U.S. and Canada: Continued Recovery With Some Potential for Headwinds

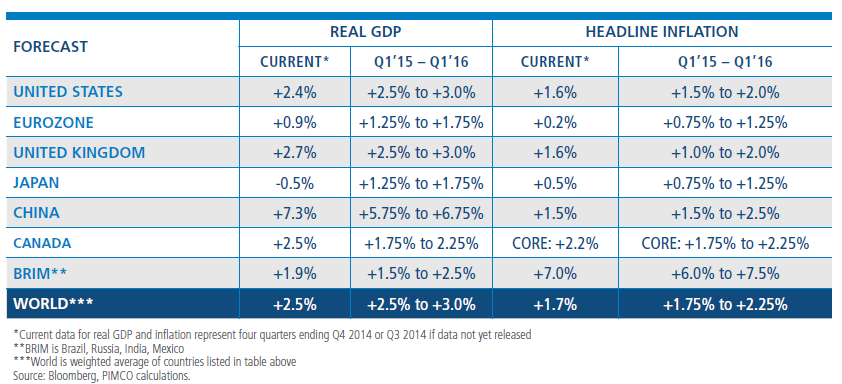

- We continue to believe that closing output gaps in the labor market and the boost to disposable income due to the drop in commodity prices will be a win for the U.S. consumer, driving growth of 2.5%–3%. However, offsetting this positive backdrop will be a drag on capital expenditures due to lower oil prices as well as the effects of a stronger dollar.

- There are two opposing forces that have potential for significant impact on the Canadian economy. The first, continued economic growth in the U.S., is a tailwind, and the second, the dramatic drop in the price of oil, is a headwind. That said, we see the balance of risks being tilted to the upside for our 2015 real GDP growth forecast of 1.75%–2.25%.

- In the U.S. we believe an underweight to duration in the front end of the U.S. yield curve is warranted, while overweighting non-agency MBS, TIPS and consumer spending and housing related credits.

- In Canada, we think real return bonds will outperform nominal bonds, and we prefer not to own federal government bonds and instead buy bonds issued by provinces and Canadian banks at relatively significant yield pickups.

Each quarter, PIMCO investment professionals from around the world gather in Newport Beach to discuss the firm’s outlook for the global economy and financial markets. In the following interview, portfolio managers Ed Devlin and Mike Cudzil discuss PIMCO’s cyclical outlook for Canada and the U.S.

Q: In December, PIMCO was optimistic about the U.S. economy in 2015. Is the U.S. still the global developed economy growth story?

Cudzil: Over the cyclical horizon, PIMCO expects the U.S. to grow at 2.5% to 3%. We continue to believe that closing output gaps in the labor market and the boost to disposable income due to the drop in commodity prices will be a win for the U.S. consumer. With consumption close to 70% of GDP, this favorable backdrop will continue to drive U.S. growth.

Having said that, since our last cyclical forum in December, oil has continued to decline and the dollar has continued to appreciate:

- While we believe that the decline in oil is a definitive positive for the U.S. on the whole, there will be winners and losers in this process. The benefit to the consumer will come, to some degree, at the expense of and the detriment to energy and mining companies. This expense will represent a drag on GDP via capital expenditures in this sector and could subtract as much as 0.2%–0.5% from GDP.

- The rapid appreciation of the dollar will weigh on GDP via the net export channel as well as strain corporate profits.

All of these moving parts have added a bit more uncertainty into the growth forecasts over our cyclical horizon, but the solid foundation for U.S. growth remains intact.

Q: What is your outlook for continued economic recovery in Canada?

Devlin: There are two opposing forces that have potential for significant impact on the Canadian economy. The first is continued economic growth in the U.S., which continues to be a main driver of export growth for Canada. The second is the dramatic drop in the price of oil, which is, without question, a headwind for Canada as a producer and exporter of energy. We agree with the Bank of Canada that the negative energy shock facing producers will be felt early in 2015 while the benefits of a lower currency for exporters and lower gas prices for consumers will be gradual tailwinds. Given PIMCO’s baseline forecast of oil recovering by $10–$15 by year end, we see the balance of risks being tilted to the upside for our 2015 real GDP growth forecast of 1.75%–2.25%.

Low interest rates, aided by the 25-basis-point surprise rate cut by the Bank of Canada on 21 January, should continue to support consumption and residential investment in 2015. While ultra-low interest rates risk future financial stability with overvalued housing and over-indebted consumers, we see this as an issue for 2016 and beyond.

We expect the key core inflation rate to stay near its current 2% level. While declining oil prices will affect headline inflation, they are largely stripped out of the key core inflation rate. The declining Canadian dollar will continue this year to put upward pressure on the core inflation rate via higher import prices.

So we will be watching oil, the U.S. economy and the evolution of BOC policy very carefully as the Canadian economy continues its volatile expansion in 2015.

Q: While U.S. employment has steadily improved over the past few years, there are finally signs that wages are rising too. Is broader inflation ahead?

Cudzil: With the unemployment rate closing in on the non-accelerating inflation rate of unemployment (NAIRU), and wage gains only one-half to two-thirds of what they are in traditional recoveries, wages should begin to show signs of normalizing. Along with some one-off anecdotes of corporations raising their minimum wages, there are survey-based indications and velocity measures that all point to rising wages over the cyclical horizon. Whether we look at the Job Opening Labor Turnover Survey (JOLTS) data on total job openings and the quit rate or NFIB Small Business surveys on “jobs hard to fill” and “plans to raise compensation,” all indicators are at or near pre-recession levels and point to higher wages.

With that backdrop for wages, our outlook for inflation is somewhat optimistic relative to market expectations, but inflation will not reach the Fed’s long-term objectives over our cyclical horizon. Although wages are moving higher, inflation will likely be held in check by the substantial move higher in the dollar along with the drop in commodity prices that we have seen since our last cyclical forum in December. This drop in oil should lead headline inflation close to or below zero out to the summer months. Having said that, we believe that core CPI should bottom at 1.5% to 1.6% in the summer before returning to 1.75% to 2% by the end of 2015. With so many central banks easing and some conducting quantitative easing (QE) due to a lack of global aggregate demand, our base case is for only a modest rise in inflation by the end of the year.

Q: PIMCO expects the Fed to begin raising rates for the first time in nine years. Discuss how that could play out. Will it be a bumpy transition off of zero? How do you think it will affect housing?

Cudzil: Given the continued improvement in labor markets and PIMCO’s forecast for inflation to move higher over the cyclical horizon, we believe the Fed will raise rates in the next three to six months and begin the process of normalizing monetary policy. Given that there is no peacetime example of a central bank exiting the zero bound, there are certainly risks to how this unfolds. PIMCO believes the Fed will begin to normalize rates as long as the unemployment rate continues to move toward the Fed’s target for NAIRU and the Fed is reasonably confident that inflation will rise to its long-term objective in the medium term. Along with this, once the Fed begins the process of raising rates, it will carefully monitor financial market and economic conditions to ascertain whether it can continue to raise rates slowly. We believe this is important. The Fed will only continue to raise rates and normalize monetary policy if the market and the economy allow it to do so. If growth were to show signs of weakening, or markets were to show signs of tightening financial conditions too quickly, the Fed would move even more slowly or altogether pause. Similarly, the Fed will raise rates at a more normal pace if inflation and employment reach its objectives and markets are functioning well. Finally, we believe that the destination for terminal fed funds is lower in this cycle, as high levels of debt will ultimately cause the Fed to settle on a long-term neutral rate of fed funds near 0% real.

We believe the Fed’s mentality will prevent monetary policy from having a meaningful impact on housing in and of itself. The taper tantrum in 2013 weighed heavily on residential housing activity as rates rose quickly in a vacuum without a commensurate move in economic activity and inflation. Given our base case of a Fed focused on financial conditions and economic activity as it raises the fed funds rate, it will only begin (or continue) the normalization process if the economy and markets can handle it. If rates are moving higher because wages and employment continue to improve, we do not believe this will weigh on housing. Our base case remains for housing to appreciate at 3% per year for the next two years, with housing velocity increasing as millennials move out of their parents’ basements and begin to form households of their own.

Q: Why did the Bank of Canada cut rates earlier this year, and what is the policy outlook?

Devlin: The Bank of Canada characterized its 25-basis-point rate cut on 21 January as an “insurance” policy. The BOC is concerned about the potential for the dramatic oil price decline to spill over into consumer and business confidence and the risk for that to create a larger drop in economic output than traditional models would suggest. The Stephen-Poloz-led Bank of Canada is clearly more dovish than when Mark Carney was governor. The Poloz-led Bank of Canada has shown a willingness to look past positive economic data and focus on weak economic data. For that reason, we think the BOC will take out another 25-basis-point “insurance” policy later in 2015. We think the Bank will continue to err on the side of supporting economic growth, and with so many question marks around the path of economic recovery in 2015, a third rate cut is possible later in the year if oil prices continue to decline.

Q: What are the investment implications of PIMCO’s economic outlook for the U.S.?

Cudzil: Although we continue to believe in The New Neutral, we also believe that markets are more than priced for this reality. It is against this backdrop that PIMCO believes an underweight to duration in the front end of the U.S. yield curve is warranted. As the consumer continues to benefit from an improving employment picture and increased disposable income due to a drop in oil, this should bode well for consumer spending and housing related activities. We continue to favor non-agency mortgages and select credit sectors with pricing power and barriers to entry. Finally, given our favorable inflation outlook relative to consensus and pricing in markets, we find Treasury Inflation-Protected Securities (TIPS) attractive.

Q: What are the investment implications of PIMCO’s outlook for Canada?

Devlin: Long-term nominal federal bond yields look unattractive (10-year yields at 1.4% and 30-year yields at 2.0%). The BOC has a long history of hitting its 2% target inflation rate, so with a current breakeven inflation rate for 30-year real return bonds (RRBs) at approximately 1.7% as of 30 March 2015, we think RRBs will outperform nominal bonds. Given that credit spreads have not kept up with the decline in federal government yields, we prefer not to own federal government bonds and instead buy bonds issued by provinces and Canadian banks at relatively significant yield pickups.

Past performance is not a guarantee or a reliable indicator of future results. All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed.Equities may decline in value due to both real and perceived general market, economic and industry conditions. Investing inforeign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Mortgage- and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and while generally supported by a government, government-agency or private guarantor, there is no assurance that the guarantor will meet its obligations. Sovereign securities are generally backed by the issuing government. Obligations of U.S. government agencies and authorities are supported by varying degrees, but are generally not backed by the full faith of the U.S. government. Portfolios that invest in such securities are not guaranteed and will fluctuate in value. Inflation-linked bonds (ILBs)issued by a government are fixed income securities whose principal value is periodically adjusted according to the rate of inflation; ILBs decline in value when real interest rates rise. Treasury Inflation-Protected Securities (TIPS) are ILBs issued by the U.S. government.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Investors should consult their investment professional prior to making an investment decision.

This material contains the opinions of the authors but not necessarily those of PIMCO and such opinions are subject to change without notice. This material has been distributed for informational purposes only. Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark or registered trademark of Allianz Asset Management of America L.P. in the United States and throughout the world. THE NEW NEUTRAL and YOUR GLOBAL INVESTMENT AUTHORITY are trademarks or registered trademarks of Pacific Investment Management Company LLC in the United States and throughout the world.

©2015, PIMCO.

© PIMCO