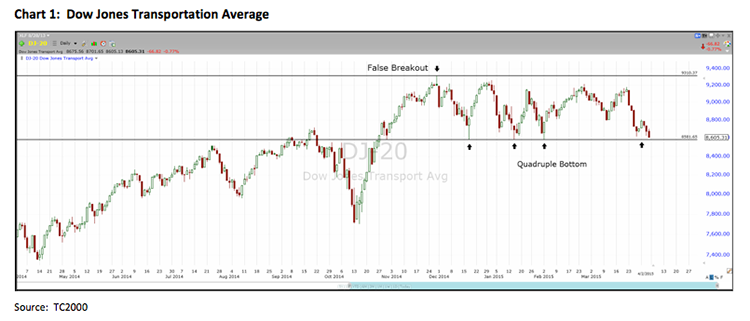

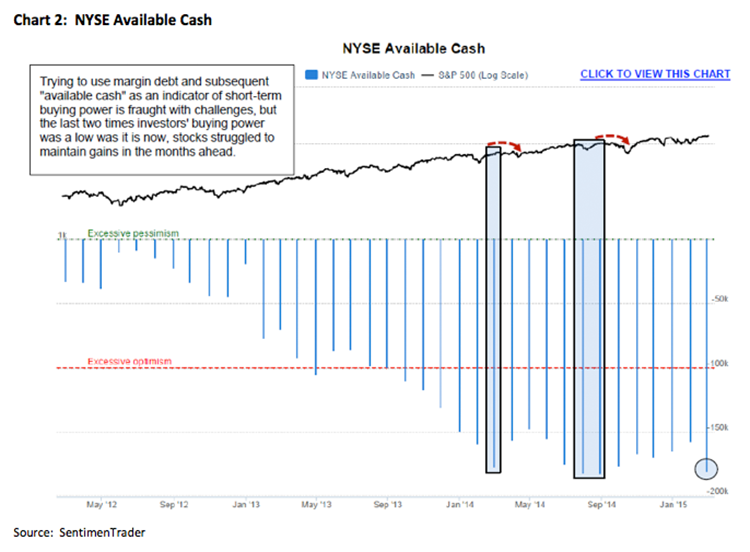

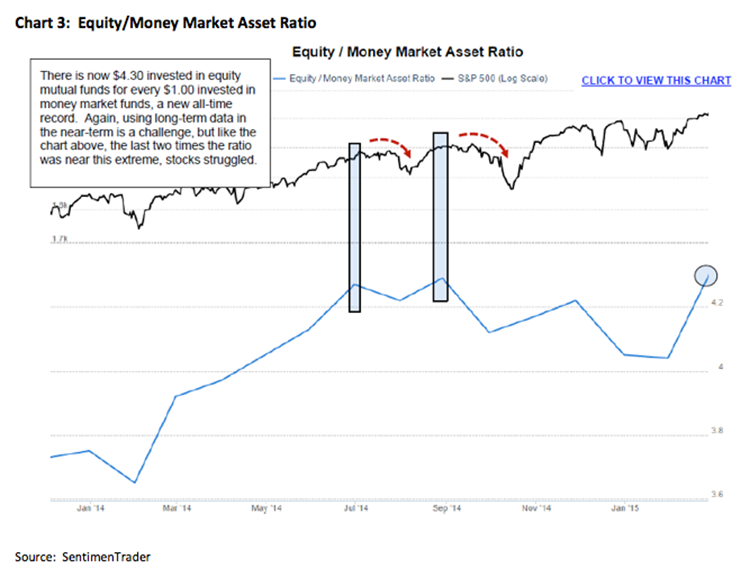

According to Wikipedia, “Brobdingnag is a fictional land in Jonathan Swift's satirical novel about Gulliver's Travels whose land is occupied by giants. Lemuel Gulliver visits the land after the ship he is travelling on is blown off course and he is separated from a party exploring the unknown land.” I thought of Brobdingnag as I stared at a chart of the D-J Transportation Average ($TRAN/8605.31) last week, which looks like it is making what a technical analyst would term a giant broadening top, or in my terms a “Brobdingnagian Top?” The chart pattern begins in November with a false upside breakout (to ~9310) that is followed by a decline into mid-December (to ~8581). Those high and low points set the stage for the parallel channel the Trannies have been locked in for going on six months. Interestingly, the chart formation also shows a spread quadruple bottom (four low points). Therefore, if 8580 is decisively broken to the downside, it is going to look pretty ugly in the charts (see chart 1). While it would not be a Dow Theory “sell signal,” it certainly would raise a red flag, at least on a short-term basis. Another “uncle point,” I wrote about last Thursday is the 2060 level for the S&P 500 (SPX/2066.96). Hereto, a close below that level would not look good to me. Meanwhile, the MACD indicator (Moving Average Convergence/Divergence is a trading indicator that is supposed to reveal changes in the strength, direction, momentum, and duration of a stock/index/commodity/etc.) is currently flashing the same type of warning signals it did in 1Q00 and 4Q07, not that I expect similar downside results. Then there is what Jason Goepfert, of SentimenTrader fame, wrote about last week. To wit, “Buying power available to investors is near an all-time low. The NYSE Available Cash figure has dropped to one of its lowest levels, and the last two times it was near this level, stocks struggled in the months ahead (see chart 2).” Meanwhile, again as Jason notes, “According to the American Association of Individual Investors, mom-and-pop investors have their highest exposure to stocks since 2007, and nearly their lowest cushion of cash since 2000 (see chart 3).” Whether any of this will be impactful in what is the best upside statistical month of the year (April) remains to be seen, but it has pushed me back into cautionary mode.

Whatever happens in the short run, I have never wavered in my long-term belief that we are in a secular bull market that has years left in it. This point was strongly reinforced as I read my friend Frederick “Shad” Rowe’s quarterly letter to his investors. I spoke with him last Thursday. Shad is captain of Greenbrier Partners, a private partnership that invests in publicly traded securities and has produced excellent returns since 1985. These are Shad’s words that resonated with me:

Many investors constantly worry about the state of the world or whether the United States is undervalued or overvalued relative to French stocks or whatever case they are making. They are failing to see that we are in the midst of a long-term cycle of wealth creation by American companies. ... Rapid technological change is doing more for people and doing it faster, better, cheaper, etc. ... and that trend is only going to accelerate. Interestingly, according to a recent Bank of America survey, investor sentiment toward American stocks is at the lowest point it has been since 2008. Some investors are skeptical of American stocks because they are more fully priced than some companies in Europe or some companies in Asia. But there are reasons for it. First among them is our increasing energy independence. There is also our ability to take what some people call ‘Moneyball,’ borrowed from Michael Lewis’ book about applying rigorous data analysis to baseball, and apply it to every aspect of American life: do it better, faster, cheaper, and do it in a way that is scalable and salable across the world. They are looking backwards not forwards and what I see are the same opportunities I saw three years ago only bigger.

Some of the stocks that Shad holds in his fund, which are rated Outperform by Raymond James’ fundamental analysts, include (with some of Shad’s comments attached):

Facebook (FB/$81.56) “Facebook Messenger now has 600 million monthly active users (up from 500 million in November), Messenger is becoming a platform for other apps (this is the route to monetization), Facebook user data can now be used to target non-Facebook mobile advertising via LiveRail, and that virtual reality seems as promising and far-off as ever.”

Apple (AAPL/$125.32) “Apple has the most desired digital ecosystem in the world and trades at a discount in comparison to the market and its intrinsic value on virtually every metric. Tim Cook’s performance at this year’s annual meeting could hardly have been better. He has escaped the shadow of Steve Jobs and is clearly in charge.”

Google (GOOG/$535.53) “Through organizing and providing access to the world’s information, GOOG has become the most powerful force in advertising and is navigating the world’s transition to mobile and video beautifully.”

eBay (EBAY/$56.91) “The value of eBay’s digital assets remains unrecognized by the investing public. We expect this to change over the next few months, as the PayPal spinoff approaches.”

Pulte (PHM/$22.70) “The current housing cycle appears to be different. A far more sustainable recovery in homebuilding is slowly gaining traction and is dominated by the biggest, most efficient builders.”

Bank of America (BAC/$15.54) “Bank of America represents a proxy on an improving domestic economy and the stock is cheap at 0.7x book value (1.1x tangible book value).”

We will be watching these stocks closely on pullbacks as potential “buy candidates.”

The call for this week: On Friday the U.S. March employment report did not make for pleasant reading with non-farm payrolls increasing by a mere 126,000 versus the consensus guess of 244,000. It was the worst report since December 2013. Adding insult to injury, there was a net revision of -69,000 jobs to the January and February numbers. Our economist, Scott Brown, Ph.D., had this to say, “Disappointing at face value – a smaller than expected increase in payrolls in March and a downward revision to the two previous months. Bonds have rallied, the dollar has weakened, the Fed funds futures have pushed out (implying a slower trajectory for short-term rates), and equities are poised to open sharply lower on Monday. The financial markets rarely look beyond the headline numbers, but this report wasn’t as bad as it seems. We could merely be seeing a statistical moderation (strong 4Q numbers followed by ‘softer’ 1Q figures).” This morning, however, Mr. Market is manic again leaving the preopening S&P futures off about 15 points at 6:00 a.m. on the jobs’ report. This is very likely going to break the TRAN below its spread quadruple bottom and the SPX below the 2060 level. If they close below those levels, it will not look good in the charts and will bring into view 1980 – 2000 for the SPX. On a more positive note, Saudi Arabia raised crude oil prices to Asia over the weekend on strengthening demand.

(c) Raymond James