, we will delve into the latest data on who pays income taxes and who doesn’t. The numbers may surprise you, especially given that the Democrats want to raise income taxes on high income earners and corporations. What else is new? US Dollar Has Risen Over 20% in the Last Year A country’s currency is, in part, a reflection of how well or poorly its economy is doing. And, for the moment, the US is setting the pace for most of the developed world. US gross domestic product surged at a 5% annual rate from July through September, the fastest pace in more than a decade. As the recovery picked up speed in the 2Q and 3Q of last year, American employers added nearly 3 million jobs to their payrolls, the biggest gain in 15 years. Investors around the world looking for a piece of that growth have to use dollars to buy into it. And that demand for dollar-based investments drives up the price. In the second half of last year, the dollar rose more than 16% against a collection of world currencies. Let’s start with a chart of how much the US dollar has risen in the last year alone. The rise has been very impressive, especially in light of how much our national debt continues to rise – now above $18 trillion – the largest in American history. Let’s take a look.

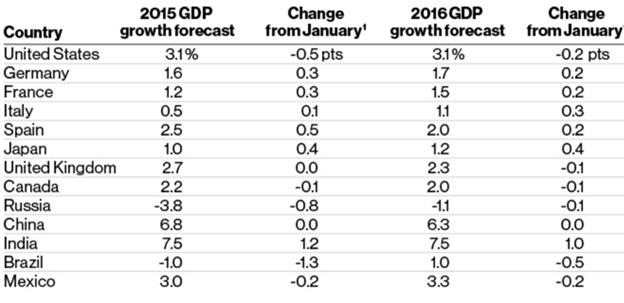

Bloomberg’s Dollar Spot Index, which tracks the US currency against 10 major peers including the euro and yen, has surged 20% since the middle of 2014. The gains stalled recently, sending the Index down more than 3% in the three weeks through April 3, as Fed officials tempered investors’ expectations about the pace of interest rate increases. Yet as you can see above, the dollar has rebounded in the last two weeks, and some analysts believe it will move significantly higher before this trend is over. The Really Bullish Case For the US Dollar US dollar bulls argue that there’s pent-up demand for the US currency that will lead to years of appreciation because the world is “structurally short” the dollar, so says former International Monetary Fund economist Stephen Jen and others. Sovereign governments and corporate borrowers outside America owe a record $9 trillion in the US currency, much of which will need repaying in coming years, according to data from the Bank for International Settlements (BIS). That’s up from $6 trillion at the end of 2008. In addition, many foreign central banks that had reduced their holdings of the greenback in recent years are starting to reverse course, creating more demand. The dollar’s share of global foreign reserves shrank to a low of 60% in 2011 from 73% a decade earlier, although it has since climbed back to 63%. While there will continue to be short-term ups and downs caused by changes in Fed policy, interest rates and economic data releases, the major trend may well remain higher due to these larger forces combining to fuel more appreciation, so Mr. Jen believes. He adds: “Short-covering will continue to power the dollar higher. The dollar’s strength is not just about cyclical factors such as growth. The recent consolidation will likely prove to be temporary.” Jen predicts that the dollar will climb another 9% over the next several months, and maybe more if the Fed hikes its short-term interest rate, which I don’t expect until September at the earliest. Of course, there are still some who believe the FOMC will raise the Fed Funds rate at the June policy meeting. Should that happen, I would expect the dollar to move to new highs, if it hasn’t already done so. Jen isn’t the only one who thinks short-dollar positions will cause the rally to extend. Chris Turner, head of foreign-exchange strategy at ING, sees the dollar surging through parity with the euro by mid-year. He said gains will be spurred by bonds from Germany to Ireland that are yielding below zero. “Central banks are re-accumulating their dollar reserves and low, or negative, bond yields in the euro zone will probably speed up that trend,” said London-based Turner, whose bank topped Bloomberg’s rankings for the most accurate currency forecasts in the past two quarters. Surging Dollar Boosts Europe, Japan & Others The International Monetary Fund (IMF) revised its forecasts for global growth in 2015 and 2016 last Tuesday, considering among other things the recent strength in the US dollar and weakness in other currencies. While the IMF downgraded its estimate of US growth modestly, it actually revised upward its forecasts for most of Europe, Japan and some other countries whose currencies have weakened against the US dollar. Let’s look at the latest numbers. The IMF left its projection for global growth in 2015 unchanged from three months ago at 3.5%. Underneath the stable forecast, however, the IMF depicts a global economy being reshaped by swings in currency markets and the drop in oil prices. The Washington-based lender of last resort cut its US expansion forecast by 0.5% to 3.1%, still the fastest among the most developed major economies. The Japan growth outlook increased to 1% from 0.6% in January. The euro area is projected to expand 1.5% from 1.0% earlier this year as weakening currencies provide a “welcome boost,” the IMF said. Here are the latest IMF estimates for 2015 and 2016.

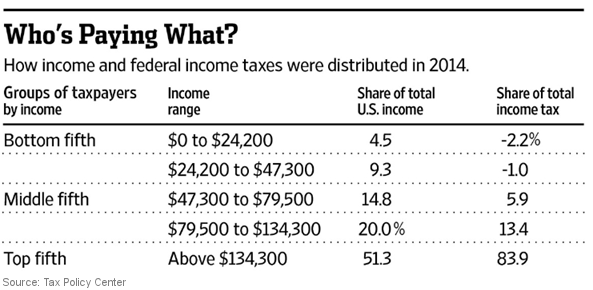

Elsewhere, emerging markets are showing their own mixed forecasts, with growth projected to slow to 4.3% from 4.6% in 2014, the fifth straight annual decline and the same forecast as in January. The figures show India will grow more quickly this year than China for the first time since 1999, according to the latest forecast. The IMF predicts India will expand at a 7.5% rate this year, up 1.2 percentage points from the January forecast. Meanwhile, China is expected to grow 6.8% this year, unchanged from January’s forecast. The world’s second-biggest economy is slowing as “previous excesses in real estate, credit and investment continue to unwind,” the IMF said. Brazil will contract 1.0% in 2015, compared with projected growth of 0.3% percent at the start of the year. The IMF projects an even deeper contraction in Russia this year than it did in January, with output expected to shrink 3.8%. The bottom line is that the rising US dollar has benefited most other countries which have seen their currencies weaken, thus making their exports cheaper on the world market. For the US, on the other hand, the stronger dollar has made our exports more expensive. Yet with exports accounting for only about 15% of GDP, the stronger dollar has not had a huge impact on our diversified economy. Who Pays Income Taxes in America & Who Doesn’t April 15 came and went last week and most of Americans who owed taxes dutifully paid them. Today, I thought we would look at the latest data showing who pays income taxes and who doesn’t. The numbers from 2014 may surprise you. According to the Tax Policy Center, the top 1% of earners – who had so much hate directed at them when the Occupy Wall Street movement captured the media’s fancy a few years ago – pays 45.7% (almost half) of all income taxes while making only 17.1% of national income. The top 20% of earners pay 83.9% of all federal income taxes. At the same time, they make only 51.3% of total US income. The middle 20% of earners pays only 5.9% of federal income taxes, while earning 14.8% of national income. Meanwhile, the bottom 20%, which earns only 4.5% of all US income, pays -2.2% (yes, negative 2.2%) of federal income taxes. In other words, those in this quintile, instead of paying an income tax, actually get paid money from Uncle Sam after Washington has taken it from everybody else.

Anyone who thinks this distribution is fair should think again. The system is so steeply progressive that Karl Marx would likely approve if he were alive today! This, of course, isn’t what we hear from redistributionists who go on and on about how “the rich don't pay their fair share.” A Pew poll in mid-February found that 72% of Americans think many wealthy people don’t pay their fair share of federal income taxes. An Investor’s Business Daily poll in March found that 90% of Democrats favor “raising taxes on the wealthiest Americans to pay for programs that will benefit the lower and middle classes.” So Democrats are now embracing a more full-throated kind of populism, releasing a new tax plan that takes from the richest Americans and Wall Street. Rep. Chris Van Hollen, the Maryland Democrat, is behind the proposal. You will be hearing more about it just ahead. How Government Disguises the Real Level of Taxes In various polls, most Americans say they believe they pay too much in federal taxes. Yet those views would be even more negative if people felt the full pain of funding the $4 trillion a year federal government. But the citizenry hasn’t resorted to pitchforks yet because politicians use “fiscal illusion” techniques to hide a lot of the costs. Here are some of the techniques (hat tip to The Daily Caller):

All these techniques make the “price” of government seem artificially low, such that Americans keep electing politicians who promise to give us even more of it. At the same time, fiscal illusions embolden politicians to spend money on activities that make no economic sense. But fiscal illusion is fiscal dishonesty. Whether people believe in small government or big government, they should want lawmakers to trade-off the costs and benefits of programs in a transparent way. So one goal of federal tax and spending reforms should be to repeal as many of these illusionary techniques as possible. I could go on (and on), but I’ll leave it there for today. |

|

Forecasts & Trends E-Letter is published by ProFutures, Inc. Gary D. Halbert is the president and CEO of ProFutures, Inc. and is the editor of this publication. Information contained herein is taken from sources believed to be reliable but cannot be guaranteed as to its accuracy. Opinions and recommendations herein generally reflect the judgement of Gary D. Halbert (or another named author) and may change at any time without written notice. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Readers are urged to check with their investment counselors before making any investment decisions. This electronic newsletter does not constitute an offer of sale of any securities. Gary D. Halbert, ProFutures, Inc., and its affiliated companies, its officers, directors and/or employees may or may not have investments in markets or programs mentioned herein. Past results are not necessarily indicative of future results. Reprinting for family or friends is allowed with proper credit. However, republishing (written or electronically) in its entirety or through the use of extensive quotes is prohibited without prior written consent. |